Fertilizer prices remain high in the region with no clear signs of decreasing. The direct impact will be felt in the costs of the 2026/27 growing season and in export competitiveness.

As of February 21, 2026, fertilizer prices in Latin America remained high and stable, with firm benchmarks in key markets such as Brazil, Argentina, and India. The global upward trend shows no compelling factors for reversal, and this is important because it directly impacts production costs for the upcoming winter and summer crop seasons, affecting margins, financing, and commercial strategies throughout the region.

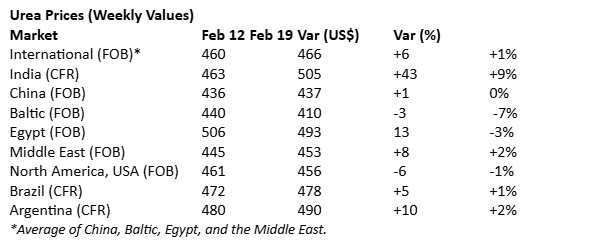

The international urea market maintains strong fundamentals. While a seasonal plateau was observed this week, global supply remains tight for March shipments.

India received bids for more than 3 million tons, with expected awards exceeding US$500/ton CFR, sustaining returns for Gulf suppliers and reinforcing the strength of international trade flows.

In the United States, demand remains strong heading into the spring planting window; in Brazil, activity has slowed due to seasonal factors, and in Argentina, the market remains under-covered for the 2026/27 season, increasing trade risk.

Phosphates: Supply constraints support MAP

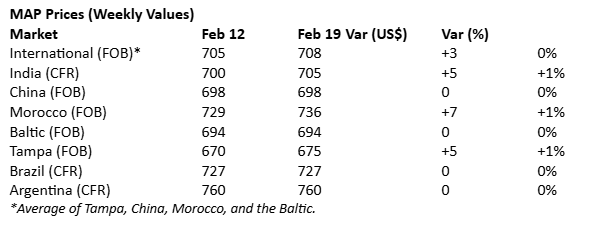

The global MAP and DAP market traded with reduced activity due to holidays, but with structurally sound fundamentals. Weather disruptions in Morocco, Chinese export restrictions, and logistical limitations in Russia are supporting the upward bias.

In Argentina, the wholesale MAP price is around US$865-875/ton, a significant premium compared to Brazil, reflecting the region’s unique supply and cost structures.

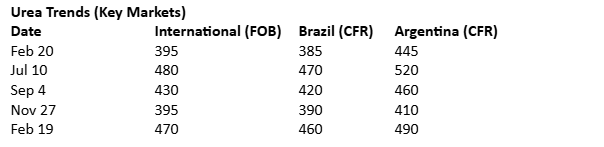

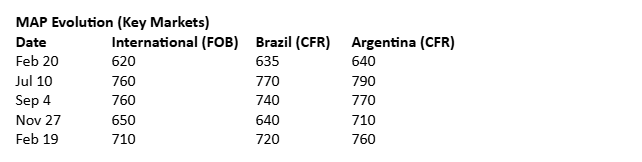

The curve confirms a recovery since November, although still below the July highs, consolidating a scenario of firm prices.

Impact on competitiveness and agri-food chains

For Latin America—a strategic player in global agri-food value chains—stability at high levels puts pressure on the cost structure of soybeans, corn, and wheat, with a direct impact on the trade balance and competitiveness compared to other production hubs.

In a context of high international volatility, the input/output ratio is once again a determining factor for decision-making. Technological advancements, digital agriculture, efficient application rates, and financial optimization will be key to maintaining resilience and profitability.

With no clear signs of a price decrease and the marketing window advancing, hedging and financing strategies are at the heart of 2026/27 planning.

Source: AgroLatam.com

Mosaic misses profit estimates on weak US phosphate demand

The Tampa, Florida-based fertilizer producer warned in January that an unusually sharp decline in North American fertilizer demand during the quarter would pressure sales and cash flow.

Demand for fertilizers has been under pressure as farmers cut nutrient use amid tight budgets, while an early onset of winter shortened the application window.

Sales volumes in the Phosphates segment fell to 1.3 million tonnes from 1.6 million tonnes a year earlier, the company said.

Phosphate markets have tightened as Chinese exports remain largely absent after Beijing extended its phosphate export restrictions, Mosaic said, adding that it expects restrictions to stay in place through at least the first half of the year.

“Like phosphate, potash prices have shifted higher, and current expectations suggest global shipments could reach record levels in 2026,” Mosaic added.

The company said it expects full-year phosphate production volumes to be at or above 7 million tonnes and potash production volumes to be about 9 million tonnes.

Mosaic forecast first-quarter phosphate sales volumes of 1.7 million to 1.9 million tonnes and potash sales volumes of 2.0 million to 2.2 million tonnes.

It also forecast capital spending of about $1.5 billion for the year.

The company reported adjusted earnings of 22 cents per share for the quarter ended December 31, compared with analysts’ average estimate of 47 cents per share, according to data compiled by LSEG.

Source: Reuters

NNPC and Dangote signal deeper cooperation on fertilizer capacity in Lagos complex

A potential expansion of fertilizer production has emerged as a central theme in talks between the Nigerian National Petroleum Company and Dangote Fertilisers, as both sides explore closer strategic collaboration within the Dangote industrial complex in Lagos.

During a visit to the refinery and fertilizer facilities, NNPC Group Chief Executive Officer Bashir Bayo Ojulari said alignment between the two organizations could create value across gas supply, downstream processing, and industrial manufacturing.

He described the fertilizer operations as part of a broader integrated platform designed to convert Nigeria’s natural gas resources into higher-value products, supporting domestic agriculture and foreign exchange earnings.

Aliko Dangote, president of the Dangote Group, said expanding cooperation with NNPC could unlock additional capacity within the existing complex, particularly in fertilizer and petrochemicals. He reiterated that Nigeria stands to gain more by prioritizing domestic processing of raw materials rather than exports, adding that fertilizer production remains a strategic lever for industrialization and economic diversification. Both parties said they would identify priority areas for structured collaboration in the coming weeks.

Source: New Telegraph (Nigeria)

EU imports €900 million of phosphorous from Russia

Despite Russia’s war in Ukraine, the EU has continued to import large volumes of phosphorus from Russia according to a new analysis by Swedish environmental company Ragn-Sells.

In 2025, the EU imported Russian phosphorus products worth close to €900 million, making Russia one of the EU’s largest suppliers of a nutrient critical to European food production.

“No phosphorus means less food and more inflation. As long as Europe remains dependent on imports from a handful of countries like Russia and Morocco, food supply remains insecure. If the EU is serious about food security, it must start recovering the phosphorus already circulating in our wastewater,” said Pär Larshans, Chief Sustainability Officer at Ragn-Sells.

Phosphorus is essential for producing mineral fertilizers and animal feed. Yet almost all phosphorus used in the EU is imported, mainly from Russia and Morocco. The EU’s only active phosphate mine, in Finland, supplies under 10% of European agricultural demand.

In 2025, European companies imported phosphorus fertilizers and phosphates from Russia worth around €890 million, according to preliminary data from the European Commission analysed by Ragn-Sells. While this represents a slight decrease compared with 2024, Russian phosphorus still accounted around one fifth (21%) of the EU’s total phosphorus imports.

“Europe is sleepwalking into a phosphorus crisis. Recognising phosphorus as strategically important and removing remaining barriers to recycled phosphorus is essential for European competitiveness, food security and long-term resilience,” stated Jan Svärd, EasyMining CEO.

EasyMining, a Ragn-Sells innovation subsidiary, has developed the Ash2Phos technology. This process recovers more than 90% of the phosphorus from sewage sludge ash and produces RevoCaP, a high-purity recycled calcium phosphate that can replace imported, mined phosphorus.

Although the European Commission has approved recycled phosphorus for organic farming, a decades-old law still bans its use in animal feed. Sweden is asking the Commission to request a new risk assessment from European Food Safety Authority as a basis for revising the legislation. Sweden and Finland have also urged the EU to stop fertilizer imports from Russia.

“Europe has the technology to produce phosphorus domestically, but outdated rules keep us dependent on imports. Updating an annex in EU feed legislation could unlock significant investment, strengthen competitiveness and reduce dependency on Russia,” commented Pär Larshans.

Source: World Fertilizer.

ARGENTINE MAIN CROPS OVERVIEW

SOYBEANS

Optimal/Adequate soil moisture conditions improved by 10 percentage points. With 72% of the early-planted soybeans entering their critical period and improved moisture reserves, we maintain our production forecast at 48.5 million tons (MTn).

CORN

Harvesting of early-planted corn continues, while soil moisture availability for late-planted crops has improved following recent rains. In central and southern Buenos Aires province, crop development still depends on further rainfall.

SUNFLOWER

After a week-on-week increase of only 0.2 percentage points, the harvest has reached 30.1% of the suitable area. This represents an advance of 7.2 percentage points compared to the historical average. Stable yields maintain the forecast at 6.2 million tons (MTn).

Source: Buenos Aires Grain Exchange