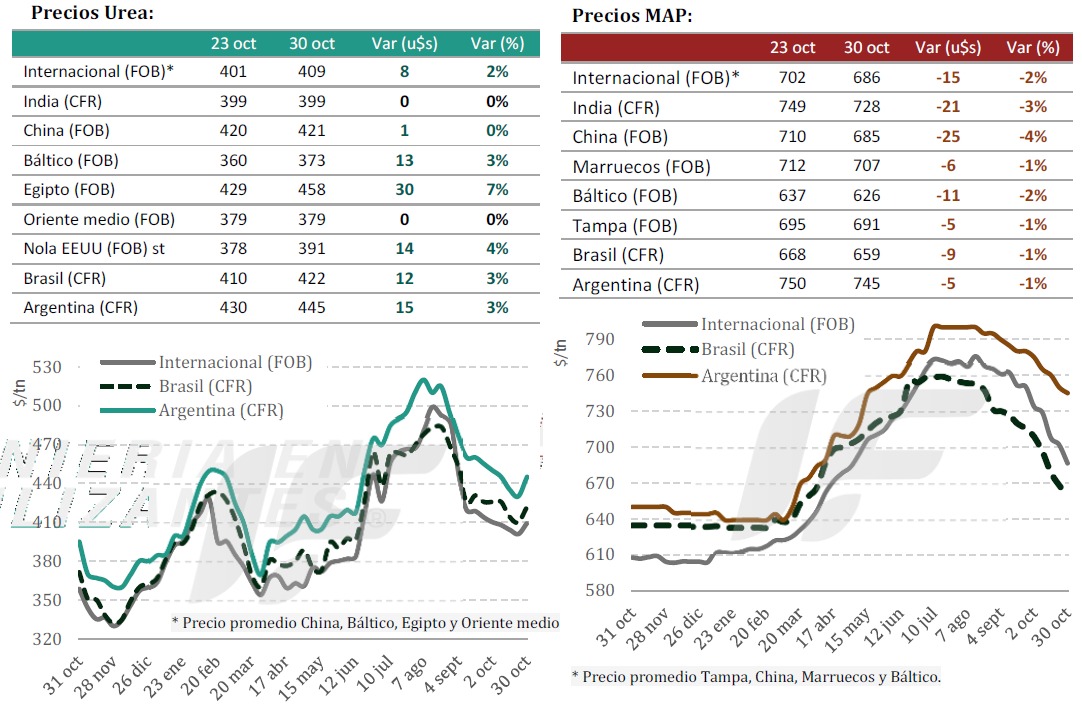

The downward trend in international nitrogen fertilizer prices reversed this week due to increased demand in key markets.

This week, the Indian corporation Rashtriya Chemicals and Fertilisers (RCF) purchased 430,700 tons of granulated urea in an international tender. Of this amount, 90,000 tons are destined for the east coast of India at US$395/ton CFR, and 340,700 tons for the west coast at US$402/ton CFR. A new tender is expected in mid-November, according to the latest report from the consulting firm IF Fertilizer Engineering.

The European Union remains a significant source of demand due to regulatory issues, as the Carbon Border Adjustment Mechanism (CBAM) will come into full effect on January 1, 2026, further complicating the import process for this input within the EU-27.

In the Baltic region, urea prices ranged from US$365-393/ton FOB, with producers prioritizing shipments to Europe and the US. Spot sales in Egypt reached US$445-465/ton FOB, and in Algeria, prices reached US$470-480/ton FOB.

The Brazilian market remained strong, with imports at US$420-430/ton CFR, driven by recovering demand due to the progress of soybean and corn planting.

In Argentina, prices settled at US$440-450/ton CFR, driven by strong global demand and reduced local supply due to the maintenance phase at the local urea plant (Profertil).

Conversely, the global phosphate market continued its downward trend due to seasonally weak demand and the impact of India’s new subsidy program, which has yet to generate sufficient incentives to improve importers’ margins in that Asian nation.

Chinese exports are virtually at a standstill following the closure of official quotas, but suppliers in North Africa and the Middle East continue to make shipments steadily.

“The combination of high stocks in Asia and Europe, along with reduced Chinese supply, points to a slowdown in the downward trend toward the end of the year,” projects the IF Ingeniería en Fertilizantes report.

Source: Valor Soja

Global fertilizer market enters another contraction.

Rabobank forecasts a drop in demand in 2025 and a sharper slowdown in 2026, driven by high prices.

The international fertilizer market is entering a new phase of contraction, as rising prices begin to weigh on global demand. This assessment comes from Rabobank, in an analysis signed by Bruno Fonseca, the bank’s sector analyst for inputs, released today (November 3).

According to the study, this cyclical shift, already predicted in a projection released in April, is now confirmed by the continued decline in the fertilizer accessibility index, an indicator that measures the relationship between price and the producer’s purchasing power. Although some regions still show resilience, the overall trend points to a weakening of demand in 2025 and a more pronounced slowdown in 2026.

The 12-month moving average of the index has already moved into negative territory, which, according to Rabobank, confirms the start of a new downturn, similar to the contraction recorded in previous periods.

The regional market dynamics remain volatile. In the United States, geopolitical tensions and trade tariffs are expected to weigh on the cost of agricultural inputs. In Europe, the Carbon Border Adjustment Mechanism (CBAM) is likely to further increase prices. In Brazil, producers face tight margins and credit restrictions, although fertilizer deliveries could reach record levels in 2025.

China remains focused on domestic supply, reducing exports, while India continues to influence the global urea trade through its auctions, which set international prices.

Urea, phosphates and potassium

Urea consumption is expected to decline in 2026, following recent sharp price increases. In Brazil, this trend is already being felt with the partial substitution by the use of ammonium sulfate.

Phosphate fertilizers are also facing high prices, which should lead to a 4% drop in global consumption in 2025, with further reductions projected for the following year. The decline in Chinese exports has been partially offset by increases in shipments from Morocco and Saudi Arabia, but the total trade volume remains subdued.

Regarding potassium, consumption recovered in 2024, driven by falling prices. However, the trend is for a further slowdown in 2025, with prices rising again. Brazil is expected to increase imports and may offset some of the reduced demand in other regions, but if high prices persist, global consumption could fall again in 2026.

Source: Cultivar Magazine

Fertilizers in Argentina: Corn Leads Consumption and Import Dependence Grows

More than half of the fertilizers used in the country are imported, while corn accounts for 38% of total consumption, according to the Córdoba Grain Exchange.

The fertilizer market in Argentina is going through a crucial phase in which corn is consolidating its position as the main consumer, while the country remains heavily dependent on imports to sustain its agricultural productivity.

According to the most recent economic report from the Córdoba Grain Exchange (BCCBA), 38% of total fertilizer consumption corresponds to corn, followed by wheat and regional crops, which also show a growing share.

The Córdoba-based organization highlighted that fertilizer use is a direct indicator of investment in technology and soil management, key to maintaining yields in a context of tight international prices and competitiveness challenges.

The report warns that 56% of the fertilizers used in the country are imported, a proportion that reflects both the sustained demand from the agricultural sector and the limited national production capacity.

Among the main countries of origin for these imports are Morocco, China, the United States, and Peru, which supply a significant portion of the inputs used by Argentine producers.

“The local supply of nitrogen fertilizers covers only a portion of domestic demand. Urea continues to be the most in-demand product,” the BCCBA report details.

Currently, nitrogen fertilizers represent 68% of national production, while phosphate and potassium fertilizers are almost entirely imported. This situation leaves the country exposed to the volatility of international prices and logistical fluctuations at the ports of origin.

The 2024/2025 growing season confirmed the leading role of corn in fertilizer use. Its expansion in planted area, along with the pursuit of higher yields per hectare, has driven record input consumption.

Corn accounts for more than a third of the national total, reflecting producers’ commitment to greater nutrient use efficiency and practices that support crop rotation in the face of soybean expansion.

Wheat remains the second largest consumer, especially in regions such as central and southern Córdoba, northern Buenos Aires, and the coastal region. Meanwhile, regional crops (such as peanuts, sugarcane, and legumes) are also experiencing increasing use, reflecting the country’s productive diversification.

Internationally, China continues to be the leading producer and consumer of fertilizers, followed by Morocco, the United States, Russia, and Brazil. These countries account for a significant portion of the global input trade, in a market where prices and availability are affected by geopolitical conflicts and export policies.

The BCCBA report underscores the need to strengthen local production and optimize fertilizer use, both to reduce external dependence and to improve the sustainability of Argentine agricultural systems.

“The challenge lies in balancing productive efficiency with environmental sustainability, promoting strategies that encourage rational and responsible fertilization,” the organization concludes.

Source: AgroLatam

ARGENTINE MAIN CROPS OVERVIEW:

CORN: Corn planting for grain production advanced 1.2 percentage points, reaching 35% of the projected area nationwide. In the central agricultural region, early planting is practically complete, while some areas in central and southern Buenos Aires province still need to be planted. In these areas, excessive rainfall caused by last weekend’s storms has slowed the pace of planting, reducing the proportion of early plantings compared to previous seasons. Regarding the condition of already planted crops, most fields are in Normal to Good condition, reflecting adequate initial establishment in regions with favorable weather conditions. Meanwhile, in north-central Santa Fe province, the first fields are beginning to reach the tasseling stage (VT). However, most crops are currently in vegetative stages between V4 and V8.

CORN: Planting progress for corn intended for grain advanced by 1.2 percentage points, reaching 35% of the projected national acreage. In the central agricultural core, early-season planting activities are virtually completed, while acreage incorporation remains to be finalized in central and southern areas of Buenos Aires province. In these zones, excessive soil moisture (waterlogging), resulting from last weekend’s storms, has constrained the operational pace, leading to a reduction in the proportion of early-planted fields compared to previous crop seasons. Regarding the condition of the established crop, most fields exhibit ratings between Normal and Good, reflecting adequate initial establishment in regions with favorable weather patterns. Meanwhile, in North-Central Santa Fe, the first fields are entering the tasseling stage (VT). However, the bulk of the crop is progressing through vegetative stages ranging from V4 to V8.

SUNFLOWER: Sunflower planting has now reached 63% of the projected 2.7 million hectares, following a week-on-week increase of 11.8 percentage points. While the weekend’s rains caused some delays in central and western Buenos Aires province due to waterlogged soils, in the central and northern agricultural areas, where planting is practically complete but available moisture was becoming limiting, these rains proved beneficial for the development of the oilseed, especially in the 12.4% of the area that is transitioning from bud to flowering. To date, 81.4% of the standing area has adequate to optimal soil moisture, and 96.9% maintains normal to excellent crop conditions.

WHEAT: Wheat harvesting progressed by 3.1 percentage points week-on-week and now covers 8.4% of the suitable area. The advance of combine harvesters across the northern agricultural area continues to yield above-projected results, bringing the national average to date to 20.3 quintals per hectare. However, following the aforementioned rains, which covered practically the entire agricultural area, 23.4% of the wheat crop is currently experiencing temporary waterlogging, which is expected to subside in the coming days. Nevertheless, the focus of the analysis will be on evaluating the impact of the cold front that followed the rains, which moved across much of the southern agricultural region, currently in its critical period. Although current moisture levels could mitigate the impact of these events, the consequences will become clearer over the next few days. In this context, the production forecast remains at 22 million tons.

BARLEY: As mentioned previously, late frosts occurred across southern and western Buenos Aires province. These events could affect yield components, given that the crop is currently in sensitive phenological stages. However, the high ambient humidity may have mitigated the potential impact of the low temperatures, so it is necessary to wait for crop development to more accurately assess the actual effect. Under this scenario, the production forecast remains at 5.3 million tons.