The Argentine fertilizer market continues to show lower-than-expected demand for this time of year due to both climatic and economic factors.

Persistent rains in central and western Buenos Aires province have caused excessive water, flooding, and significant operational inconsistencies, which continue to affect planting and slow the purchase and application of inputs.

The flow of liquidity from wheat is uncertain despite the extraordinary yields achieved in many regions due to both low prices and issues with the grain’s baking quality. It’s also worth noting that wheat, like other grains, is subject to a 9.5% export tax.

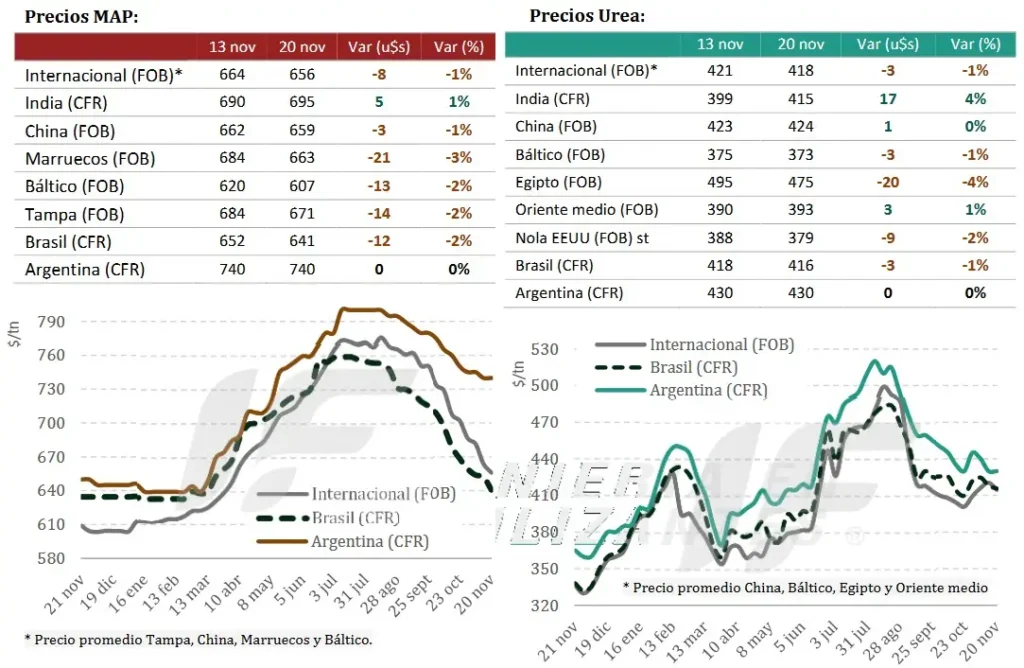

In this context, the phosphate fertilizer market remains virtually stagnant. “The combination of relatively high prices—which remain elevated despite international declines—and the inability to apply fertilizers on time due to adverse weather conditions is deepening producer caution,” states the latest report from the consulting firm IF Ingeniería de Mercado.

“Soybean demand has been significantly lower than expected, and the planting delays are eliminating immediate pressure. However, a temporary rebound could occur toward the end of the year, both due to delayed plantings and the start of the second corn crop, where application rates are lower but the planted area could be larger than initially projected,” the report adds.

In nitrogen fertilizers, the market continues to be the most dynamic. Abundant moisture supports expectations of a strong agronomic response and keeps adjusted purchases of urea and NPS blends active, especially for early-planted corn and the first plantings of late-planted corn.

Around December and January, weather permitting, the area planted with second-crop corn could increase, leading to a surge in nitrogen consumption, although this crop typically receives lower doses than early-planted corn.

“The end of the period leaves the phosphate market practically paralyzed and nitrogen as the only active sector, both highly influenced by the weather window and the producer’s need to resume operations as soon as conditions allow,” the report summarizes.

This week, the global nitrogen market experienced a phase marked by expectations surrounding a new auction in India, which resulted in the lowest prices since October and established a new international price floor.

“Demand outside of India remained subdued. Europe halted purchases due to logistical congestion and the imminent entry into force of the Carbon Border Adjustment Mechanism (CBAM) on January 1, 2026,” the report notes.

“Brazil maintained limited liquidity, and the US absorbed the elimination of import tariffs. Supply from the Middle East and North Africa continued to seek outlets for December shipments to India and Europe. The overall context left producers focused on India as their almost exclusive destination in the short term,” the report notes.

Regarding the global phosphate market, it experienced another downward trend this week. The elimination of import tariffs in the US accelerated the decline in barge shipments of monoammonium and diammonium phosphate (DAP and MAP) and discouraged new offerings.

“Meanwhile, Brazil maintained typical off-season low demand, with weak sentiment except for single superphosphate (SSP), supported by higher sulfur costs. China continued with limited export activity and declining prices due to a lack of buyers. In India, the market remained stable after a one-off purchase of Russian DAP. The downward pressure spread from the main origins—Russia, Morocco, Saudi Arabia, and China—to most global destinations,” the report summarizes.

Source: Valor Soja

End of tariffs repositions US in fertilizer trade.

The decision eases terms of trade, reignites demand, and puts downward pressure on fertilizer prices.

The decision by US President Donald Trump to eliminate tariffs on imported fertilizers — announced on November 14 — significantly alters the US market environment and generates new expectations for price formation in the short and medium term.

According to the Weekly Fertilizer Report from StoneX, a global financial services company, the removal of tariffs should reduce the cost of imported fertilizers and restore the attractiveness of the US market, one of the most important in the global nutrient trade.

“The tariffs imposed in the first half of 2025 created a significant distortion. Farmers have faced one of the worst terms of trade in recent years, pressured simultaneously by the decline in agricultural commodities and the increased cost of inputs. The suspension of tariffs tends to alleviate some of this imbalance,” assesses Tomás Pernías, Market Intelligence analyst at StoneX.

During the period when the tariffs were in effect, international suppliers redirected shipments to markets where they would not be taxed, reducing domestic supply in the US and contributing to maintaining prices at high levels. The uncertain environment also affected investors and intensified the caution of American farmers, who reduced new purchases due to the weak economic stimulus.

With the removal of tariffs, the market is already reacting. “The significant drop in diammonium phosphate (DAP) futures prices in recent days is a clear sign that the market has quickly incorporated the change and started pricing in bearish expectations,” explains Pernías.

Nevertheless, the expert cautions that the downward trend may have its limits. “The approaching spring stockpiling season could sustain demand and prevent a linear price drop. The market is currently experiencing a power struggle: on one hand, the bearish factor of tariff removal; on the other, the replenishment of purchases and the need for supplies,” he concludes.

Source: Cultivar Magazine

Misr Phosphate de Egipto informa sobre su planta de fertilizantes

Major Egyptian phosphate rock producer Misr Phosphate has ventured into the production of fertilizers, boosting its required phosphate rock output.

Construction of Misr Phosphate’s DAP/MAP/NPK plant will begin at Ain Sokhna in northeast Egypt by the 2Q26 once negotiations with lenders conclude at the end of 2025.

The plant will have a capacity of 600 000 tpy of DAP. Its annual capacity for phosphoric acid and sulfuric acid will be 320 000 t solution and 1.023 million t, respectively.

Misr Phosphate said that it will provide 1.25 million tpy of phosphate rock from its Red Sea mines to the plant.

The plant is under a joint venture of which Misr Phosphate will be a 15% shareholder and will receive 20% of production, which it plans to sell both to traders and directly to destination markets.

In July 2024, Egypt’s petroleum and mineral resources ministry reported meeting with global manufacturer Indorama to discuss establishing a phosphate fertilizer plant in Ain Sokhna in cooperation with Misr Phosphate.

Misr Phosphate is also working on projects with a Chinese producer, likely to be Chuanjinnuo, and with another Egyptian company. Pre-feasibility studies for both projects are ongoing.

Phosphate rock output to increase

To meet the requirements for its downstream projects in Egypt, and to maintain its presence in the global phosphate rock market, Misr Phosphate is increasing its phosphate rock production.

It said that its total run-of-mine across all its facilities may reach a capacity of 7 million tpy by the end of 2025.

Drilling programmes to increase proven reserves are ongoing and Misr Phosphate aims to secure more mining licences in 2026.

It is undergoing explorations near El-Dakhla in southwest Egypt to find new reserves.

The producer started marketing phosphate rock with reduced dust content from its mine at Abu Tartour at the end of 2024, mostly selling the product to Europe. It is aiming to increase its production of de-dusted rock to 1 million tpy by the end of 2026. The “de-dusting” facility had been running at an output of around 1000 tpd in February.

The proportion of fine particles in phosphate rock as it naturally occurs in Egypt had made it too dusty to be unloaded at many European ports.

Misr Phosphate said that in January-October this year it supplied around 600 000 t of phosphate rock to Europe, most of which is de-dusted product. This is already up compared with the 433 000 t of Egyptian phosphate rock that the EU imported in 2024, according to GTT data, which was less than half the volume from top-supplier Morocco in the same period.

Further east, demand for phosphate rock imports to Vietnam is emerging because of reduced domestic supply. Misr Phosphate said that so far this year it has shipped 150 000 t of phosphate rock to Vietnam, averaging 27% P2O5. The country imported 47 000 t of phosphate rock in 2024, and only 2000 t in 2023, all from Egypt.

Some market participants expect Vietnamese phosphate rock demand to be as high as 1 million t in 2026.

Vietnam reportedly takes phosphate rock from Egypt’s Red Sea mines, rather than Abu Tartour.

The quality of Egyptian phosphate rock delivered to buyers had been variable in the past. Misr Phosphate said that it has implemented improved quality control procedures throughout the mining and processing of the rock.

Source: World Fertilizer

ARGENTINE MAIN CROP’S OVERVIEW:

SOYBEANS: After a week-on-week increase of 12 percentage points, soybean planting has reached 24.6% of the projected 17.6 million hectares, registering a year-on-year delay of 11 percentage points. Meanwhile, 35.6% of the intended first-crop soybean planting area has been sown.

CORN: Corn planting has reached 37.3% of the projected area, with fields mostly in Normal to Excellent condition thanks to good moisture, although excess moisture persists in 12% of the area, hindering field operations. With 36% of the national total planted, producers are awaiting the optimal late-planting window towards the end of November to continue planting. The planted area is reported to be in Good to Excellent condition in 79% of cases.

SUNFLOWER: Planting is entering its final stage, with a week-on-week increase of 10.5 percentage points. Sowing has reached 95.1% of the projected 2.7 million hectares. 98% of the soil is in Normal to Excellent condition, and 85.1% has Adequate/Optimal moisture.

SORGHUM: Grain sorghum planting is progressing in the central agricultural area, reaching 34% of the national total under good water conditions.

WHEAT: Following the rains, harvest progress increased by 3.8 percentage points week-on-week, covering 20.3% of the suitable area. The average yield is 29.9 quintals per hectare, maintaining the production projection at 24 million tons.

Source: Buenos Aires Grain Exchange