International fertilizer prices appear to have plateaued after a strong upward trend that outpaced the performance of major grain and oilseed markets.

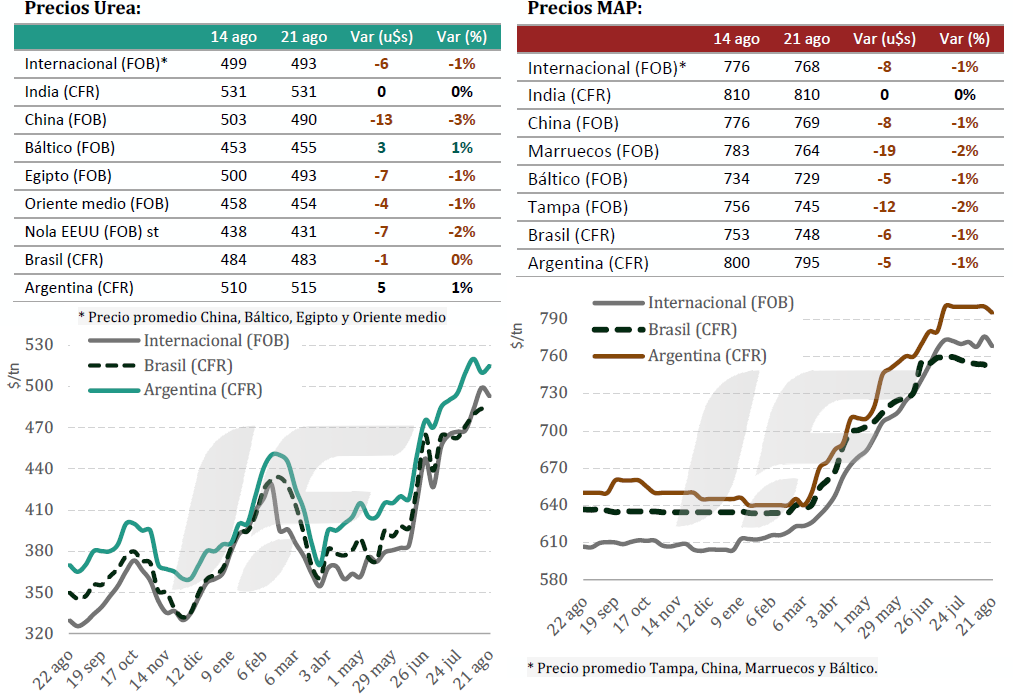

In the nitrogen market, India surprised traders by announcing a new tender for 2.0 million tons, closing on September 2, just days after its IPL Corporation awarded over 2.0 million tons at prices of $530–$532/ton CFR. This demand boost from the world’s largest fertilizer importer was offset when China released a third urea export quota of 650,000 to 750,000 tons, for delivery by October 15.

“In Egypt, prices fell slightly to $490-$495/ton FOB amid weak European demand. Russia showed limited sales at $460-$465/ton FOB while fulfilling existing orders for India,” notes the weekly report from consulting firm IF Ingeniería en Fertilizantes (IF Fertilizers).

“Brazil began making spot purchases of urea from Nigeria and North African countries at $480-$490/ton CFR, although more activity is expected in September due to seasonality. In Argentina, prices stood at $517-$520/ton CFR, higher than in Brazil, reflecting a willingness to pay a premium to ensure availability,” the report added.

The global phosphate market was also influenced by China’s release of new export quotas, which helped ease fertilizer prices in key origins like Morocco and the US.

“Brazil showed the greatest weakness: monoammonium phosphate (MAP) prices fell to $740-$750/ton CFR, and traded as low as $700/ton within the country, but this failed to stimulate new purchases. In Argentina, MAP stood at $790-$805/ton CFR, with minimal activity as traders remained on the sidelines, waiting for clearer international signals,” notes IF Fertilizers.

Argentine Market Outlook

“As local demand picks up and international prices remain firm, wholesale prices in Argentina are expected to adjust to international parity, gradually eroding the benefit of earlier purchases made at lower prices. This explains the price dispersion among importers and creates business opportunities depending on individual purchasing strategies,” warns IF Fertilizers.

The firm adds, “During the last week, there was greater dynamism in fertilizer sales and logistics. Importers began to tighten their commercial policies and raise list prices, in line with the international market’s upward correction.”

Import volumes of MAP and DAP (diammonium phosphate) were lower, while purchases of chemical blends (NPS, NPS+Zn)—which are more competitive in terms of cost per unit of phosphorus—increased.

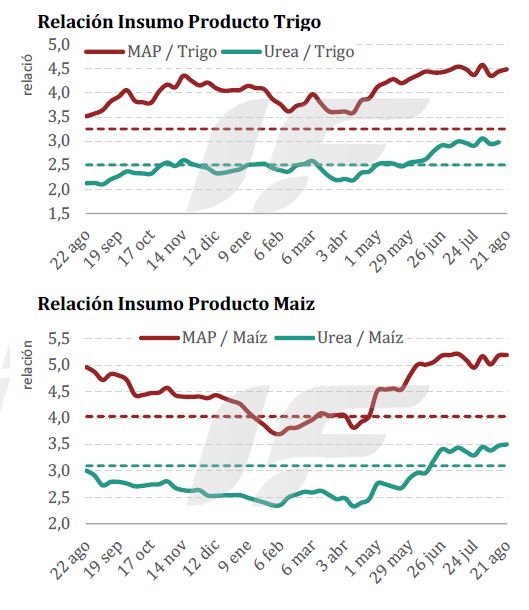

“Based on available information, there are no signs of a sharp price decline. On the contrary, all indicators suggest that the main crop season will be marked by high fertilizer prices and a very challenging input-to-output price ratio for Argentine producers,” the report emphasized.

In the southeast and south of Buenos Aires province (Argentina’s main grain-producing region), the economics do not justify further investment in wheat refertilization, while the outlook for malting barley appears much more promising.

Source: Valor Soja

Malaysia turns to ammonium chloride as amsul costs rise

According to Argus Media’s findings, Malaysian importers could turn to procuring more ammonium chloride (AC) for the rest of 2025 as a cheaper alternative to standard caprolactam-grade ammonium sulfate (amsul) fertilizers, as suggested by market participants.

Ammonium chloride is a by-product of the Solvay process where ammonia, CO2, and sodium chloride are combined to produce soda ash. Since AC has a relatively high nitrogen content of around 25%, it is often used as a substitute for other nitrogen fertilizers such as amsul, which has a lower nitrogen content of 21%.

AC fertilizers are sold at lower prices compared to amsul, mainly because its chlorine content is highly acidic and could potentially damage the soil upon repeated application. As Malaysian importers are more price-sensitive, they have consistently opted to apply AC to their crops as a cheaper nitrogen source and as an alternative to amsul. Standard AC offers to southeast Asia were high (US$90/t cfr in the week to 15 August), while Argus Media assessed standard caprolactam-grade amsul at US$185 – 190/t cfr southeast Asia in the same week.

AC imports to Malaysia in January-June were stable from the previous year at 354 000 t, according to the latest Global Trade Tracker data. China is the main AC supplier to Malaysia, accounting for 353 300 t.

But amsul imports to Malaysia fell by 25% on the year to 331 000 t in January-June. Deliveries from China slipped by 38% on the year to 238 000 t, while imports from Japan and Taiwan rose slightly to 33 700 t and 30 100 t respectively.

Standard caprolactam-grade amsul prices in January-June in 2025 have been higher at US$169/t cfr on an average midpoint basis, compared to US$154/t cfr in the same period in 2024, according to Argus Media’s data. The higher prices could have discouraged importers from readily purchasing large volumes of amsul, leading them to adopt a hand-to-mouth purchasing strategy.

At current prices, AC costs approximately US$386/t on a $/t nitrogen basis, while amsul costs around US$893/t. Amsul is twice as expensive compared to AC on a pure nutrient basis, which has encouraged Malaysian importers to make the switch to AC. AC is mainly used on oil palm plantations, because the crop is hardier and more resistant to damage from repeated applications of AC.

Malaysian importers will likely continue to procure more AC this year because it is comparatively more affordable. But an ongoing 60-day customs inspection approval process for Chinese AC exports could mean importers must secure cargoes earlier to ensure timely arrival for application.

Source: World Fertilizer

ARGENTINA MAIN CROPS OVERVIEW:

SUNFLOWER: At the beginning of this week, a broad storm front advanced, covering the entire eastern agricultural area, stretching from the NEA region to southeastern Buenos Aires, significantly improving the sunflower seeding scenario. While in the north of the country, planting has already exceeded 70% of the projected area, in the north-central part of Santa Fe, with 23% planting progress, the projected area to be planted has been consolidated. Although these events temporarily delayed the continuation of work, which marked a week-on-week progress of only 3 percentage points, nationwide, 15.8% of the projected 2.6 Mha has already been planted, registering a year-on-year advance of 15.3 percentage points and 6.6 percentage points compared to the average for the last five years.

WHEAT: Wheat, for its part, shows a significant improvement in available moisture at a crucial time for refertilization efforts (particularly in key regions contributing to production volume). Although excess moisture is observed in the central and eastern parts of the country, with favorable weather conditions, the situation is expected to normalize in the short term, allowing not only progress with the aforementioned efforts but also efficient nutrient assimilation. Regarding the ongoing excess water in the southern part of the agricultural area, collaborators assure that the most affected areas are those that have remained under water since the beginning of the campaign, and no additional crop losses are expected.

BARLEY: Regarding barley, planting has concluded nationwide after the last plots were incorporated in the southern agricultural area. During the planting window, areas in the south, center, and west of Buenos Aires experienced delays due to excess water, which hampered the entry of machinery. In a context of good water availability, 98% of the plots in the southern barley-producing areas are in Normal/Excellent crop condition, with 60% in full tillering. At the same time, following the recent rains, excess water has been recorded in central Buenos Aires, where 50% of the crop is in full tillering and will depend on the absence of precipitation to advance fertilization efforts.

CORN: The grain corn harvest advanced just 1.3 percentage points last week, reaching 95.9% of the estimated area. This progress represents a delay of -2.8 percentage points compared to the same period last year, as well as 1.1 percentage points compared to the average of the last five campaigns. There are still some late and second-crop plots to be harvested in the southern part of the agricultural area, an area that will require several days for general harvesting to resume. Therefore, the completion of the 24/25 corn harvest could extend into September. In this context, a production projection of 49 MTn is maintained.

Source: Buenos Aires Grain Stock