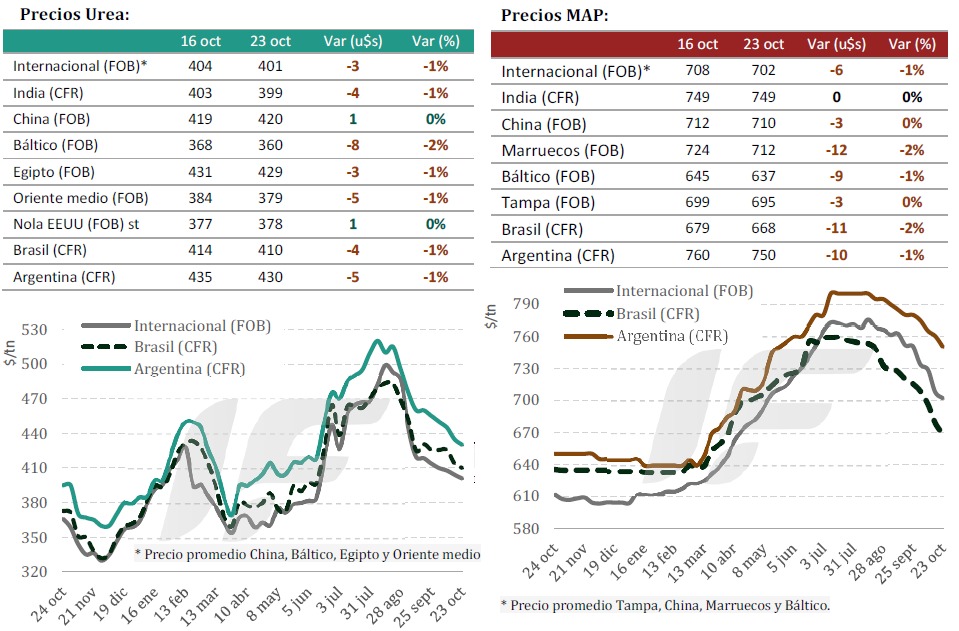

International fertilizer prices continue to weaken in most key agricultural regions, although they remain above the levels recorded a year ago.

This week’s auction of granulated urea by India’s RCF Corporation resulted in prices below expectations and awards falling short of the 2.0 million ton target, reducing seller interest and leaving open the possibility of a new auction in November.

Meanwhile, in China, according to the latest market report from the consulting firm IF Fertilizer Engineering, urea exports accumulated through September significantly exceeded those of the same period in 2024, with sustained shipments to Latin America and Africa.

In the Baltic Sea region, exporters reduced shipments to India to prioritize shipments to Europe and Latin America due to better margins, although activity remains limited. Egypt also prioritized shipments to the EU-27.

The increased European demand stems from the fact that the Carbon Border Adjustment Mechanism (CBAM) will come into full effect on January 1, 2026, which will further complicate the import process for this input.

In Brazil, urea demand remained strong, although the arrival of ships diverted from Asia to this South American destination led to an oversupply that cooled import prices. In Argentina, the market remained cautious, with traders closely monitoring the exchange rate after the legislative elections on October 26.

As for the phosphate market, it continues to consolidate a downward trend due to the inaction of major buyers and the closure of the fertilizer export quota by the Chinese government, in addition to India pausing its imports.

The US, meanwhile, is showing little activity at the port terminals of New Orleans; the financial weakness of US producers, uncertainty regarding the domestic price of soybeans, and import tariffs are maintaining the preference for locally sourced fertilizers.

The Baltic region continues to face weak demand in the European market, while Russia has lowered export prices to facilitate shipments.

In Brazil, demand for phosphates remains selective and focused on replenishment, while Argentina is operating with low volumes and caution due to sluggish domestic demand and an unstable macroeconomic environment.

Source: Valor Soja

Argentina simplifies procedures for importing fertilizers.

The Argentine Customs Revenue and Control Agency (ARCA) has incorporated the submission of declarations and import permits for fertilizers into the Argentine National Single Window for Foreign Trade (VUCEA). This measure aims to simplify procedures and reduce operating costs for foreign trade.

With this update, importers can now process both the “Import Notice” and the “Import Authorization” digitally through an integrated system that centralizes controls and eliminates the need for duplicate authorizations. From now on, the General Directorate of Customs will release the merchandise without requiring additional documentation, provided that the declarations established in the new system have been correctly completed. In practice, this means less bureaucracy, shorter waiting times, and a significant reduction in the logistical costs associated with the import and export of fertilizers and soil amendments.

The impact of this resolution could be felt throughout the entire production chain. In a context where neighboring countries, such as Brazil and Uruguay, are advancing in the digitalization of their customs systems and the reduction of operational barriers, this decision places Argentina in a more competitive position within the regional market for agricultural inputs. The reduction in time and costs not only benefits importers but also producers who depend on these inputs to maintain agricultural productivity and efficiency.

Source: AgroLatam.com

Brazil: Sulfur levels soar 115% in 2025, worrying the fertilizer sector

Tight supply and rising Asian demand sustain high prices and reduce industry margins

Between the beginning of 2025 and the second half of October, sulfur prices at Brazilian ports have already accumulated an increase of approximately 115%, reaching levels similar to those observed in 2022, when the outbreak of war between Russia and Ukraine caused a spike in global fertilizer prices, according to StoneX, a global financial services company.

The current rise in sulfur prices is the result of an imbalance between supply and demand in the international market. On the demand side, Asian countries have been key players. “China, with its robust phosphate fertilizer industry, increased its imports this year, surpassing the volume recorded in 2024. India, on the eve of the Rabi harvest, intensified its purchases to ensure supplies for local fertilizer plants. Other Asian countries have also been prominent, albeit to a lesser extent,” says Market Intelligence analyst Tomás Pernías.

Meanwhile, global supply remains tight. Russian production was hampered by attacks on refineries resulting from the war, forcing the country to seek sulfur from neighboring nations to supply its own industry. In Europe, the shortage is also a concern: regional production remains insufficient to meet demand, further pushing up prices.

“With reduced availability, importers from various parts of the world have redirected their purchases to Canada and the United States, which increases competition for cargo and reinforces the upward scenario,” Pernías highlights.

This price increase impacts the fertilizer supply chain. Although sulfur isn’t directly used in the formulation of DAP (diammonium phosphate), it is an essential raw material in the production chain of certain phosphate fertilizers, and its price increase tends to put pressure on industry margins—especially at a time of falling fertilizer prices on the international market.

“The impact is also felt on SSP (single superphosphate), a fertilizer widely used in Brazil. As the country is a major producer and consumer of this input, fluctuations in sulfur prices can increase its production costs and are a concern for the sector,” the analyst concludes.

Source: Cultivar Magazine

Nutrien shuts down Trinidad nitrogen operations amid gas supply and port access issues

Nutrien has begun a controlled shutdown of its nitrogen operations in Trinidad, citing port access restrictions and a lack of reliable natural gas supply that have made production at the Point Lisas facility uneconomic.

The shutdown, effective October 23, follows months of constrained operations caused by limited access to natural gas and logistical bottlenecks linked to restrictions imposed by Trinidad and Tobago’s National Energy Corporation (NEC). Nutrien said the reduced output has weighed on the facility’s free cash flow contribution “over an extended period.”

The company’s Trinidad operations typically produce about 85,000 tonnes of ammonia and 55,000 tonnes of urea per month. Despite the suspension, Nutrien expects to remain within its 2025 nitrogen sales volume guidance of 10.7 to 11.2 million tonnes, supported by the continued strong performance of its North American plants.

Nutrien said it will continue to engage with local stakeholders and evaluate options for the future of its Trinidad operations, which have faced recurring challenges related to feedstock supply in recent years.

Headquartered in Saskatoon, Canada, Nutrien is one of the world’s largest producers of crop inputs, including potash, nitrogen and phosphate fertilizers, and operates an extensive retail and distribution network serving global agricultural markets.

Source: Fertilizer Daily

Argentine Main crops overview:

CORN:

After a week-on-week increase of 4.1 percentage points, planting covers 33.8% of the national total. While the central agricultural area is beginning to require rain, excess moisture persists in central and western Buenos Aires province.

SUNFLOWER:

After a week-on-week increase of 10.9 percentage points, 51.2% of the projected 2.7 million hectares have been planted. 78.4% is growing under Adequate/Optimal soil moisture conditions, and 99.1% is in Normal to Excellent condition.

WHEAT:

Harvesting has begun, progressing across 5.3% of the suitable area. The average yield is 18.7 quintals per hectare. Of the standing wheat, 84.8% is at the heading stage or beyond, and 88% is in Good/Excellent condition. The production projection is set at 22 MTn.