The prices of phosphate fertilizers in the international market continue to show a clearly downward trend due to the weakness of demand from India and exporting nations trying to generate business in countries reluctant to do business.

“With Asia and part of Latin America operating with moderate purchases and coverage already assured, competition between suppliers put pressure on manufacturers in the Middle East and North Africa, while Europe and Southeast Asia maintained reduced activity. The market remains fragile, with high stocks, reduced final demand and greater exportable availability,” says the weekly report from the consulting firm IF Engineering in Fertilizers.

“In India, port inventories and the lack of clarity about subsidies decreased interest in new purchases. Few operations were observed, focused on some offers of monoammonium phosphate (MAP) and a specific sale of diammonium phosphate (DAP),” he adds.

In Brazil, the market continues to be conditioned by high stocks of MAP in the Paranaguá terminals, low commercial fluidity and a marked shift in demand towards simple super phosphate (SSP). “Significant volumes of SSP were traded in Brazil and one fertilizer company even exported MAP to Canada due to the weakness of the local market,” the report comments.

In Argentina, the input/output ratio continues at historically high levels, which supports a defensive posture between importers and distributors, prioritizing low inventories despite the international decline and maintaining contained local demand.

Regarding the nitrogen fertilizer market, it went through a week with mixed signals: firmness in the eastern hemisphere due to the impact of the next tender in India and the recovery of export activity in China, while in the west a certain weakness persists associated with adverse weather conditions, an abundance of pending shipments and less urgency to purchase.

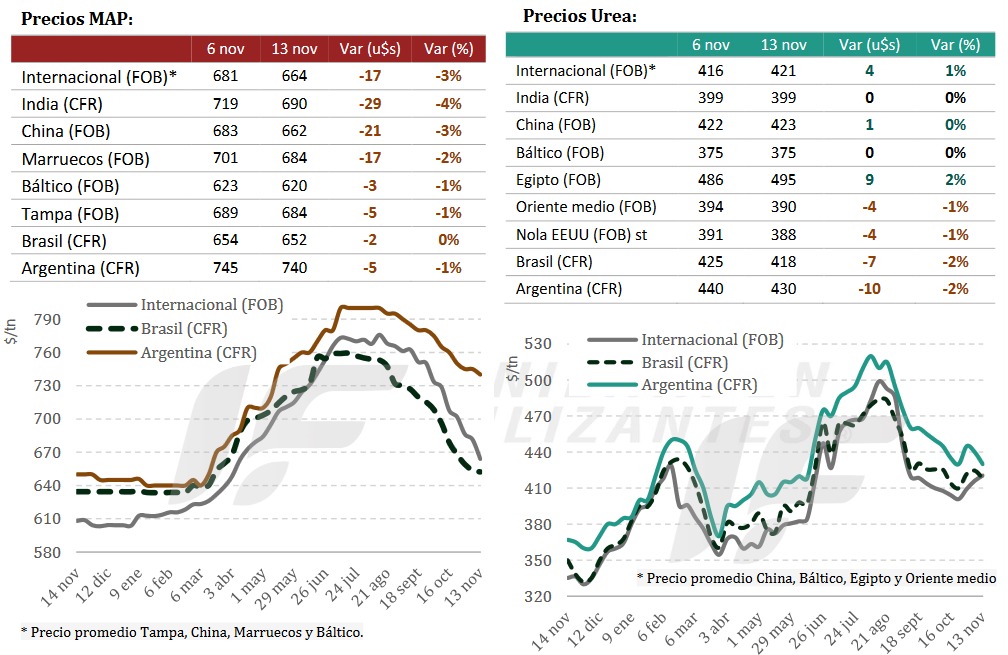

MAP and Urea Price List (November 6-13)

| Orign / Condition | 6 nov | 13 nov | Var (US$) | Var (%) |

|---|---|---|---|---|

| International (FOB)* | 681 | 664 | -17 | -3% |

| India (CFR) | 719 | 690 | -29 | -4% |

| China (FOB) | 683 | 662 | -21 | -3% |

| Morocco (FOB) | 701 | 684 | -17 | -2% |

| Báltic (FOB) | 623 | 620 | -3 | -1% |

| Tampa (FOB) | 689 | 684 | -5 | -1% |

| Brazil (CFR) | 654 | 652 | -2 | 0% |

| Argentina (CFR) | 745 | 740 | -5 | -1% |

Europe continues to be a focus of logistical tension due to the accumulation of urea stocks in ports and the anticipated coverage against the entry into force of the Carbon Border Adjustment Mechanism (CBAM) as of January 1, 2026, which will make the import process of this input in the EU-27 extremely complex.

“In India, the announcement of a new tender by the IPL corporation for 2.5 million tons of urea generates expectations and conditions sales decisions in multiple origins. The call will absorb a relevant portion of the supply from the Middle East, China and Russia,” he points out.

“In China, the release of new export quotas coincides with plants operating at high levels and internal stocks that are beginning to decline. Producers remain cautious, limiting external sales while they wait for the signal from the Indian tender,” he points out.

In the Baltic region, Russian shipments are preferably directed towards Europe, although some continue to go towards Latin America and a relevant participation is also expected in the Indian tender.

In Egypt, producers adjust positions after several weeks of intense activity and face a slower pace of purchases from Europe.

Meanwhile, in Brazil, demand is weakening due to delays in planting and a greater share of ammonium sulfate, while in Argentina the market is firmer after new purchases and greater activity from importers, in a well-supplied regional context, but with attention focused on the late corn planting window.

Source: Valor Soja

China reduces MAP and DAP exports, putting pressure on the market.

Chinese shipments fall 23%, altering global flows; restrictions increase competition among importers, including in Brazil.

Chinese exports of MAP (monoammonium phosphate) and DAP (diammonium phosphate) fertilizers have fallen to their lowest levels in recent years, according to StoneX, a global financial services company. Between January and September 2025, China shipped 3,7 million tons of these phosphates, a volume 23% lower than that recorded in the same period of 2024. The decline occurs at a time of stricter control over foreign sales by the Chinese government, a common practice before the domestic peak season, but which is proving more restrictive in this cycle.

According to market intelligence analyst Tomás Pernías, the data confirms that the Asian country is more aggressively reducing its exports. “China already tends to limit exports to protect domestic supply, but in 2025 the intensity of the restrictions surpasses that of previous years, which has increased the concern of international buyers,” he states.

The country’s importance to global trade reinforces the warning. Estimates indicate that, in 2024, approximately 16% of global exports of MAP, a fertilizer also widely used in Brazil, originated in China. Alongside Morocco, Russia, and Saudi Arabia, the country is among the main international suppliers. The reduction in its share creates additional tensions for importers, especially those most dependent on these flows.

In the Brazilian case, the impact is indirect, since only 4% of the MAP imported by Brazil in 2024 originated from China, with the majority coming from Russia, Saudi Arabia, and Morocco. Even so, when China restricts exports, global demand shifts to other suppliers, increasing competition for cargo and raising competitiveness among markets.

“When Chinese volumes disappear from the market, buyers from different regions start looking for the same suppliers. This sudden change puts pressure on prices and reduces the predictability of negotiations,” Pernías notes.

Brazil is also experiencing a period of lower MAP imports in 2025, reflecting high raw material prices and unfavorable terms of trade in recent months. In this scenario, Brazilian producers have increased purchases of SSP (single superphosphate), a less concentrated fertilizer that, at various times, has offered a better cost-benefit ratio.

Source Cultivar Magazine

Cinis Fertilizer will stop its Sweden plant for overhaul amid weak market conditions

Cinis Fertilizer will temporarily suspend production at its potassium sulfate plant in Köpmanholmen, Sweden, in mid-November to carry out an extensive technical overhaul aimed at boosting production capacity and operational stability. The shutdown is expected to last four to six weeks, the company said.

The decision coincides with a period of subdued market demand and lower fertilizer prices, which, together with higher raw material costs, have put pressure on the company’s margins. The production halt will enable the implementation of technical improvements designed to enhance process efficiency and environmental performance.

Planned upgrades include increased cooling capacity to improve production stability and volumes, as well as the installation of a new filter system to reduce dust emissions and improve the working environment.

“This is good timing to conduct plant improvements given the seasonality of the fertilizer market,” said Jakob Liedberg, chief executive and founder of Cinis Fertilizer. “A short stop of production provides an opportunity for us to concentrate on implementing planned improvement measures with our own staff and external parties.”

Cinis Fertilizer is also conducting a strategic review focusing on reducing input material costs, increasing production efficiency, and improving finished goods pricing.

The company will release its third-quarter interim report on November 13, 2025, and said it expects to provide an update on the review when available.

Cinis Fertilizer, listed on Nasdaq First North Growth Market, produces potassium sulfate (SOP) using recycled materials from the battery and pulp industries. Its patented process uses about half the energy of conventional production methods and generates fertilizer with a lower carbon footprint.

Source Fertilizers Daily

ARGENTINE MAIN CROPS OVERVIEW:

SOYBEAN: Soybean planting advances nationally, covering 12.9% of the 17.6 million hectares projected for the 2025/26 campaign, after a weekly progress of 8.4 percentage points. However, it presents a year-on-year delay of -7.4 p.p.

CORN: While waiting for the start of late planting, 76% of the total planted report a condition between Good and Excellent, compared to 29% reported the previous season.

SUNFLOWER: After a week-on-week progress of 12.9 p.p. Planting covers 84.5% of the projected 2.7 MHa. 100% of the oilseed maintains a Normal to Excellent crop condition and 27% transitions from flower bud onwards.

WHEAT: The harvest marked an interweekly progress of 4.9 p.p., covering 16.5% of the suitable area. The national average yield amounts to 26 qq/Ha, and the expected yield continues to increase. We update our projection to 24 MTn.

BARLEY 78% is filling grain, with a good general condition, although with specific effects due to frost, waterlogging and diseases. Despite this, above-average yields are expected, with a projected production of 5.3 MTn

Source: Buenos Aires Cereal Exchange