The escalation between the US, Israel, and Iran is driving up energy and fertilizer prices. Agriculture faces greater volatility in grain prices and rising costs.

The escalating conflict between the United States, Israel, and Iran began impacting agricultural markets on March 9, with increases in energy, fertilizer, and logistics costs already generating greater volatility in corn, soybeans, and wheat. The most worrying figure for the sector is the surge in urea prices, which are approaching US$700 per ton, threatening to raise agricultural production costs worldwide.

The conflict, which initially impacted the energy market, is now beginning to affect agricultural commodities, disrupting prices and generating uncertainty during planting and harvesting planning. One of the factors that accelerated the market reaction was the blockade of the Strait of Hormuz, a key point for global energy trade.

This boosted the price of Brent crude oil by about 15%, bringing it close to US$90 per barrel. In an increasingly integrated agricultural market, these movements can quickly translate into international grain prices.

Fertilizers on alert: Urea prices rise sharply

The most significant impact of the conflict is being felt in nitrogen fertilizers, which are essential for agricultural production.

In recent days:

- Urea prices have risen by about US$80 per ton,

- representing an increase of approximately 13%,

- reaching prices of US$683 per ton in the Gulf of Mexico.

Much of the international fertilizer trade depends on natural gas and energy routes in the Middle East, so any disruption in the region directly impacts the cost of food production.

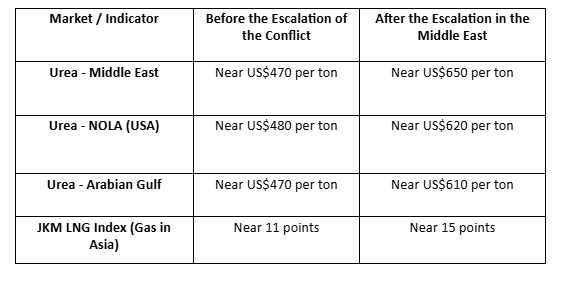

How Fertilizers and Energy Reacted After the Start of the Conflict

Market Highlights: Urea rose between US$130 and US$180 per ton in just a few days.

Liquefied natural gas (LNG) also surged, reflecting global energy pressures.

Energy and fertilizers move in tandem because urea production is heavily dependent on natural gas.

“In recent geopolitical clashes, the impact was limited and short-lived. The difference now is that tensions continue to escalate and are ultimately affecting grain prices as well.” Corn, the most exposed crop

Among the major grains, corn appears to be the most vulnerable to the new international landscape.

This is due to three reasons:

1. It uses large quantities of nitrogen fertilizers,

2. It is linked to the energy market through ethanol,

3. And it is a strategic staple food for many countries.

Therefore, when fertilizer and energy prices rise, corn tends to be the first to react in international markets. Furthermore, the increase in urea prices comes at a critical time for the United States, where producers are about to begin planting. Analysts warn that current costs could lead to a reduction of between 1 and 1.5 million hectares planted, which in the medium term could boost prices.

In the case of wheat, the market shows mixed signals. On the one hand, Argentina is aggressively placing its production on the international market, making it difficult for exporters like Europe to sell their surpluses.

- However, prices still face limitations because:

- Global stocks remain high,

- and crops in the Northern Hemisphere are still in their winter stage.

In soybeans, on the other hand, the outlook continues to be driven by Chinese demand. US exports remain weak, and China maintains its preference for buying from Brazil, which is once again experiencing high production this year. Today, global agriculture faces an unusual scenario: geopolitical factors outweigh agricultural ones.

The war in the Middle East is generating a chain reaction:

- Fuel prices are rising,

- Fertilizer prices are increasing,

- Transportation costs are rising,

- and grain price volatility is increasing.

If the conflict continues to escalate, agricultural production costs could continue to rise, with a direct impact on international food prices.

Source: AgroLatann

Turkey removes urea import duty

According to an Argus Media report, Turkey has eliminated its 6.5% import duty on urea under a Presidential Decree published in the Official Gazette on 7 March 2026. Most urea origins, apart from Egypt, Qatar, and Malaysia, faced a 6.5% import duty prior to the move.

The amendment covers urea spanning HS codes 31021012, 31021015, 31021019 and 31021090, and took immediate effect upon publication.

Import dependence

Turkey remains heavily reliant on imported nitrogen products, with urea imports averaging 2.8 million tpy in 2023 – 25.

Imports reached about 2.7 million t in 2025, with Iran – frequently listed as Oman – supplying roughly 44% of total volumes. Egypt accounted for around 24%, while Russia supplied about 13%, mainly in 1H26. Deliveries from Turkmenistan and Uzbekistan together totalled around 300 000t.

Turkey also imported 60 000 t of Qatari urea in 2025. Qatari urea last featured in the Turkish line-up in 2022 and 2023, with just 44 000t and 22 000 t imported, respectively. Turkey opted to remove import duties on Qatari urea from 1 August.

Market implications

The removal of import duty is expected to increase urea inflows ahead of Turkey’s spring demand peak, particularly for wheat top dressing, as well as barley, rapeseed and early corn applications. The change is set to reshape trade flows, eroding the previous duty-free advantage enjoyed by Egypt and more recently Qatar, and bringing other exporting origins into more direct competition.

Competitive pressure on domestic producers

The elimination of import duties will intensify competitive pressure on Turkish nitrogen producers, whose costs are structurally higher, given their reliance on imported gas and other feedstocks. Local producers may respond by focusing on contract sales or maybe blending products to protect market share.

The policy shift will likely reinforce Turkey’s role as a growing import, blending and redistribution hub, a local market participant told Argus.

Source: World Fertilizer

Bulo Bulo Urea Plant Resumes Operations and Reinforces Fertilizer Supply for Agriculture

After 28 days of technical maintenance, the plant expects to operate at 90% capacity, guaranteeing the supply of a key input for agricultural productivity in Bolivia.

The Ammonia and Urea Plant (PAU) in Bulo Bulo, located in the department of Cochabamba, resumed operations after 28 days of technical maintenance, a necessary process to ensure the efficient functioning of its production systems. According to Yacimientos Petrolíferos Fiscales Bolivianos (YPFB), the plant restarted activities on Sunday and expects to reach approximately 90% of its operating capacity in the coming days.

According to the plant’s Operations and Maintenance Director, Luis Antonio Sempertegui, the scheduled shutdown was primarily for maintenance work on the secondary reformer’s heat recovery boiler (101-C), a fundamental component in the fertilizer production process.

The Bulo Bulo plant is considered one of the most important strategic infrastructures for the Bolivian agricultural sector, as it produces urea, a nitrogen fertilizer widely used in crops such as soybeans, corn, rice, wheat, sugarcane, and other grains that form part of the country’s productive base.

During 2024, the plant reached a record production of 525,574 tons of urea, a volume that allowed it to cover almost 100% of the domestic market, significantly reducing dependence on imported fertilizers. This has been key to maintaining relatively competitive costs for agricultural producers, especially in productive regions such as Santa Cruz, Beni, and the country’s valleys.

“The reactivation of the urea plant strengthens the supply of fertilizers for the agricultural sector, reducing dependence on imports and supporting the productivity of Bolivian agriculture.”

The availability of domestically produced urea has a direct impact on agricultural productivity, as this fertilizer provides nitrogen to the soil, one of the essential nutrients for crop development. Proper use of this input allows for improved yield per hectare, increased production, and strengthened food security.

However, when the plant halts operations, even for maintenance, the agricultural sector is concerned about the potential impact on fertilizer supply. In previous years, prolonged shutdowns forced farmers to import urea at higher prices, increasing their production costs.

The rising cost of fertilizers is one of the factors that most affects the cost structure in agriculture, especially in extensive crops where fertilization is essential for achieving competitive yields.

For this reason, maintaining the plant in continuous and efficient operation is crucial for the country. It not only guarantees domestic supply but also allows for the generation of surpluses for export, representing additional income for the national economy.

With the resumption of operations at the Bulo Bulo Ammonia and Urea Plant, the agricultural sector once again has a strategic source of fertilizers that contributes to sustaining the productivity of the Bolivian countryside and strengthening the competitiveness of national agriculture.

Source: PubliAgro – Bolivia

Aprosoja in Brazil advises producers against unnecessary fertilizer purchases to avoid fueling the price surge.

The organization representing soybean producers in Brazil (Aprosoja) advised caution when planning fertilizer purchases.

“Recent volatility in international energy, transportation, and agricultural input markets has reignited concerns about the potential impact on the prices of imported fertilizers, primarily from Middle Eastern countries,” Aprosoja stated in a press release.

“However, the current situation does not justify an immediate rush to anticipate purchases, especially by producers who do not currently have the operational or financial need to lock in prices,” it added.

Aprosoja recommended “caution, as prices do not yet reflect a structural shock like those seen in previous conflicts, when there was a direct disruption of supply and an explosive increase in costs.”

While uncertainty about the duration and intensity of the conflict in the Middle East remains high—meaning that fertilizer prices could rise or fall—Aprosoja warned that excessive purchases now could lead to opportunistic actions and cause further price increases.

According to Aprosoja, anticipating purchases makes no sense when the decision is based solely on fear or market pressure, nor in situations where the producer is unclear about the area to be planted or the nutritional plan.

“The organization believes that purchasing is not recommended when anticipation compromises cash flow or increases exposure to credit, nor when there is no immediate risk of logistical disruption for the type of fertilizer used,” it emphasized.

“Anticipation can be considered in cases where there is a real need to guarantee availability; when the purchase improves margin predictability; when the producer has favorable financial conditions; and when the risk of price increases clearly outweighs the risk of price correction,” Aprosoja stated.

In other words: the decision must be rational, based on feasibility, planning, and margin analysis. And not on market panic.

Source: Valor Soja.

ARGENTINE MAIN CROPS OVERVIEW:

SOYBEANS: For soybean cultivation, while significant rainfall accumulations have been recorded in the north and west of the agricultural region, central and southern Buenos Aires continue to experience a marked water deficit. Consequently, the area under Adequate/Optimal water conditions registered a week-on-week increase of almost 5 percentage points. Furthermore, recent rainfall improved crop conditions, with 76.2% now in the Normal/Excellent category (a week-on-week increase of 2 percentage points). Regarding first-crop soybeans, 81% of the planted area is in Normal/Excellent condition, and with harvest approaching, expected yields average 37 quintals/hectare in the Northern Core region and 38 quintals/hectare in the Southern Core region, according to our collaborators. Meanwhile, for second-crop soybeans, 65.5% of the area is in Normal/Excellent condition, with more than 50% of the area currently in the critical period. Under this context, a production projection of 48.5 million tons (MTn) is maintained.

CORN: Regarding corn, the harvest is progressing 2.2 percentage points and has reached 9.4% of the suitable area nationwide, with work concentrated mainly in the Northern Core and North-Central regions of Santa Fe, where yields average 96.8 and 72.1 quintals per hectare (qq/Ha), respectively. Meanwhile, the Central-Eastern region of Entre Ríos and the North-Central region of Córdoba are also continuing harvesting fields with yields close to 66 and 70 qq/Ha, respectively. As for late-planted corn, crop conditions continue to gradually improve, with 89.7% of the surveyed area rated as Normal to Excellent. However, in Central Buenos Aires, Southeastern Buenos Aires, and the Salado River Basin, a predominantly dry scenario persists, maintaining a more challenging situation for the crop in these regions. Under these circumstances, and subject to the evolution of weather conditions accompanying late plantings, a projection of 57 million tons (MTn) remains.

SUNFLOWER: The sunflower harvest shows week-on-week progress of 3.4 percentage points, currently covering 37.2% of the suitable area. Harvesting in the southern regions is still in its early stages due to delays in the fields reaching harvest maturity, with yields varying widely, but averaging 22 to 24 quintals per hectare (qq/Ha), except for Northern La Pampa and Western Buenos Aires, which continues to exceed 28 qq/Ha, approaching the historical high. In addition to the areas that have finished harvesting, Central-Northern Santa Fe and the Northern Core region have also completed their harvests, with yields of 21.9 and 25.6 qq/Ha, respectively, exceeding the average of the last 10 seasons by 6.1% and 11.2%. Given this scenario, the production forecast remains at 6.2 million tons (MTn).

SORGHUM: The grain sorghum harvest is showing early progress, reaching 6.4% of the estimated national area, with initial operations concentrated in north-central Santa Fe and east-central Entre Ríos. So far, yields average 46.7 and 41.7 quintals per hectare (qq/Ha), respectively. Regarding crop development, fields are transitioning from leaf expansion to the beginning of maturity in regions such as the Northeast (NEA) and north-central Córdoba, due to the wide variability in planting dates. There is greater homogeneity in the southern agricultural area, with sorghum ranging from stem elongation to flowering, reflecting a broad range of conditions related to available moisture. Harvesting is expected to gain momentum in the coming weeks as new regions join the harvest. In this context, the production forecast remains at 3 MTn.

Source: Buenos Aires Grain Exchange