July brings a certain amount of enthusiasm. According to the Rosario Stock Exchange, widespread rains gave wheat an “exceptional start.” Added to this is a fact that further excites the chain: corn planting intentions are growing in the core region.

The two crops together account for 65% of national fertilizer consumption, so the positive outlook translates into increased demand for nutrients.

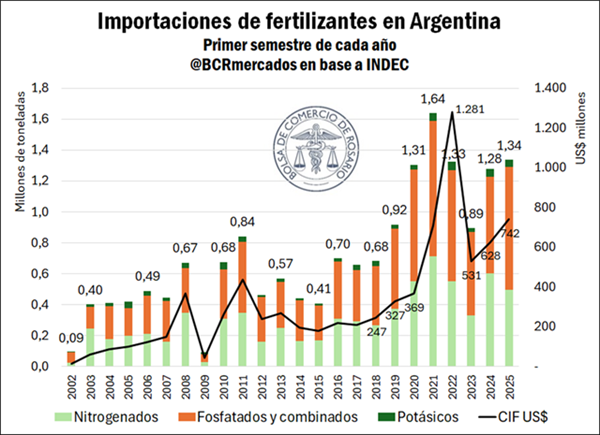

The same Rosario-based entity conducted a study predicting that 2025 could be a great year for the Argentine fertilizer market.

According to data from CIAFA (Argentine Chamber of the Fertilizer and Agrochemical Industry) and Fertilizar Asociación Civil, 81% of wheat crops received some type of fertilization in 2024. For corn, the proportion rises to 84% in the late season and 92% in the early season. Soybeans, which account for 17% of fertilizer consumption, also showed significant levels: 60% of first-season soybeans and 47% of second-season soybeans were fertilized last year.

With an optimal moisture profile and the recent drop in export duties, the outlook for fertilizer use is more than favorable. The economic incentive improves margins and, along with the weather, paves the way for a campaign with greater application of technology.

“With these expectations, fertilizer consumption in 2025 in Argentina could grow by around 7% compared to 2024 volumes,” the specialists stated. However, it should not be overlooked that the dynamics of nutrient prices, essential for agricultural margins, can modify domestic demand for fertilizers. This is especially true considering that more than 60% of the country’s fertilizer imports are concentrated in the second half of the year.

This optimism comes at a key moment for national agriculture. According to estimates by Fertilizar, the agricultural sector “owes” the soil approximately $30 billion in nutrient replacement, which was extracted season after season and not returned. The amount of fertilizer, translated into cash, results in this figure.

Import figures are beginning to reflect this, with the first half of 2025 seeing 4.5% more fertilizer imports than in the same period last year. While nitrogen fertilizers showed year-on-year declines, this decline was offset by an increase in purchases of phosphate and combination fertilizers, the latter made with more than one nutrient, such as nitrogen, phosphorus, and potassium.

With wheat planting underway and corn on the radar, the fertilizer sector is starting the campaign with a favorable wind. Now, everything will depend on continued favorable weather conditions and whether international and local prices slow the momentum.

According to Rosario experts, “with 1.34 million tons imported in the first half of 2025, we are facing the second-largest volume of fertilizer imports on record. Imports are valued at US$742 million. This represents an 18% increase in imported value.”

Imports in value grew faster than the increase in volume due to increases in average prices for all fertilizer groups.

A recent World Bank report attributes the rise in international prices to rising demand, trade restrictions (especially export restrictions in China), and production deficits, with particular emphasis on the urea market.

“The good news brought by the rains and soil moisture, along with the reduction in export duties, allows us to project this growth in fertilizer demand for the country. In this sense, replenishing soil nutrients in Argentina is essential to continue supporting agricultural yields and further increasing the country’s grain production,” the BCR summarized.

Source: Bichos de campo

Urea prices rise 29% at Brazilian ports, Limited supply, strong demand, and political uncertainty drive up fertilizer prices

Supply in the international nitrogen market remains tight. This situation, according to the weekly fertilizer report from StoneX, a global financial services company, has contributed to supporting prices in global trade.

At the same time, strong demand in India and the country’s acquisitions have been key drivers of growth in recent weeks. “India is currently holding a tender for the import of urea, which could involve up to 2 million tons of the product. Investors are closely monitoring this event, awaiting further price information to gain greater clarity on the intentions of the participants in this negotiation,” highlights Market Intelligence analyst Tomás Pernías.

According to Pernías, this tight supply-demand dynamic generally hinders a drop in nitrogen prices. In the United States, for example, Trump’s import tariffs have reduced the attractiveness of the North American market, inhibiting the entry of nitrogen fertilizers into the country.

“Therefore, the result has been limited supply following an application season marked by strong fertilizer consumption. Furthermore, in recent days, another factor has caused urea prices to soar in the country: the threat of new sanctions against Russia has raised concerns among buyers. Russia is among the main suppliers of urea to the US, and without its goods, the Americans would have to turn to other suppliers, which could make imports even more expensive,” explains the analyst.

Brazilian market is impacted by the global scenario

According to Pernías, this context of uncertainty has affected Brazil. Currently, Brazilian urea purchases have not been particularly strong, but as China continues to restrict its export flows of this fertilizer, the reduced international supply has kept prices relatively high in the country.

Furthermore, the threat that the US could impose sanctions on Russia—affecting countries that import Russian goods, such as Brazil—has raised concerns among Brazilian importers, as Russia is a major supplier of fertilizers to the country.

“Between the first days of January and the end of July 2025, an increase in urea prices at Brazilian ports of approximately 29% was observed, reflecting the tighter fundamentals in the international market. The appreciation of fertilizers is, in part, one of the factors responsible for the higher production costs faced by Brazilian farmers for the 2025/26 harvest,” concludes Pernías.

Source: Cultivar Magazine

Socar Carbamide aims for full production capacity in 2025

Socar Carbamide, a subsidiary of Azerbaijan’s state oil and gas company Socar, plans to reach its maximum annual production capacity of 660,000 tons of urea in 2025, according to Shohrat Mirzoyev, head of the plant’s production department.

The facility produced 652,000 tons in 2024, bringing it close to its design limit. Commissioned in January 2019, the plant operates on 435 million cubic meters of natural gas annually. The total investment in the project reached €800 million.

Socar Carbamide supplies both the domestic market and exports to other CIS countries and neighboring regions.

The company’s expansion in urea production aligns with Azerbaijan’s broader strategy to develop value-added fertilizer exports and strengthen its position in the regional market.

Source: Fertilizer Daily

Bangladesh issues DAP, TSP, MOP private-sector tender

Bangladesh’s agriculture ministry has issued a long-awaited private-sector tender to buy diammonium phosphate (DAP), triple superphosphate (TSP) and muriate of potash (MOP), closing on 5 August, as researched by Argus Media.

The Ministry has declared that it is seeking:

500,000t of DAP

200,000t of TSP

250,000t of standard MOP

20,000t of monoammonium phosphate (MAP)

The product must be shipped from loading ports by 20 September and delivered to Chattogram, Narayanganj, Nagarbari and Noapara.

Financing problems delayed the tender. Last year, the ministry issued the private-sector tender on 11 June, to close on 4 July. After failing to secure the full quantity at the initial tender, it continued to buy through private-sector tenders over the rest of 2025.

Source: World Fertilizer

ARGENTINA MAIN CROPS OVERVIEW:

WHEAT: In the last week, wheat planting progressed 2.4 percentage points, covering 98.3% of the projected area of 6.7 Mha. Rainfall of varying intensity across the entire agricultural area, but with greater concentrations in central Santa Fe, Entre Ríos, and Corrientes, has a variable impact. Water reserves in the north of the country are improving for the start of reproductive stages. In production centers, where the moisture content of the profile remains complete before planting, some producers report losses in the plant stand due to excess water, although not significant. However, 78.7% of the grain is developing under Adequate to Optimal moisture conditions, and 96.9% is in Normal to Excellent crop condition. Regarding phenology, only 3.8% of the standing wheat (concentrated in the north of the country) is in the stem stage or later.

CORN: The commercial grain corn harvest continues, reaching 88% of the estimated area nationwide, after registering a week-on-week increase of 4 percentage points. The average national yield remains at around 72.3 t/ha. In the province of Córdoba, harvesting is nearing completion in the north-central portion, with an average yield of 80.5 t/ha. Meanwhile, in the southern part of the province, 14% of the area remains to be harvested, with an average cumulative yield of 74.3 t/ha. In the province of Buenos Aires, delays persist, particularly in the central and southern areas, where even early crops remain to be harvested. However, yields recorded so far are within expected levels. Under this scenario, the national production projection remains at 49 metric tons.

SORGHUM: The grain sorghum harvest maintained a good pace, especially in the northern agricultural region. To date, 95% of the planted area nationwide has been harvested, with an average yield of 35.3 t/ha. Late plantings in the central agricultural region yielded better-than-expected results. Although a greater negative impact was anticipated due to the intense heat and water stress experienced toward the end of summer, yields were better than anticipated. This performance, coupled with a higher proportion of the crop in regions with good production potential, led to an upward revision of the production estimate by 100,000 tons, representing a 3.3% increase compared to the previous projection. In this context, the new national production projection is 3.1 metric tons.

Source: Buenos Aires Grain Stock