Adecoagro announced the submission of a binding offer to acquire YPF’s 50% stake in Profertil S.A., the largest producer of granular urea in South America.

The binding offer was presented on terms and conditions virtually identical to those previously agreed upon between Adecoagro and Nutrien, including a purchase price of approximately US$600 million.

YPF’s acceptance of Adecoagro’s offer is subject to approval by the board of directors of YPF, a company controlled by the Argentine state.

If President Javier Milei’s administration accepts the offer—a highly likely scenario—then Adecoagro, a company controlled by the cryptocurrency corporation Tether,

will become the controlling shareholder of Profertil with 90% of the total share capital. The remaining 10% will be held by the Argentine Cooperative Association (ACA).

Adecoagro, in a statement, said it “will finance the transaction through a combination of existing cash balances, a new long-term credit facility already committed, and proceeds from the sale of equity.”

With an annual capacity of approximately 1.3 million metric tons of urea and 790,000 metric tons of ammonia, the company supplies approximately 60% of Argentina’s urea consumption.

Its state-of-the-art industrial complex, located in Bahía Blanca—Argentina’s most important petrochemical center—has access to natural gas and electricity at competitive prices.

“This transaction marks an important milestone for Adecoagro, as it expands our scale, diversifies our portfolio, and strengthens the company’s long-term performance,” said Mariano Bosch, co-founder and CEO of Adecoagro.

“With the support of our main shareholder, we are leveraging Argentina’s competitive advantages to drive sustainable growth and create value for our stakeholders. The acquisition of Profertil positions Adecoagro as a key supplier to the regional agricultural sector, integrating a business with solid fundamentals and consistent cash flow generation,” he added.

With control of Adecoagro, the project designed by YPF—more than a decade ago—would be consolidated. This project involves building a new urea plant adjacent to the existing one, doubling national production and transforming Argentina into a nitrogen-self-sufficient nation.

Although the technical proposal has already been validated, the project has never been implemented due to a lack of suitable macroeconomic conditions that prevented access to financing at reasonable rates.

“At Tether, we are pleased to support Adecoagro in this strategy. Profertil is a best-in-class company, essential to the agricultural production chain in Argentina and South America, and we believe its integration will significantly enhance Adecoagro’s platform by increasing exposure to real and sustainable assets that generate long-term value,” said Juan Sartori, Director of Special Projects at Tether and Chairman of the Board of Adecoagro.

Source: Valor Soja

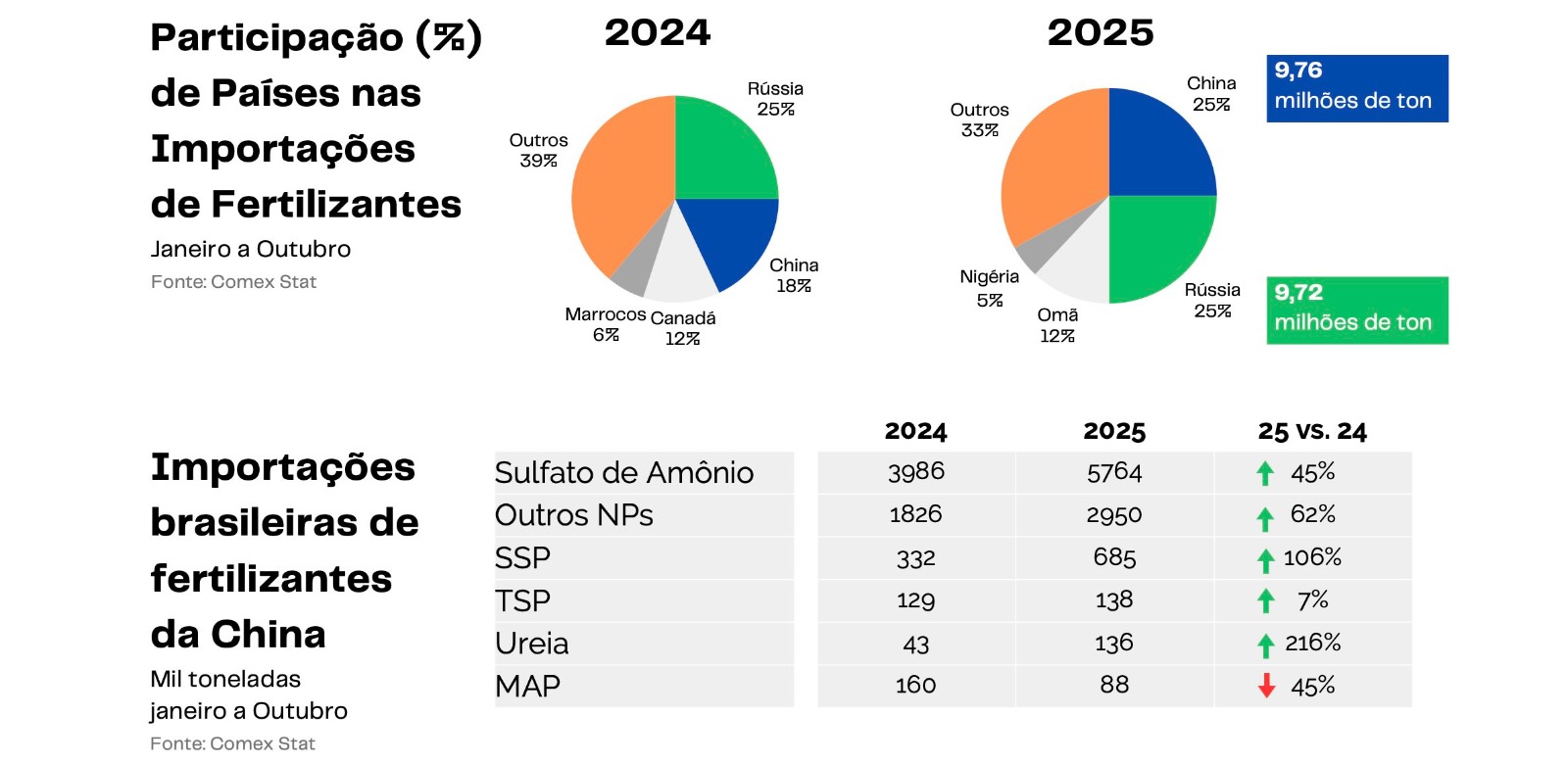

China takes the lead in supplying fertilizers to Brazil.

A report from CNA indicates cautious domestic demand, prices still under pressure, and a structural change in the profile of suppliers.

Brazil has increased its fertilizer imports and recorded a further increase in Chinese participation in sales to the country. From January to October, purchases totaled 38,3 million tons, a 4,6% increase compared to the same period in 2024. China surpassed Russia and became the leading supplier, driven by increased exports of Ammonium Sulfate (SAM) and NP formulations. This information is contained in a report by the CNA (National Confederation of Agriculture).

The domestic market is operating with weakened demand. India, the United States, and Brazil are reducing their impetus for new negotiations. This retraction sustains the trend of stable or falling prices. Urea costs R$ 3.445 per ton, MAP R$ 4.899, SSP R$ 2.091, and KCl R$ 2.880.

The pace of deliveries in the country is exceeding that observed in 2024. By August, 30,5 million tons had arrived, a 9% increase. The CNA (National Confederation of Agriculture) projects a record volume in 2025. Delays in purchases in Rio Grande do Sul may influence the final result. In 2026, even with profitability and credit challenges, producers are expected to maintain investment in crops.

Growth in supply

Chinese supply is growing at a rapid pace. Imports jumped from 9,72 million tons in 2024 to 9,76 million in 2025. This movement generated queues at the Port of Paranaguá. Ships waited up to 60 days to unload. The backlog put pressure on operational capacity and increased costs and demurrage.

In the domestic market, nitrogen fertilizers remain volatile. The purchase announced by India halted the decline in urea prices and brought upward pressure. Cautious demand is encouraging substitution with SAM (sugar-based phosphates). In phosphates, MAP (mineralized phosphate) is falling, but the terms of trade are still hindering new purchases. In potash, limited supply in Brazil is supporting firm prices.

Exchange rates show a loss of purchasing power in several crops. Soybeans face less favorable conditions for KCl acquisition. Cotton maintains a negative scenario, affected by still expensive phosphates. Corn improves its exchange rate with SAM and registers an advance in urea. Coffee remains an exception and shows consistent gains for the producer.

Cultivar Magazine, based on information from CNA

Saipem has been awarded two new contracts by Dangote Fertilizer.

Africa’s leading fertilizer producer, for technical know-how and licensing for the realisation of six urea units – four in Nigeria and two in Ethiopia – and the provision of basic engineering and design services for the related plants.

The licenses concern the use of patented and proprietary Snamprogetti™ urea technology, while the process engineering services include all the technical documentation required for the construction of the urea units within the fertilizer production plants. Each unit will feature a record capacity of 4235 tpd.

The new plants are part of an industrial plan that foresees the construction of six integrated ammonia/urea complexes – four in Nigeria and two in Ethiopia – for a total production capacity of over 25 000 tpd of urea.

In addition, Saipem and Dangote Fertilizer have signed a Letter of Intent (LoI) for the award to Saipem of front end engineering design (FEED) services relating the new complex in Ethiopia, developed in partnership with Ethiopian Investment Holdings for the construction of a plant with a capacity of 3 million tpy of urea in Gode, in the Somali region of the country.

With these new licensing and process engineering contracts, Saipem consolidates its leadership in the fertilizer sector, strengthening its presence on the continent and confirming its ability to deliver high-efficiency, low environmental impact technological solutions, and setting new standards for the sector. Today, the Snamprogetti urea technology has been so far adopted in more than 140 operating units worldwide, testifying to a global recognised know-how.

ARGENTINE MAIN CROPS OVERVIEW:

SOYBEANS: Nationwide soybean planting has reached 36% of the 17.6 million hectares projected for the current season, registering a year-on-year delay of 9 percentage points and a 1 percentage point delay compared to the average of the last five seasons. Excessive rainfall persists in central Buenos Aires province, hindering progress in planting the first-crop soybeans. Meanwhile, over 70% of the intended first-crop planting has already been completed in both the central and southern regions, with localized delays in areas such as Chacabuco due to excessive rainfall. Simultaneously, with 2.3% of the intended planting area already sown, planting of the first second-crop soybeans is beginning, primarily in southern Santa Fe province.

CORN: Corn planting for grain is gaining momentum with the start of the late planting window in the central and southern agricultural areas. To date, 39.3% of the national total has been planted, following a week-on-week increase of 2 percentage points. Of the area already sown, an estimated 82% is in good to excellent condition, reflecting an 8 percentage point improvement thanks to adequate soil moisture. However, further rainfall is expected to ensure proper germination in late plantings. Meanwhile, in central and western Buenos Aires province, approximately 30% of the planted area is affected by excessive moisture.

SUNFLOWER: Sunflower planting, meanwhile, showed week-on-week progress of 1.2 percentage points due to delays caused by excessive moisture in the southern agricultural area. To date, 96.3% of the projected 2.7 million hectares have been planted. Meanwhile, sunflowers planted in the provinces of Buenos Aires and La Pampa are progressing through vegetative stages, with the most advanced fields at the V6 stage. In the central and northern agricultural areas, 30.1% of the crop is at the bud stage or beyond. With 86.7% of the crop under adequate/optimal water conditions, 98% remains in normal to excellent condition.

WHEAT: Harvesting has already covered 33.9% of the suitable area, following a week-on-week increase of 13.6 percentage points. Harvesting is extending into the central agricultural region, progressing at a rate similar to the historical average, yielding results that exceed expectations in our previous production forecast, with a national average of 35.9 quintals per hectare. Meanwhile, the assessment of the impact of the late October frosts shows less damage than anticipated, both in the extent of the affected area and the severity of the damage, reflecting how the high moisture levels present in the soil profile helped to mitigate the effect of these events. In conclusion, the production projection is 25.5 million tons (MTn), 1.5 MTn above the previous projection, exceeding the previous maximum (2021/22 season: 22.4 MTn) by 13.8%.

BARLEY: The barley harvest covers 3% of the suitable area nationwide, and work is becoming widespread in the central and northern agricultural regions, while progress remains limited in the south. Nationally, of the area still pending harvest, 43% is at physiological maturity, and the remainder is in the final grain-filling stages. Over the west and southeast of Buenos Aires, although the frosts of late October and early November have had a heterogeneous impact, the yield potential is better than expected, compensating for the losses caused by the frosts and allowing a production projection of 5.3 MHa to be sustained.