Fertilizer prices on the international market continued to adjust downward this week, beginning to align with the purchasing power of major grains.

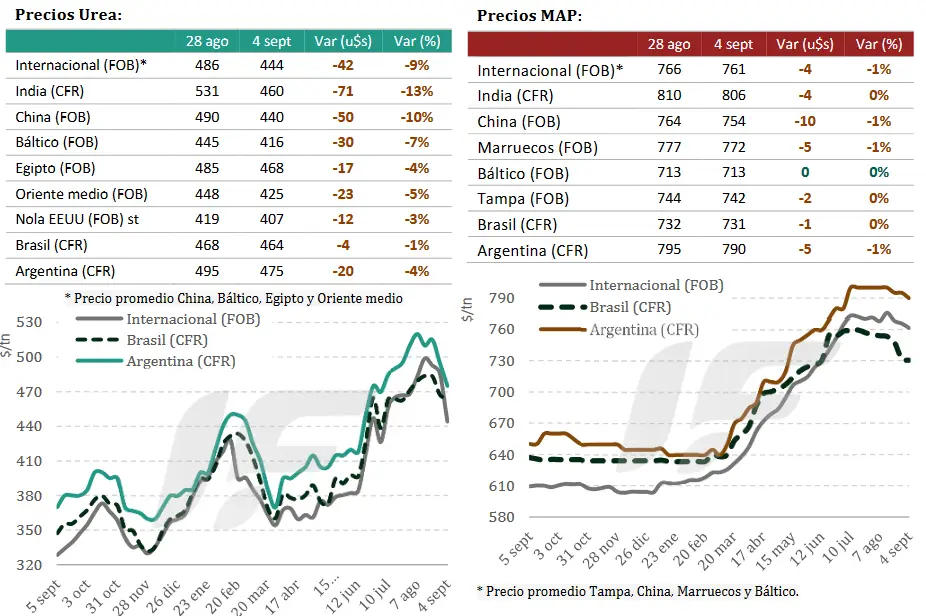

Regarding nitrogen, the urea tender launched by the Indian corporation NFL received bids totaling 5.6 million tons, a much higher volume than expected, reflecting ample product availability from Russia, the Middle East, North Africa, China, and Iran.

China was the main player in the Indian tender, with 600,000-700,000 tons committed before new export restrictions came into effect on October 15. “Abundant supply and falling prices led importers in Brazil, Europe, and the US to adopt a wait-and-see attitude,” notes the weekly report from the consulting firm IF Ingeniería en Fertilizantes.

In Brazil, trade activity was limited, and toward the end of the week, import prices consolidated in the range of US$440 to US$450/ton CFR. “Brazil continues to be the key market for the second half of the year, so the price level there is expected to be decisive for the direction of international trade,” the report notes.

“In this context, CFR urea prices in Argentina fell toward the end of the week to US$475/ton CFR, in line with international trends,” it adds.

The flooding caused a cooling of demand from Argentine producers, but if environmental conditions improve, fertilizer purchases should resume. Fortunately, heavy rains are not expected in the affected regions until at least September 15.

Regarding phosphates, the global outlook continues to show weak demand and tight supply, with prices slowly declining without yet achieving a significant drop that would improve the input-output ratio.

“The central factor was the expansion of export quotas in China, which released more volumes into the market, accentuating downward pressure. However, large tenders launched by Bangladesh (165,000 tons) and Ethiopia (549,000 tons) provided some short-term support,” the report explains.

In Brazil, the market showed weakness marked by financial problems of agricultural producers and a high level of pre-purchases of nitrogen and phosphates from China.

In the US, meanwhile, prices remained stable, although low inventories and the imminent closure of the Mississippi River anticipate upward pressures towards the final quarter. The Baltic Sea and Russia continued to adjust prices downward, affected by European tariffs and freight costs.

In India, the depreciation of the rupee against the dollar made imports more expensive and reduced purchasing capacity, so demand was limited, with a one-time purchase of 30,000 tons from Russia.

“In Argentina, the phosphate market showed signs of weakness, with reference prices falling US$5/ton for MAP (monoammonium phosphate). Trading activity remained limited. Although a gradual recovery in demand is expected as the season progresses, the market remains cautious regarding weather conditions and the availability of financing for producers,” he notes.

“In this regard, it is key to evaluate more competitive alternatives to traditional MAP 11-52 and DAP (diammonium phosphate), such as the chemical blends NPS, NPS+Zn, and MAP 10-50, which currently offer better relative market conditions,” he summarizes.

Source: Valor Soja

Las importaciones brasileñas de fertilizantesBrazilian fertilizer imports hit record high in August alcanzan un récord en agosto

Imported volume in the last month exceeds 5 million tons and may continue to rise in the coming months

Brazilian fertilizer imports this August reached a record high, exceeding 5 million tons, according to a weekly report from StoneX, a global financial services company. Last month, purchases of this type of input increased 10% compared to the same period last year, driven by increased purchases of raw materials essential for domestic production, such as ammonia, urea, sulfur, KCl, DAP, MAP, NAM, NP, SAM, SSP, and TSP.

According to the survey, due to seasonal factors, Brazilian fertilizer imports tend to increase between the end of the first half of the year and the first months of the second half of the year. “This period accounts for most of the agricultural input purchases made by importers, resulting in higher volumes between June and October,” says Market Intelligence analyst Tomás Pernías.

According to the analyst, historical data from the last three years indicate that phosphate imports peak between June and August, while potassium chloride purchases peak mainly between May and August. “Thus, July and August are among the months with the highest fertilizer inflows into the country, reflecting preparations for the next harvest,” adds Pernías.

Demand for less concentrated fertilizers grows in the country

According to the StoneX report, the increase in imports was also driven by the greater demand for less concentrated fertilizers, a trend that marked the Brazilian market in 2025. “With the reduced supply in the MAP market and the adjusted balance in urea, Brazil sought alternatives with a better cost-benefit ratio,” explains Pernías.

Among the products that have been gaining ground in the Brazilian market is NP, whose imports totaled more than 2,6 million tons between January and August 2025 — a 68% increase compared to the same period in 2024. Ammonium sulfate also stood out, with 3,7 million tons imported, a volume 59% higher than last year.

According to the analyst, the choice of less concentrated products tends to increase the total volume imported and traded, as larger quantities are required to meet the same nutrient demand that would be met by more concentrated fertilizers. However, it raises questions about the ability of these products to replace other, more concentrated goods, traditionally preferred by importers in recent years.

Source: Cultiva Magazine

Adufértil to acquire Fass Agro in push to expand liquid fertilizer portfolio

Adufértil Fertilizantes, a unit of Singapore-based Indorama, has agreed to acquire Fass Agro, a Brazilian producer of liquid fertilizers, in a move that underscores intensifying competition in the global crop nutrition market.

The transaction, which remains subject to regulatory approval, would broaden Adufértil’s offerings beyond solid blends and establish a stronger position in the liquid segment—a category gaining traction among growers seeking more efficient and precise application methods.

Gustavo Zaitune, Adufértil’s chief executive, said the deal will reinforce the company’s role in key regional markets while widening its portfolio of sustainability-focused solutions. “It also expands our offering of productivity-enhancing solutions for our clients,” he said.

Indorama Vice Chairman Amit Lohia said the acquisition will create “a leading platform for liquid fertilizers for our farming community,” complementing existing solid formulations in the group’s portfolio.

The move highlights how global producers are reshaping portfolios to capture demand for inputs that promise higher yields with lower environmental impact. Competitors such as Nutrien, Yara International and Mosaic are also expanding into specialty and liquid products, betting that farmers facing volatile commodity prices and regulatory pressure on emissions will turn to more targeted fertilizer use.

Source: Fertilizer Daily

ARGENTINE MAIN CROPS OVERVIEW:

SUNFLOWER: Sunflower planting is slowing after the rains of recent days. Nationwide, week-on-week progress was 3.4 percentage points, covering 22.7% of the projected 2.6 million hectares. Progress of 7.4 and 17.5 percentage points is still recorded compared to the average for the last five years and the previous cycle, respectively. In the NEA region, planting is nearing completion, and early vegetative development is occurring under optimal humidity conditions. In north-central Santa Fe, planting progressed at an accelerated pace prior to the arrival of the rains. Despite the current excess water levels, work is expected to resume in the coming days if conditions are favorable. However, the scenario is different in the south of the agricultural area, where the recurrent action of the rains prevents the recovery of lots and roads that, linked to the evolution of the climate, could see their implementation compromised.

WHEAT: In the case of wheat, the Santa Rosa phenomenon affected a large portion of the planted area in the western agricultural area, considerably improving the outlook for the cereal in those sectors. Although 27.3% of the area shows excess water, concentrated mainly in the eastern and southern areas where outbreaks of fungal diseases are beginning to be reported, 98% of the standing area remains in Normal to Excellent crop condition. This is particularly favorable for the 26.9% of the cereal that is in the seed stage and beyond. Although there is growing concern about the recurrence of rains, the impact on winter crops is estimated to be positive given the increasing demand for water they will experience as they enter the reproductive stages.

BARLEY: Regarding barley, as mentioned above, the recent rainfall has improved moisture profiles; however, it has caused flooding in specific areas of eastern and southeastern Buenos Aires. Currently, 82% of the fields have Adequate/Optimal water conditions, and 93% of the planted area shows an overall crop status of Normal/Good. Regarding phenology, 76% is in full tillering, while 11% has begun the tillering stage. Collaborators in southwestern Buenos Aires report that progress has been made with nitrogen fertilization plans. Furthermore, 91% of the barley fields in the south, which account for 70% of the total area, have Normal/Good crop conditions.

CORN: Finally, the 2024/25 corn harvest progressed slowly over the past week due to the aforementioned rainfall, reaching 98.5% of the estimated total, reporting a national average yield of around 72 t/ha, allowing us to maintain our projection of 49 MTn. On the other hand, planting for the 2025/26 season, which is expected to see a 9.9% year-on-year area recovery, has progressed slowly due to excessive rainfall, and harvesting is expected to resume in much of central and southern Santa Fe, Entre Ríos, and eastern Córdoba in the coming days.

Source: Buenos Aires Grain Stock