Current phosphate fertiliser prices in the Argentinian market appear to be final for the remainder of the 2025/26 crop year. In contrast, the price of urea is more volatile and depends on international variables.

This is indicated in the latest market report by the consulting firm IF Ingeniería en Fertilizantes. This week, the wholesale reference value of granulated urea was 515 USD/tonne, while for monoammonium phosphate (MAP) it was 845 USD/tonne.

“The local market is well supplied, with stable cost structures, particularly in the case of phosphorus. At a logistical level, there is a high frequency of ship arrivals carrying fertilisers. Added to this are delays in shipments, which could generate space limitations in some ports over the next 15 to 20 days”, the report points out.

‘In the international market, MAP is less available and DAP (diammonium) is more prevalent. This has led to a higher proportion of diammonium arriving on vessels. Consequently, some companies have limited MAP stocks, while DAP is more readily available, creating an increasing price gap between the two products,’ he adds.

Internationally, the market experienced a week of high uncertainty and low trading activity, dominated by anticipation of China’s return to the export market. ‘Although no official policy has yet been issued, various sources have confirmed meetings between Chinese authorities and major producers, fuelling speculation about exports. However, the ban on sales to India will remain in place, limiting the short-term impact,’ the document explains.

‘This scenario has prompted an immediate reaction from buyers, who are postponing purchasing decisions while awaiting greater regulatory and commercial clarity. The mere expectation of China’s return as a supplier has created downward pressure,’ it notes.

“This scenario has prompted an immediate reaction from buyers, who are postponing their purchases while awaiting greater regulatory and commercial clarity. The mere expectation of China’s return as a supplier has created downward pressure,” it notes.

The only significant sales were from Iran, which exported around 150,000 tonnes of urea to destinations including Brazil and various African countries. In Egypt and the Middle East, producers lowered their prices due to unwillingness to accept higher prices from buyers.

The US, however, saw the opposite market dynamics to the rest of the sector, with domestic prices holding steady or rising in the Gulf of Mexico due to active seasonal demand and supply constraints.

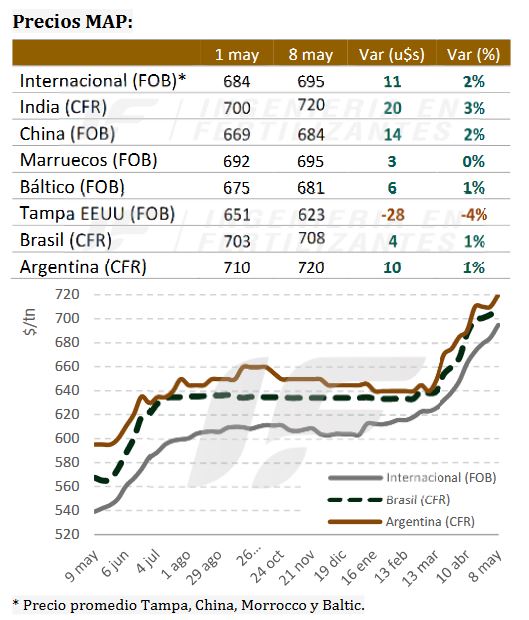

In the phosphates market, prices rose across the board, driven by limited export availability in China and strong demand in key markets such as India, Brazil and Ethiopia. “These factors coincided with tight supply and logistics constraints, contributing to a bullish tone across all regions”.

India completed multiple DAP trades with Saudi Arabia and Jordan at $700–720/tonne CFR due to concerns that China will withdraw as a supplier.

In the US, DAP and MAP values in the Gulf of Mexico continued to rise due to a combination of tight local supply, the impact of recent tariff measures, and renewed domestic interest.

Ethiopia emerged as a new market player by launching a major tender for 425,390 tonnes of DAP for delivery between May and June. This follows its recent purchase of 60,000 tonnes of Egyptian DAP at $670 per tonne FOB.

Brazil maintained its upward trend. Even without confirmed trades, MAP prices rose to $710/tonne CFR, reflecting firm demand ahead of soybean planting and the relative scarcity of supply. TSP quotes also increased significantly.

“The short-term outlook remains firm until China actually starts exporting. Shortages in India, the need for restocking in Brazil, and production limitations among some traditional suppliers are sustaining the upward bias of values, which could moderate from June onwards,” the consultant summarises.

Source: Valor Soja

Mexican Ministry of Agriculture distributes 70,000 tons of free fertilizer to over 157,000 producers

The Mexican Ministry of Agriculture and Rural Development (SADER) launched its 2025 Fertilizers for Well-Being program on May 9 in the State of Mexico, distributing free fertilizer to more than 157,000 producers of basic crops.

The initiative aims to deliver approximately 70,000 metric tons of fertilizer, including 24,000t of diammonium phosphate (DAP) and 46,000t of urea supplied by PEMEX. Distribution will be carried out through 69 Agriculture Distribution Centers (CEDA) located in key municipalities, with SADER staff managing the direct handover of fertilizer to eligible recipients.

The program prioritizes producers of staple crops such as corn, beans, rice, sugarcane, and others essential to the regional economy. Among the beneficiaries are over 56,000 women, reflecting the program’s stated commitment to advancing food sovereignty and preserving traditional agricultural practices.

According to SADER, the program will reach 233,400 hectares of farmland. Each producer may receive up to 300 kilograms of fertilizer per hectare, with support capped at two hectares per person—translating to a maximum of 12 bags of 25kg fertilizer.

Allocations vary by crop. Corn, rice, prickly pear, wheat, and sugarcane producers will receive four bags of DAP and eight of urea. Bean growers will receive four bags of each, while producers of crops such as amaranth, oats, peanuts, coffee, barley, chia, and sunflower will be allocated six bags of each type.

The federal government under President Claudia Sheinbaum Pardo has framed the fertilizer program as a constitutional right, part of a broader agenda to reduce rural inequality and improve equity in agricultural development.

Source: Fertilizer Daily

ARGENTINA MAIN CROPS OVERVIEW:

SOYBEANS: Following a significant week-on-week progress of 21 percentage points, 44.9 % of the suitable area has been harvested nationwide, with a year-on-year delay of only -2.8 percentage points. The national average yield stands at 3.24 Ton/Ha, exceeding the 2.97 Ton/Ha recorded during the 2023/24 season. With 53 % of first-crop soybeans harvested, the average yield is 3.33 Ton/Ha, with results surpassing initial expectations particularly in Córdoba, both core production regions, and the Central-Eastern area of Entre Ríos, confirming the upward trend anticipated in previous reports. Regarding second-crop soybeans, with 21 % of the area harvested, early lots in both core zones are also showing higher-than-expected yields, a trend that is also observed in Entre Ríos and the North of La Pampa-Western Buenos Aires. Given this favorable scenario, the national production estimate has been revised upward by +1.4 million tons, reaching a total of 50 million tons for the current season.

CORN: Harvest operations progressed ahead of the rainfall recorded in recent days, reaching 34.9 % of the suitable area, with an average yield of 8.18 Ton/Ha. The cumulative volume to date totals 20.1 MT, exceeding last season’s collection at this time by 4.9 MT, primarily driven by a higher proportion of early plantings. Simultaneously, late corn harvest has just begun in Córdoba province, where early yields exceed 8.5 Ton/Ha. Once soybean harvesting concludes, these harvest activities are expected to become more widespread. In this context, the national corn production estimate is maintained at 49 MT, which represents a decrease of 1 MT compared to the average of the past five agricultural seasons.

SUNFLOWER: Although a few standing fields remain that will not affect the current estimate, the 2024/25 harvest is now considered complete, following the collection of the remaining area in Buenos Aires and La Pampa. The results obtained in this campaign position the 2024/25 season as the highest in terms of both yield (2.34 Ton/Ha) and volume produced (4.7MT), surpassing the five-season average by 12.8 % and 26.3 %, respectively.

SORGHUM: Harvest has progressed by 10.3 percentage points, reaching 35.3 % of the national suitable area, which reflects a yearover-year advance of 7.4 percentage points. Yields recorded to date average around 38.4 qq/Ha (3.84 Ton/Ha). However, a significant portion of the remaining area still needs to be harvested in lower-potential regions affected by thermal and water stress, as well as in late-planted fields in the central part of the country, which also show reduced yield prospects. For this reason, the national average yield is expected to decline as harvest progresses. Under this scenario, the production estimate is maintained at 3 million tons, aligning with the average of the last five seasons.

Source: Buenos Aires Grain Stock