The global fertilizer market has shifted from discussing prices to assessing product availability. With fewer available tons, greater logistical risk, and uncertain replenishment costs, prices appear to have no ceiling in the current situation.

“First, India absorbed global liquidity with an allocation of 1.3 million tons of urea, setting a new price floor. Then came the real shock: the escalation of the conflict in the Middle East, which deepened the supply constraint, disrupted logistics, and triggered a global price hike,” notes the weekly report from the consulting firm IF Fertilizer Engineering.

“The focus is no longer on capturing specific value opportunities, but on managing supply risk in a context where each available ton has an increasing implicit cost,” the report emphasizes.

In the global nitrogen market, the inability to move volumes from the Gulf, along with cuts in Algeria and disruptions in Russia, maintains a scenario of limited supply. Despite a slight slowdown in demand, prices remain firm due to geopolitical uncertainty and a shortage of available product.

“India continues to evaluate its supply strategy and is delaying its market entry as it tries to secure gas supplies. A new urea tender is expected in the short term, which could put additional pressure on available supply,” the report notes.

China maintains export restrictions, prioritizing domestic supply, which exacerbates the current situation in the Middle East and North Africa, where supply remains heavily constrained by armed conflict, with withheld volumes, logistical difficulties, and production cuts in key countries such as Algeria and Iran.

Europe is experiencing moderate demand and sporadic purchases, with importers operating cautiously in the face of high prices. Some consumption is shifting toward nitrates as an alternative given the limited availability of urea.

“In the Americas, Brazil remains active but with low volume, while in the US, buyers are showing reluctance to extend their positions. In Argentina, offers remain at high levels with little buying interest, reflecting cautious demand focused on immediate needs,” the report explains.

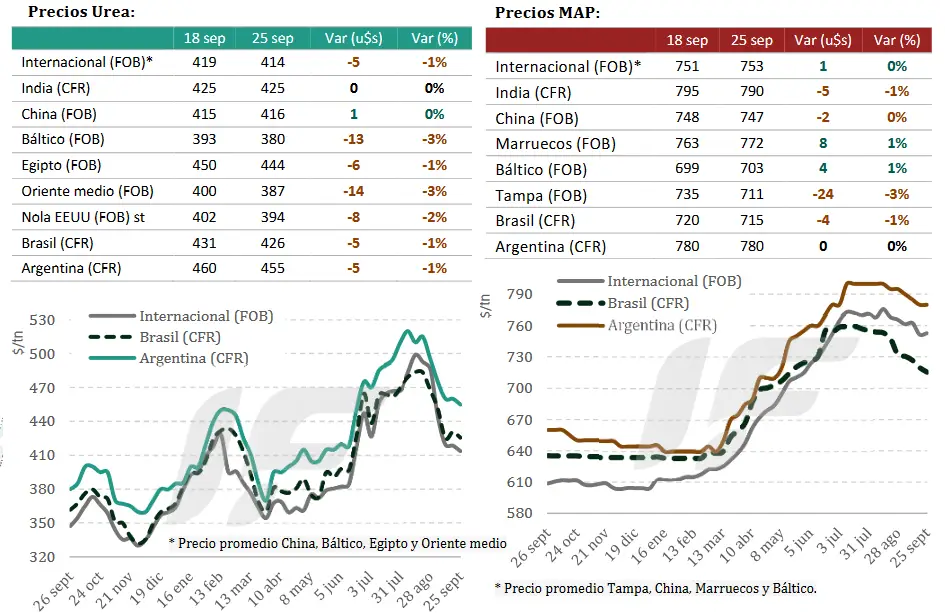

In Argentina, urea prices are indicated at US$780-800/ton, with wholesale references ranging between US$855 and US$920/ton.

“In recent weeks, there have been small rounds of business in the Argentine market where well-funded distributors took advantage of the international price increase to monetize inventory purchased before the conflict. This wasn’t a genuine recovery, but rather a tactical strategy: selling older stock, capturing margin, and replenishing cash flow. Producers are consulting and monitoring the price board, but are not committing to volume,” the report notes.

“The width of these bands reflects the fact that there isn’t a single price, but rather values constructed based on risk. Those who need to rotate stock position themselves at the bottom; those who prioritize covering replenishment position themselves at the top. The price board isn’t ordered by demand, but by risk perception. This logic generates a fragmented market, where short-term tactical operations coexist with defensive hedging decisions, without a clear reference signal to guide volume,” he points out.

In nitrogen fertilizers, Profertil’s production, along with recent imports, ensures a significant physical buffer. The risk isn’t related to stock levels, but to replacement cost: if demand reacts, the product will be available, but at higher costs that will push domestic prices to the upper end of the range.

Regarding the global phosphate market, the conflict in the Middle East continues to affect the logistics and availability of key raw materials such as sulfur, while China maintains its export restrictions, deepening the global deficit.

“Despite this scenario, demand is showing signs of caution in several markets, especially in Asia and Latin America, where high prices are beginning to limit activity. The market is entering a waiting phase, with purchases deferred but not canceled, while supply risks accumulate,” indicates IF Fertilizer Engineering.

India continues to experience subdued demand awaiting decisions on government subsidies, which is slowing imports despite high prices and negative margins for producers. Meanwhile, stocks are relatively high, and local production is decreasing due to maintenance and costs.

Meanwhile, China deepened its suspension of phosphate exports, including triple superphosphate (TSP), eliminating a key source of global supply. Production is also affected by input constraints, especially sulfur.

In the Middle East, logistics remain severely disrupted, with restrictions on passage through the Strait of Hormuz limiting shipments from Saudi Arabia. Morocco faces uncertainty regarding its sulfur supply, although it is currently maintaining its export pace.

Europe is experiencing record high prices with moderate demand and sporadic purchases, while in the Americas, the market shows signs of cooling demand in the face of high prices.

In Brazil, there is a clear pullback in buyers and low liquidity, with importers postponing decisions while awaiting better conditions. In Argentina, prices continue with a marked upward trend, with recent transactions at high levels and rising bids.

In Argentina, monoammonium and diammonium phosphate (MAP and DAP) are listed at US$850-880/ton CFR, with offers climbing to over US$900/ton, while wholesale reference prices range between US$915 and US$945/ton.

“In the phosphate sector, Argentina is entirely dependent on imports, and operators have adopted a defensive stance, avoiding new shipments due to price and freight risks. This means that the risk of phosphorus shortages for winter cereal planting is real, in a context where the available supply is not only more expensive but also more uncertain in terms of logistical lead times. The decision window is shrinking, and the cost of waiting is increasing,” the report warns.

“Therefore, supply will have to shift towards alternative sources and blends (SSP, TSP, NPS/NPS+Zn). Waiting for price drops means assuming the risk of running out of product,” it summarizes.

Source: Valor Soja

Argentine – Fertilizers Prices Rise by Up to 50%, Caution for Wheat Stocks

Argentina has sufficient fertilizer stocks to cover between 30 and 60 days, amidst a sharp rise in global prices driven by the conflict in the Middle East, according to data collected as of March 30, 2026. Companies in the sector assure that supply is guaranteed in the short term for the start of the wheat season, although they warn that the situation could become more complicated in the coming months and affect producers’ planning.

The current scenario combines immediate availability of inputs with growing uncertainty going forward. Part of the supply is sustained by local production—such as Profertil’s urea, which covers about 60% of the market—but the system depends heavily on imports. This makes the country especially vulnerable to any disruption in international trade.

In this context, the focus is beginning to shift toward the second half of the year. The local urea market, which is around 2.2 million tons, will need to bolster its external purchases at a time when operations are progressing slowly and the global scenario presents greater logistical and commercial risks.

Fertilizers: Prices rise by up to 50%, raising concerns about wheat stocks.

Meanwhile, the most evident impact is already being felt in prices. Urea has seen increases of up to 50% internationally, rising from around US$490 per ton to about US$665, while in Argentina it is around US$850. In the case of phosphate fertilizers, the increases range between 15% and 20%, in line with a global upward trend.

These increases are driven by structural factors. The conflict in the Middle East directly affects key trade routes: 34% of global urea exports and 12% of monoammonium phosphate exports pass through the Strait of Hormuz, amplifying the market’s sensitivity to any disruption.

This is compounded by higher energy and logistics costs, with gas prices in Europe rising by nearly 60%, maritime freight rates increasing by up to 70%, and reduced vessel availability. Meanwhile, Argentina maintains a significant dependence on the Gulf of Mexico, which supplies approximately 37% of its urea imports.

The impact of this situation is not limited to availability but directly affects producer profitability. Currently, with the same volume of grain, producers can purchase between 30% and 50% less fertilizer than the average of the last three years, which influences key management and technology decisions in the field.

Unlike other periods of crisis, demand remains more subdued. Many producers have not yet taken a position in the market, which is creating some tension in the supply chain due to the possibility of a concentration of purchases later on.

Industry representatives are beginning to recommend anticipating purchasing decisions and securing some of the inputs for the winter crop season. This is not only due to price levels, but also to guarantee availability at planting time, in a context where logistics and international trade continue to show high volatility.

Source: agrolatam

Yara cuts India fertilizer output as conflict in the Middle East disrupts gas supplye

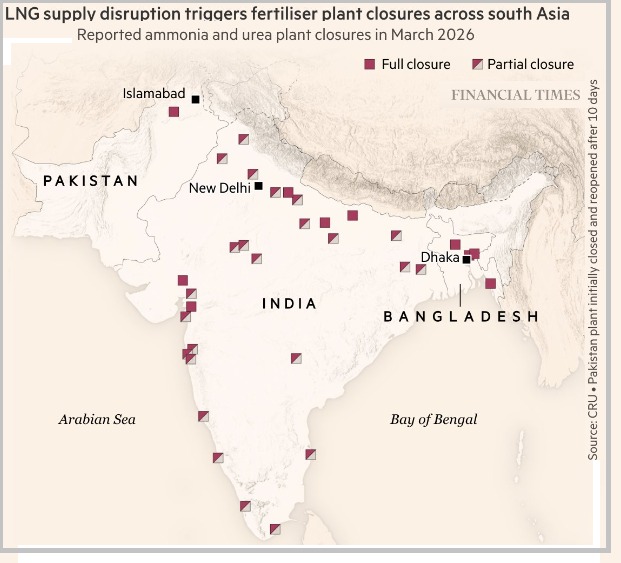

Yara International has reduced ammonia and urea production at its plant in Babrala, in the state of Uttar Pradesh, due to disruptions to natural gas supplies linked to the ongoing conflict. Chief Executive Svein Tore Holsether said the company was forced to curb output due to reduced availability of gas, a key feedstock, while some competitors in India have shut plants entirely.

India, a major importer of liquefied natural gas, has been particularly exposed to supply shocks following the suspension of a significant share of exports from the Persian Gulf. Qatar, one of the world’s largest LNG suppliers, has halted production, driving sharp increases in gas and fertilizer prices. Holsether warned that volatility in input costs is raising concerns about global fertilizer availability and farmers’ ability to afford essential nutrients, although Yara said the impact on its financial performance would remain limited.

The company is not currently considering production cuts in Europe, where higher urea prices have so far offset rising gas costs. Meanwhile, policy discussions are intensifying in the European Union over how to support agriculture. Istvan Nagy has called for easing restrictions on Russian and Belarusian fertilizer imports, a proposal the European Commission is reviewing. Yara has opposed the idea, arguing it could undermine Europe’s domestic industry and indirectly support Russia’s war effort, as the bloc prepares a broader Fertilizer Action Plan to strengthen supply resilience.

Source: Fertilizer Daily

Russia halts ammonium nitrate exports to secure domestic fertilizer supply

Russia’s Ministry of Agriculture has imposed temporary restrictions on exports of ammonium nitrate, suspending the validity of all issued and pending export licenses from March 21 to April 21, 2026. The measure is intended to ensure a sufficient domestic supply of the widely used nitrogen fertilizer as demand peaks during the spring field season. Shipments under intergovernmental agreements are exempt from the restrictions.

The decision was taken by the ministry’s operational headquarters, which is responsible for monitoring fertilizer distribution to agricultural producers. Authorities said the move comes amid rising international demand for nitrogen fertilizers and is designed to prioritize domestic deliveries, helping maintain stable planting operations and avoid supply disruptions for Russian farmers.

Source: Fertilizer Daily

Egyptian urea production continues to run despite gas shortages

Egyptian urea sales are still taking place for cargoes loading in April 2026, while production rates have remained unchanged as LNG deliveries continue to Egypt.

Israel’s suspension of gas exports following the outbreak of war with Iran has removed approximately one LNG cargo every four days from Egypt’s supply balance.

Egypt had secured three LNG cargoes for mid-March delivery before implementing broader energy-saving measures in the wake of the broader regional unrest. The government appeared focused on curbing domestic demand, rather than paying elevated spot prices, as it looks to preserve foreign currency reserves, contain inflation, and maintain supply stability.

Although urea plants have remained unaffected by the measures so far, producers acknowledge that the industry is not fully insulated from wider gas management policies, raising the risk that output could come under pressure if supply constraints persist.

Egyptian producers have reported selling about 260 000 t of granular urea for January – April loading so far in 2026, against potential export availability of 1.4 million – 1.6 million t over the same period.

In addition to the reported sales, Argus Media estimated that a further 200 000 – 250 000 t – or potentially more – of March-loading Egyptian urea has already been placed into India and the US. These volumes will help to narrow – but not eliminate – the sizeable gap between reported and potential exports and may point to comparatively high producer inventories or quantities sent to the domestic market.

Producers’ sales reported in 2026 include approximately 36 000 t for January loading, 80 000 t for February, around 84 000 t for March and about 60 000 t for April to date.

Domestic–export sales split

Egypt has 7.2 million – 7.3 million tpy of urea capacity and allocates a sizeable part of its output to the domestic market, leaving around 350 000 – 400 000 t/month for export.

The country exported an average of about 4.5 million tpy of urea in 2023 – 2025. The domestic season typically peaks in June – September.

Output fluctuates on both a monthly and annual basis, reflecting planned turnarounds, variations in gas availability – particularly during the summer peak power period – and intermittent disruptions to gas flows from Israel in recent years.

Source: World Fertilizer

ARGENTINA MAIN CROPS OVERVIEW:

SOYBEANS: As of this report, rainfall continues across much of the agricultural area, with localized intense events and some occurrences of excess soil moisture. As a result, for total soybean, the share of area under Adequate/Optimal soil moisture conditions increased by 4.2 percentage points week over week. Meanwhile, first-crop soybean harvest is becoming more widespread, with progress reaching 5% in the Southern Core and 9% in the Northern Core, where initial yields average 4.0 t/ha and 3.5 t/ha, respectively. In parallel, second-crop soybean shows a week-on-week improvement of nearly 3 percentage points in the Normal/Excellent crop condition category, supported by favorable moisture conditions, which are helping to halt the deterioration caused by thermo-hydric stress during the summer, particularly across both core regions. Under this scenario production forecast at remians 48.5 million tons.

CORN: Harvest continues to progress nationwide and, following a weekly advance of 3.8 percentage points, has reached 19% of the suitable area. Fieldwork maintains a good pace across much of the agricultural region, with a national average yield of 8.53 t/ha. As harvesting advances, strong yields continue to be reported across the main production regions, albeit with variability between areas. Regarding late-planted corn, most of the area is currently in the grain filling stage, while the earliest fields are entering physiological maturity in Southern Córdoba and both core regions, within a context where 73.1% of the area shows a crop condition between Good and Excellent, and 94.9% is under Adequate/Optimal soil moisture conditions. Recent rainfall has reinforced soil moisture reserves, although localized excesses have been reported in central and southern areas. Under this scenario, production forecast remains at 57 million tons.

SUNFLOWER: Despite abundant rainfall recorded shortly before the publication of this report, sunflower harvest progressed by 15.4 percentage points week over week, reaching 76.5% of the suitable area. Progress of between 26 and 37 percentage points was recorded across the southern agricultural belt, except in the southwestern region, where fieldwork was particularly delayed due to unsuitable field conditions. The national average yield shows a slight decline, currently standing at 2.37 t/ha, with regional results generally aligning with current projections in most cases, except in Southeastern Buenos Aires, where despite a wide yield range, the average remains a few quintals above initial estimates. Under this context, the production forecast is maintained at 6.4 million tonnes, although further adjustments cannot be ruled out..

Source: Buenos Aires Grain Exchange