Argentine fertilizer demand remains unresponsive despite the start of the early corn planting season, deepening the downward pressure observed in the global market.

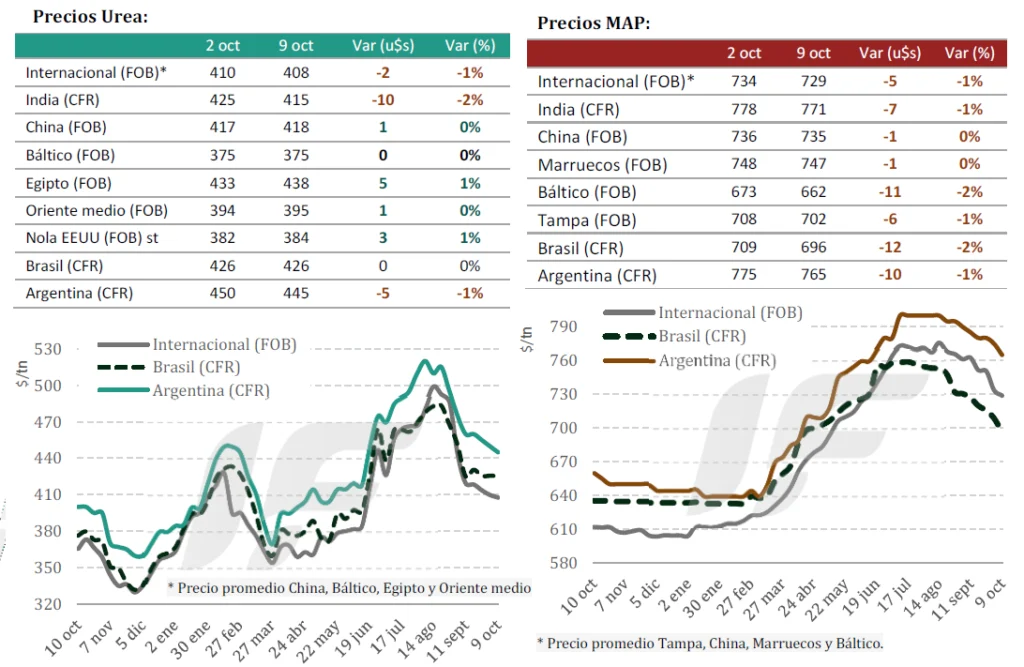

The international urea market has adopted a wait-and-see approach ahead of the Indian auction on October 15. Buyers are also closely monitoring export quotas granted by the Chinese government amidst a turbulent geopolitical environment.

In Brazil, the market is virtually paralyzed. “Buyers have suspended new urea purchases, limiting activity to very specific spot transactions. Importers continue to show a strong preference for ammonium sulfate over urea, primarily due to lower cost per unit of nitrogen,” notes the weekly report from the consulting firm IF Ingeniería en Fertilizantes.

Regarding phosphate fertilizers, international prices continued their decline, adjusting to current agricultural commodity purchasing power. India maintains ample stocks of diammonium phosphate (DAP), while China keeps its exportable supplies limited, showing no signs of expansion.

Argentina continues to see low trading activity. Urea import prices remain stable at around US$445/ton CFR, while monoammonium phosphate (MAP) averages US$765/ton CFR. Demand is weak, with several buyers withdrawing as they anticipate further price drops.

“Argentine demand was constrained by the completion of early corn applications and the shift into the planning phase for late corn and 2026 wheat planting,” the report explains.

While a very strong 2025/26 Argentine corn season is expected, this optimism is not translating into fertilizer demand. Soybean products present an even more subdued outlook, characterized by minimal demand and postponed purchasing decisions, despite the proximity of application dates.

“Corn purchases are progressing very slowly and in dribs and drabs, generating concern among importers who are struggling to move their existing stocks or meet expected sales targets,” the report notes.

This situation complicates logistics and fuels downward price pressures on both phosphate and nitrogen products. However, some specific supply constraints are observed for traditional products, particularly MAP 11-52 and DAP, as not all importers have immediate availability.

In summary, the Argentine market maintains a depressed price tone with generally good supply levels, barring specific exceptions. The report concludes: “Only urea could change its trend if China halts its exports or if the results of India’s new tender generate a shift in the international price balance.”

Source: Valor Soja

Global Fertilizer Markets: Ammonia Oversupply and Moderate Prices Forecast for 2026

Global ammonia production is outpacing demand, leading to anticipation of moderate prices in 2026. Geopolitical factors, new production facilities, and energy costs are currently driving the nitrogen fertilizer market.

The international ammonia market is navigating a transition period following two years of high volatility. According to the Argus Fertilizer Analytics report published in Fertilizer Focus, expanding production capacity in North America and the Middle East, coupled with the normalization of Russian supplies, points toward a scenario of moderate oversupply and price adjustments throughout 2026.

Supply Dynamics and Price Correction: During 2025, production disruptions in key regions—including the Middle East, Southeast Asia, Trinidad, and North Africa—caused brief, seasonal price increases. However, equilibrium began to restore in the third quarter with the reactivation of plants in Saudi Arabia, Iran, and Egypt, along with the start-up of the new 1.3 million tonne/year facility at the US-based Gulf Coast Ammonia.

Despite temporary logistical issues at Russia’s Ust-Luga terminal, the global supply quickly recovered. Russia has resumed seaborne exports and expanded its domestic rail capacity, facilitating access for inland plants to the international market. As a result, pressure on spot prices has begun to ease as availability increased toward the end of the year.

Meanwhile, India maintained a robust market presence, driven by preparations for the Rabi season (October-March). Indian ammonia imports stabilized thanks to the resumption of flows from Iran and the Middle East, although increased natural gas prices and logistical constraints kept prices relatively elevated during the third quarter. A gradual moderation is expected toward the end of the year as demand shifts to other phosphate and nitrogen fertilizer segments.

Western Market and Regulatory Headwinds: On the Western front, the situation differs. Europe and North America face higher energy costs and reduced agricultural activity during the winter, factors that limit immediate demand.

The European Union is also preparing for the entry into force of the Carbon Border Adjustment Mechanism (CBAM), which will make imports of emissions-intensive products, including ammonia, more expensive. Analysts estimate that the new tax could add between USD 25 and 30 per ton to the final cost, incentivizing greater local production using cleaner technologies.

Nevertheless, the overall trend continues to point toward a price correction. With more than 2.4 million additional tons per year expected in the U.S. before the end of the year, the market shows clear signs of abundance. The report predicts that reference prices in Tampa (USA) and the Gulf of Mexico will not repeat the peaks of 2025, instead remaining at moderate or slightly declining levels through 2026.

In the Middle East and Asia, the outlook is expected to be more stable. Improvements in logistics capacity—though partially limited by tensions in the Red Sea—will sustain flows to India, Korea, and Southeast Asia. FOB Middle East prices are expected to remain within a narrow range, with slight declines toward the second half of next year.

The Rise of Green Ammonia: The global oversupply does not necessarily imply a negative scenario. For agriculture, it represents an opportunity to improve profitability through more affordable inputs. However, competitive pressure will be greater for ammonia producers, with a possible slowdown in investment if margins remain tight.

The sector’s focus is now on the transition to green ammonia, driven by projects in Europe, the U.S., and Asia that seek to partially replace natural gas with renewable hydrogen. However, this segment’s market share is still nascent—less than 2% of the global total—and will not offset the expansion of conventional plants in the short term.

In conclusion, the global nitrogen fertilizer market is entering a period of structural adjustment where supply is growing faster than demand and prices are moderating after years of tension. While overcapacity may challenge traditional producers, it also paves the way for a more efficient, diversified industry aligned with sustainability and food security goals.

Source: AgroLatam GlobalAgroLatam Global

Brazil’s Petrobras set to supply 20% of country’s demand for nitrogen fertilizers in 2026

Brazilian state-run oil company Petrobras (PETR3.SA), opens new tab will be able to deliver about 20% of the country’s total demand for nitrogen fertilizers next year as it restarts operations at three local plants, CEO Magda Chambriard said on Thursday.

Petrobras’ Bahia and Sergipe plants, both in Brazil’s northeastern region, are expected to supply 5% and 7%, respectively, of the national urea market, according to the company’s strategic plan.

Meanwhile, its unit in Parana state, in southern Brazil, has already resumed operations, and aims to supply 8% of the country’s urea demand. All three plants were previously offline.

During an event in Bahia state, Chambriard also highlighted that the company is working to resume operations at a nitrogen fertilizer plant in Mato Grosso do Sul state. The unit would be expected to account for 15% of total demand.

“This plant is already being contracted, the construction will be completed, and once it’s ready, we will be capable of delivering 35% of all the nitrogen fertilizer Brazil needs,” the executive said.

The renewed investment in the fertilizer sector aligns with President Luiz Inacio Lula da Silva’s goals, as he has advocated for the firm to resume investing in the industry. Brazil is heavily dependent on fertilizer imports.

“With the public policies issued by the federal government and with our shareholders, we are aware of Petrobras’ strategic role,” Chambriard said.

Source: Reuters

ARGENTINE MAIN CROPS OVERVIEW:

CORN: Corn planting maintains a year-on-year advancement of 7.9 percentage points (p.p.), driven by progress in the center of the agricultural area. Early planting efforts have concluded in Entre Ríos and North-Central Santa Fe.

SUNFLOWER: 35% of the projected area of 2.7 Million Hectares (MHa) is now planted, following an inter-week progress of 2.7 p.p. This maintains significant advancements of 9.8 p.p. and 22 p.p. compared to the previous cycle and the last five-year average (U5C), respectively.

WHEAT: Despite an increase in phytosanitary issues, 96.4% of the wheat crop is currently rated under Normal to Excellent condition. 90.7% of the area is now past the stem elongation stage (tillering onward).