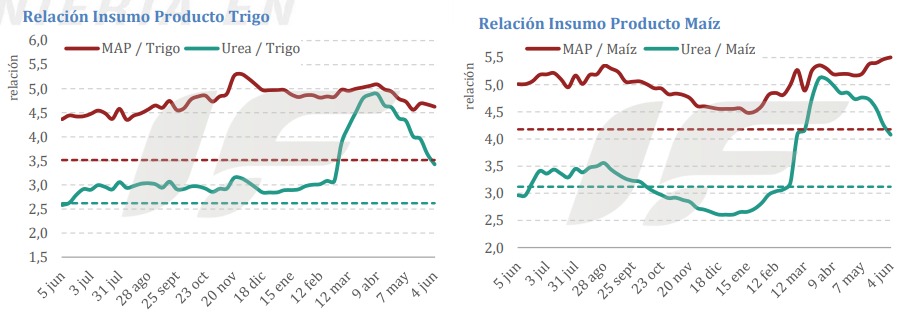

Urea import demand in Argentina remains extremely depressed, and the market is described as sluggish. Buyers are holding back, waiting for lower prices amid a global context of very weak demand.

“Urea prices for Argentina have fallen again. This week, prices are estimated to be in the range of US$590 to US$600 per ton CFR, but no deals have been finalized,” states the weekly report from the consulting firm IF Ingeniería en Fertilizantes.

The last turning point occurred in mid-April, when tensions in the Middle East and a tender in India boosted prices, reaching a peak of US$850 to US$870 per ton CFR in Argentina. Comparing that peak with current levels, the Argentine market has experienced an uninterrupted decline of between US$260 and US$270 per ton CFR in less than two months.

“Meanwhile, local prices also continue their downward trend. Argentine producers are postponing their purchase decisions until crop demand requires them, putting more pressure on supply, which is trying to generate demand by offering increasingly competitive prices, but without finding any interest at the moment,” the report notes.

The price range for urea in the Argentine wholesale market was US$760 per ton at the beginning of the week, while at the end it was trading in a range of US$720-740 per ton.

As for phosphate fertilizers, import demand in Argentina remains stagnant, although availability is tight. Offers from international suppliers remain in the range of US$910 to US$920 per ton CFR.

“Importers are reluctant to operate at current price levels, considering them unviable compared to local prices, which Argentine farmers are unwilling to accept. Instead, they are opting for a significant reduction in application rates, focusing their strategies on lower-cost starter fertilizers,” the report states.

In this context, some offers for monoammonium and diammonium phosphate (DAP and MAP) in the Argentine wholesale market have fallen to US$970-1000 per ton, in an attempt to stimulate demand, which remains stagnant despite the ongoing winter crop planting season.

“Argentine wholesale market prices are currently between US$100 and US$130 per ton below import parity. This tremendous price distortion is occurring in a very particular and unprecedented context: ‘old’ inventories with a cost that allows sales at current price levels,” the document points out.

“The question we ask ourselves week after week is: what will happen to prices in the Argentine market when the ‘cheap’ inventories are liquidated? The international market seems to offer no respite with the crisis in raw material costs for phosphate fertilizer production. Sooner or later, everything seems to indicate that local prices in Argentina will inevitably have to align with import parity,” it warns.

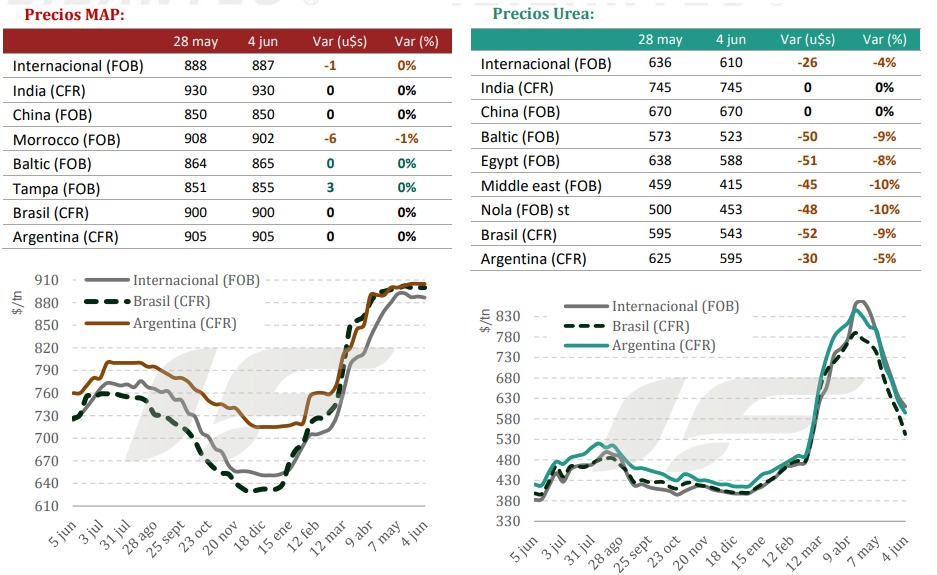

Regarding the global nitrogen fertilizer market, it continued to experience a sharp downward trend and a generalized deterioration in prices, heavily pressured by the confirmation of the return of Chinese exports and the almost total absence of buying interest worldwide.

All market attention remains focused on the NFL’s tender for 1.7 million tons of corn, which closes on June 8. “However, the market anticipates that this volume will be insufficient to absorb the increase in global supply. Adding to this, India has lowered its monsoon forecasts due to the risk of El Niño, creating uncertainty about the strength of its future agricultural demand,” the report explains.

In Brazil, importers remain on the sidelines, postponing purchases for the “safrinha” corn harvest in anticipation of further price declines. Import values continue to fall, with confirmed deals at US$520/ton CFR and a general range estimated at US$520-565/ton CFR.

In the US, barge demand in New Orleans (NOLA) has fallen sharply due to a lack of demand for hedging applications, with much of the traded volume destined for re-export.

“The main bearish catalyst was the clarity on China’s export quotas. Shipments are expected to resume this month, with allocations totaling between 2.0 and 2.6 million tons (and even up to 3.0 million). Minimum export prices have been set at around US$660/ton FOB for prilled urea and US$670-680/ton FOB for granulated urea, although the international market is already undercutting those levels,” the report highlights.

Meanwhile, the global phosphate fertilizer market remains in a prolonged stagnation, caught between a sharp decline in demand and a raw material cost crisis that continues to stifle factory production capacity.

Sulfur and sulfuric acid prices continue to rise due to the production and logistical crisis caused by the war in the Middle East, putting significant pressure on phosphate producers’ margins and limiting the availability of new shipments.

Chinese exports remain blocked. In its domestic market, DAP and MAP prices continue to climb, driven solely by rising sulfur costs, with no prospect of resuming international sales in the short term.

“India was practically the only driver of activity this week. The Indian Potash Limited (IPL) consortium purchased 100,000 tons of DAP and 100,000 tons of triple superphosphate (TSP) from the Moroccan producer OCP for shipment between June and July,” the report states.

Liquidity in Brazil was nonexistent, severely impacted by the Corpus Christi holiday and importers’ continued refusal to accept high prices. The MAP (Marine Agricultural Portion) has a reference import value of US$900/ton CFR.

In New Orleans, USA, activity slowed as buyers opted to sell surplus spring volumes rather than commit to new summer filling positions. DAP (Double Agricultural Portion) barges fell to US$780-790/ton FOB, and MAP followed suit, settling between US$795 and US$810/ton FOB.

Source: Valor Soja

Farm groups press U.S. Commerce Secretary to scrap Moroccan phosphate duties

A coalition of 65 state and national farm groups has urged U.S. Commerce Secretary Howard Lutnick to revoke countervailing duties on phosphate fertilizer imported from Morocco, arguing the tariffs are deepening a cost squeeze on growers as fertilizer prices reach fresh highs.

The letter, sent June 1 and signed by groups including the National Corn Growers Association, asks Lutnick to end the order “to ease the pain felt by farmers as fertilizer prices reach new highs.” The duty on Moroccan phosphate currently runs at about 16.6% to 16.8%, after starting at 19.97% in 2021, falling to 2.21% following a court remand, and then being raised again in a later review.

The groups cited a Texas A&M University Agricultural and Food Policy Center study estimating the duties on Moroccan phosphate added roughly $6.9 billion to input costs for U.S. corn, soybean, wheat, rice, sorghum and cotton growers across the 2021 through 2025 seasons. At its full 19.97% rate, the duty raised the U.S. price of diammonium phosphate by an estimated 28.6%, the letter said.

“Net farm income has fallen roughly 31% from its 2022 peak, fertilizer prices are up more than 150% since 2020, and Chapter 12 farm bankruptcies have surged to their highest levels in several years,” the letter said, noting growers are in a fourth straight year of losses.

The appeal lands less than a week after Federal Trade Commission Chairman Andrew Ferguson announced an industry-wide investigation into fertilizer pricing and market concentration. Mosaic controls roughly three-quarters of domestic phosphate production, while Morocco’s state-owned OCP is the main exporter subject to the order. A decision on whether to revoke the duties rests with Commerce.

Source: DTN Progressive Farmer

Russia and Bangladesh sign major potash fertilizer supply deal

Russia and Bangladesh have signed a major agreement to supply more than 500,000 tons of Russian potash fertilizers, according to statements cited by TASS from the Russian Embassy in Dhaka. The deal was concluded between the Russian foreign trade association Prodintorg and the Bangladesh Agricultural Development Corporation.

The embassy described the agreement as the largest fertilizer-sector contract in the history of bilateral interstate cooperation between Russia and Bangladesh. It added that the Bangladesh Agricultural Development Corporation has been importing potash fertilizers from Russia for several years under earlier agreements with Prodintorg.

The new contract expands on existing trade flows at a time when Bangladesh continues to rely on imported fertilizers to support its agricultural sector.

Source: Fertilizer Daily

BRAZIL: Fertilizer deliveries grow 3,8% in the first quarter.

Volume delivered to the Brazilian market increased in the first three months of 2026, despite an unstable external environment.

Fertilizer deliveries to the Brazilian market totaled 9,76 million tons in the first quarter of 2026, a 3,8% increase compared to the same period last year, when 9,40 million tons were recorded. The data was released by the National Association for the Diffusion of Fertilizers (Anda).

In March alone, deliveries reached 2,83 million tons, an increase of 18,7% compared to the 2,38 million tons recorded in the same month of 2025.

Mato Grosso led fertilizer consumption during the period, accounting for 25,2% of the total delivered in the country, equivalent to 2,45 million tons. Goiás, São Paulo, Paraná, Minas Gerais, Mato Grosso do Sul, and Bahia followed.

Despite the growth in deliveries, the outlook for the sector remains challenging. According to Anda, factors such as international geopolitical instability, high interest rates, and difficulties in accessing credit continue to put pressure on the market and impact the purchasing decisions of rural producers.

National production: National production of intermediate fertilizers totaled 1,41 million tons between January and March, a decrease of 16,2% compared to the same period in 2025. In March alone, production was 483 tons, a 9,7% decrease.

According to the entity, changes in the corporate structure of companies and operational resumptions in some units may have hindered the complete consolidation of national production data for the period.

Imports: Imports of intermediate fertilizers totaled 8,15 million tons in the quarter, a volume 4% lower than that recorded in the same period last year. In March, however, there was a 10,1% increase in imports, which reached 2,74 million tons.

The port of Paranaguá, the main entry point for fertilizers in Brazil, received 2,12 million tons in the first quarter, a 13,5% decrease compared to the first three months of 2025. The terminal accounted for 26,1% of national fertilizer imports during the period.

Source: Cultivar Magazine

ARGENTINA MAIN CROPS OVERVIEW:

WHEAT: Wheat planting for the 2026/27 season continues accelerating across virtually the entire central and northern agricultural region, reaching a week-on-week increase of 18.2 percentage points and currently covering 32.4% of the projected 6.5 million hectares. Good water availability is allowing planting to proceed at an accelerated pace, exceeding the peak of the curve and placing it 12.4 percentage points above the average for the last five years and 8.8 percentage points above the previous cycle. Activity was concentrated primarily in the Northeast (NEA), North-Central Córdoba, and the Northern Core region, with regional progress between 27 and 41 percentage points in the last week. Also noteworthy is the planting progress in the southwestern agricultural region, which has already surpassed 20% at this point in the year for the second consecutive year.

SOYBEANS: After a week-on-week increase of 7 percentage points, the soybean harvest has reached 91.7% of the suitable area nationwide. Harvesting progress is 11 percentage points ahead of last season and 7.4 percentage points ahead of the average of the last five seasons. To date, the national average yield stands at 32 quintals per hectare (qq/Ha), exceeding by 2% the average of the five best seasons recorded by the PAS series and positioning itself as the second-best historical record. Harvesting is concentrated in the southern part of the agricultural area, where yields are below average and work remains delayed, while in the northern part of the agricultural area, results remain above the average of the last five seasons. Regarding second-crop soybeans, with 81% harvest progress, the average yield is 26.5 qq/Ha. Under this scenario, we maintain our production forecast at 50.1 million tons (MTn).

CORN: The commercial grain corn harvest is progressing across 40.6% of the suitable area nationwide, with an average yield of 82.7 quintals per hectare (qq/Ha). The highest yields recorded so far are in the Northern Core, Southern Core, and Northern La Pampa-Western Buenos Aires regions, with averages ranging between 94 and 100 qq/Ha. In particular, Northern La Pampa-Western Buenos Aires is registering an average yield of 94.6 qq/Ha, a record for the PAS series in the region. Regarding late-planted crops, 96% of the area has already reached physiological maturity, while grain moisture continues to gradually decrease. If current conditions persist, we expect more land to be harvested in the coming weeks. Given this scenario, we maintain our production forecast at 64 million tons (MTn).

SORGHUM: Finally, the grain sorghum harvest continues to progress, reaching 49% of the suitable national area after a two-week increase of 14.5 percentage points, with an average yield of 44.6 quintals per hectare. As harvesting spreads across the main producing regions, the results obtained continue to support our production forecast. Regarding crop development, almost the entire remaining area is at physiological maturity and awaiting adequate moisture conditions to proceed with harvesting

Source: Buenos Aires Grain Exchange