Fertilizer prices in the Argentine market continue to trade below replacement cost due to cooling demand, just weeks before the start of the 2026/27 wheat and barley planting season.

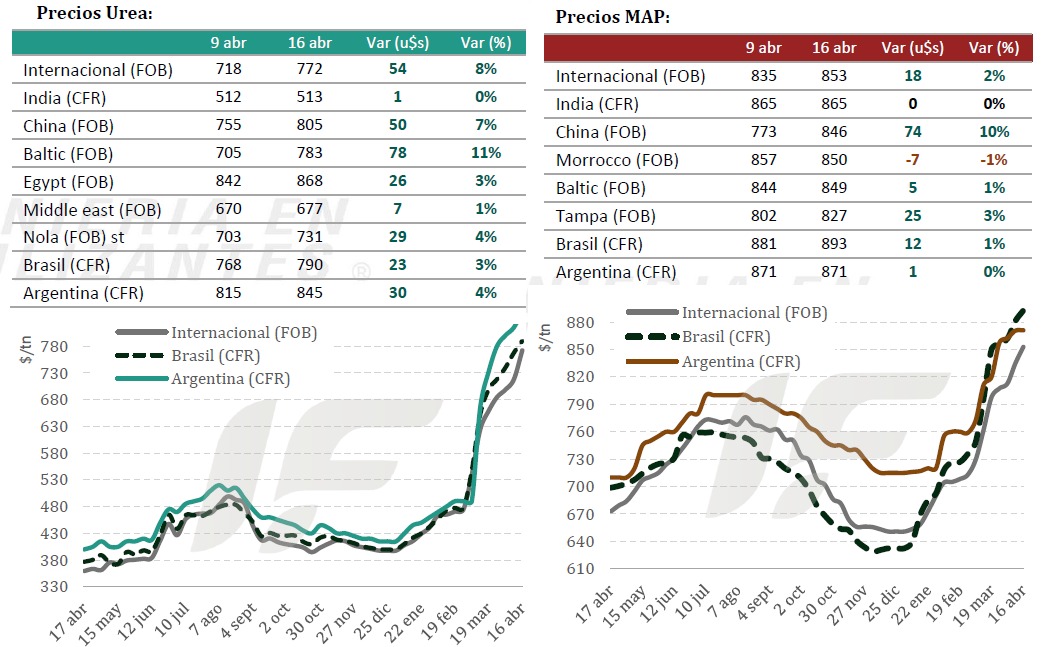

Import costs for phosphate fertilizers have risen between US$190 and US$200 per ton since the beginning of the year. Currently, diammonium phosphate (DAP) is priced between US$870 and US$890 per ton CFR, and monoammonium phosphate (MAP) between US$880 and US$910 per ton CFR.

“Although there are offers of MAP from Russia and Morocco reaching US$920 and even US$930 per ton CFR, Argentine and Uruguayan importers are refusing to accept such high prices. Some isolated purchases were reported at slightly lower levels—DAP at US$860 per ton CFR and MAP at US$890 per ton—but the volume is very small,” states the weekly market report from the consulting firm IF Ingeniería en Fertilizantes.

In the wholesale market, sales are stagnant because producers are reluctant to accept high prices. “For example, MAP is being sold domestically at around US$950 per ton, which is well below the US$1,120 per ton it would cost to import it at current prices,” the report notes.

Regarding urea import prices, this week the Argentine market showed a significant gap between sellers’ asking prices and importers’ willingness to pay.

“General assessments placed urea in Argentina in a firmer range of US$870 to US$900/ton CFR, reflecting theoretically negotiable levels in the market. Meanwhile, offers for fresh shipments have soared well above US$900/ton CFR,” the report notes.

“In contrast, importers’ willingness to pay is much lower, with a maximum purchase interest rate of US$800/ton CFR. In fact, offers for floating shipments at US$830-840/ton CFR recently submitted failed to gain traction or result in any deals,” it adds.

The document indicates that importers are showing little interest in the high international prices: they are expected to focus on acquiring domestically produced urea and utilizing existing local inventory.

“The imminent arrival of approximately 25,000 tons of imported urea is expected, with prices that will be significantly higher than domestic market levels,” it warns.

Urea is sold domestically at a wholesale price of US$880-900/ton, below the replacement cost, which is estimated at US$1,050/ton.

“There is a reluctance to pay for urea above US$900/ton, explained solely by wheat production costs. Argentine producers are buying less, retail sales have fallen compared to the previous year, and purchase delays point to potential logistical bottlenecks in the future,” the report states.

Internationally, this week the nitrogen fertilizer market was marked by a critically tight global supply and demand focused almost exclusively on India.

The supply crisis was exacerbated by Iran’s official ban on the export of all its petrochemical products (including urea and ammonia), along with reports of attacks on plants in Saudi Arabia and Bahrain. Only Oman is able to supply urea from the Persian Gulf.

“Attracted by exceptional margins, spot suppliers from Russia, Egypt, Algeria, Nigeria, and Southeast Asia will dedicate almost all their availability to fulfilling the Indian order, leaving very little volume for other destinations. Additionally, Russian plants continue to be affected by Ukrainian drone attacks,” the report states.

The global supply of ammonium nitrate (AN) and UAN remains tight. Russia is maintaining its ban on AN exports until the end of April, and in the US, UAN manufacturers report having exhausted their entire stockpile for the spring season.

The massive tender launched by the Indian corporation IPL absorbed the global supply: the lowest bids were US$935/ton CFR on the West Coast and US$959/ton CFR on the East Coast. “IPL has issued counteroffers at these prices to several suppliers, covering a total volume of 2.79 million tons, exceeding its initial target of 2.5 million.”

The global phosphate fertilizer market was also characterized by a severe deterioration in supply, although with evidence of demand destruction due to the inability to bear current prices in many destinations.

“In addition to the restrictions on exporting DAP and MAP, China unexpectedly banned sulfuric acid exports between May and December. This triggered a surge in global sulfur prices, raising production costs to levels seen during the 2022 crisis,” the report explains.

“Morocco’s OCP is cutting production due to high costs: it has brought forward maintenance that will reduce its capacity by up to 30% in the second quarter and has withdrawn its bids for Europe and Brazil,” it warns.

Saudi Arabia’s Ma’aden continues to divert shipments through the port of Yanbu on the Red Sea, which only covers 25% of its export capacity. “It is rumored that it has reduced its production to 80% as its storage capacity has run out.”

“India remains a key buyer of DAP at US$865/ton CFR, but importing at these prices generates operating losses of up to US$300/ton, making the market entirely dependent on state subsidies,” it summarizes.

Source: Valor Soja

Brazil Invests One Billion Dollars to Reactivate an Old Fertilizer Plant

Petrobras, the neighboring country’s mixed-ownership oil company, approved the resumption of construction on the UFN-III plant in Tres Lagoas, Mato Grosso do Sul, a nitrogen fertilizer plant that had been stalled since 2015. The decision involves an investment of approximately one billion dollars, and if the deadlines are met, the plant could be producing by 2029.

The news comes at a time of high tension for the global fertilizer market. Locally, 39% of Argentina’s fertilizer imports in 2025 came from countries in the Persian Gulf region, whose gas, urea, and ammonia production are key to the country’s grain production.

The conflict in the Middle East disrupted the supply chain, and the FOB price of urea surged by up to 42%, climbing from $483 to $685 per ton, levels not seen since late 2022.

UFN-III is designed to produce approximately 3,600 tons of urea and 2,200 tons of ammonia per day, with the surplus ammonia available for sale. The plant is located near key agricultural regions in Brazil’s Central-West, South, and Southeast. Petrobras argues that the project has a positive net present value in all its internal scenarios and will generate approximately 8,000 jobs during construction.

Brazil, like Argentina, is a major importer of urea. Brazilian domestic urea consumption is around 8 million tons annually, driven primarily by crops such as corn, sugarcane, and coffee. The new plant aims to reduce this dependence and improve the security of supply for Brazilian agriculture.

On the Argentine side, the picture of dependence is equally striking. According to the Rosario Board of Trade, Argentina imported 4.1 million tons of fertilizers in 2025, with urea and phosphates leading the external purchases. This volume represented a 28% increase compared to 2024 and constituted the second-highest import level of the century, surpassed only by the record of 2021.

Nitrogen fertilizers, among which urea stands out, were the most imported at 2.10 million tons, equivalent to 52% of the total. Adding to this, Profertil, the main national producer of granulated urea, experienced two production shutdowns during 2025, further increasing the need for external supplies.

The commissioning of a plant of this magnitude in the neighboring country could have indirect effects on the South American fertilizer market. A greater regional supply of urea and ammonia can help moderate prices and diversify supply sources, reducing exposure to geopolitical shocks like the current one in the Middle East.

However, it’s important to keep things in perspective. Construction wouldn’t begin until the first half of 2026, and commercial production wouldn’t start before 2029. For the upcoming wheat and corn seasons, Argentine agriculture will continue to rely on the same sources as always.

Source: Valor Soja

China limits fertilizer exports as the country prioritizes domestic market

China is becoming less prominent as a major exporter in the global fertilizer market because its government is focusing more on ensuring local farmers have an affordable supply. Tighter export controls and higher production costs are likely to affect fertilizer prices and availability in key importing regions such as Brazil, India, Southeast Asia, and Oceania.

China has been one of the world’s top producers and exporters of fertilizers, especially phosphates and nitrogen-based products, with exports worth over USD 13 billion in 2025. Since mid-March, the government has tightened export controls through the China Entry-Exit Inspection and Quarantine system, limiting shipments of phosphates and most nitrogen fertilizers, including urea. These steps aim to keep enough supply at home during the busy planting season, and the government has also released reserves to help keep local prices steady. Exports, especially of nitrogen products, are expected to slowly pick up again after May.

Higher sulfur costs are making fertilizer production more difficult. Sulfur, which is essential for making phosphate fertilizers, has become more expensive due to supply constraints and political tensions in the Middle East, particularly around the Strait of Hormuz, a key route for sulfur trade. These higher costs have led China to produce less phosphate and to temporarily ban exports until August. At the same time, strong domestic demand means there is less urea available for export, and shipments are unlikely to resume before May. Ongoing disruptions in the Arab Gulf, a major global urea supplier, are further tightening the supply situation.

China will likely remain an important player in the global fertilizer market, especially in Asia-Pacific. However, its exports will be guided more by local needs than by international demand.

Source: Fertilizer Daily

Mosaic has sold 40 000 t of DAP to South Asia

US phosphates producer, The Mosaic Company, has reported selling about 40 000 t of DAP for loading in early June and for shipment to South Asia.

Mosaic has estimated a netback from the delivered price of approximately US$840/t fob Tampa.

Mosaic did not clarify the exact destination, but India is the most likely within South Asia. If so, the delivered price is likely to be in the high US$900s/t cfr or low US$910s/t cfr. But no sale to Indian importers at this level has emerged. The latest confirmed DAP sale to an Indian importer was at US$865/t cfr.

Mosaic also did not confirm if this sale is to a trading firm or importer.

Source: World Fertilizer

OVERVIEW OF ARGENTINA’S MAIN CROPS

SOYBEANS: After a week-on-week increase of 4 percentage points, the soybean harvest has reached 10.2% of the suitable area nationwide. However, harvesting delays persist following recent rainfall events, due to waterlogged fields in large parts of the agricultural region. Simultaneously, based on satellite image analysis, the national planted area was adjusted to 17.2 million hectares (MHa), representing a reduction of 400,000 hectares from the previous estimate. Nevertheless, improved water availability since mid-February in Córdoba, western Buenos Aires, and both Core regions has boosted first-crop soybean yields above expectations. In the Northern Core region, weekly harvested yields average 39 quintals per hectare (qq/Ha), while in the Southern Core region they reach 42 qq/Ha, values that are above the average. Under this scenario, yields allow for offsetting the decrease in planted area and increasing the production estimate by 100 million tons, reaching a new production projection of 48.6 million tons.

CORN: Regarding corn, the harvest continues to progress nationwide, reaching 26.5% of the suitable area, with an average yield of 86.9 quintals per hectare (qq/Ha). Recent rainfall has slowed the progress of harvesting, as crews await improved soil conditions to allow them to resume work in the fields. Meanwhile, collaborators from various regions report that the soybean harvest is now being prioritized. Regionally, yields are at 100 qq/Ha in the Northern Core region and 95 qq/Ha in the Southern Core region. As for late-planted corn, 30% of the area has already reached physiological maturity, while the remaining crops are in the grain-filling stage. In this context, crop conditions remain mostly favorable, with 98% of fields rated between Normal and Excellent. Given this scenario, the production forecast remains at 61 million tons (MTn).

SUNFLOWER: Meanwhile, sunflower harvesting continues to progress slowly in the southern part of the agricultural area, due to recurring rains that delay drying and hinder normal operations, both because of waterlogged fields and reduced road access. After a week-on-week increase of only 1.4 percentage points, 91.3% of the suitable area has been harvested, and the resumption of operations will depend on the evolution of weather conditions in the coming days and the recovery of threshing conditions. The yield remains stable at 23.6 quintals per hectare (qq/Ha), maintaining the production forecast at 6.4 MTn.

SORGHUM: Finally, the grain sorghum harvest continues to progress, reaching 18.5% of the suitable national area after a two-week increase of 3 percentage points, with an average yield of 46.8 quintals per hectare. However, harvesting operations remain delayed due to the aforementioned rains in areas such as north-central Santa Fe and east-central Entre Ríos, where progress had been concentrated. Regarding crop development, most of the area is in the final stages of grain filling and, in general, presents a crop condition ranging from Normal to Excellent, allowing the production forecast to remain at 2.9 million tons.

Source: Buenos Aires Grain Exchange