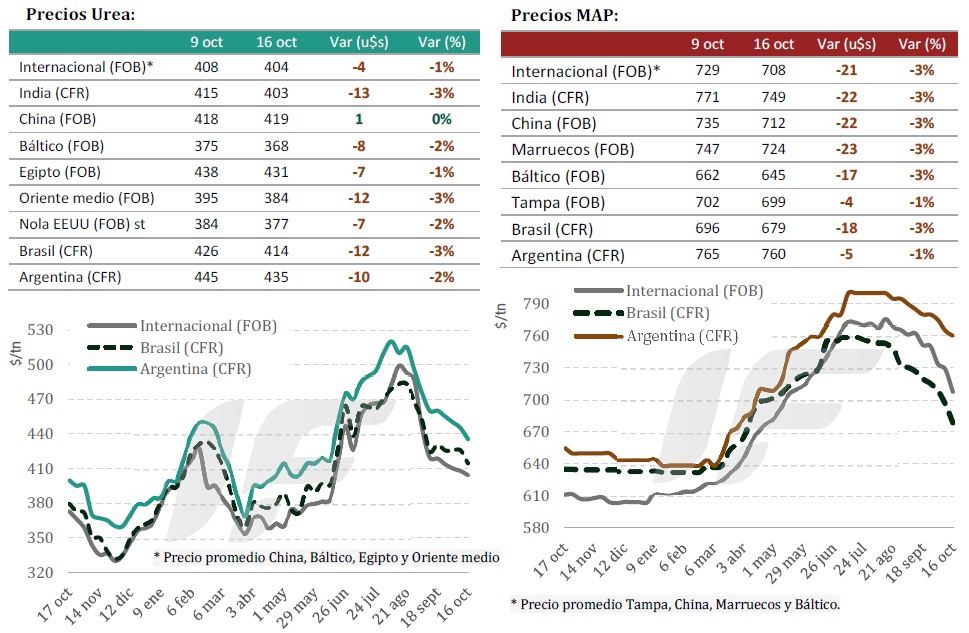

Last week, prices for both nitrogen and phosphate fertilizers continued to fall, aligning with the relative purchasing power of grains.

The granulated urea tender held by Rashtriya Chemicals & Fertilizers (RCF) in India received a higher-than-expected volume of bids, demonstrating that supply far exceeds demand.

“While the volume offered in this tender is well below the record 5.6 million tons from the last tender on September 2, the prices offered are also well below, with the lowest bid for the east coast of India at $395/tonne CFR and $402/tonne CFR for the west coast, respectively, $67 and $62/tonne below the last tender,” states the weekly report from the consulting firm IF Ingeniería en Fertilizantes.

In the US, activity at terminals in the Gulf of Mexico region was very low due to the low consumption season and logistical restrictions on the Mississippi River, with weak domestic demand and no signs of immediate improvement.

In Europe and the Baltic, urea prices weakened due to lower demand from Latin America. In Egypt, lower European demand and limited activity in the available market reflected a cautious market, while Russia showed abundant supply with no prospects of an immediate rebound.

“In Brazil, the market remained stable, with cautious buyers and selective transactions. Urea imports continue to be below the previous year, while ammonium sulfate imports are growing strongly, marking a structural change in demand,” the report notes.

“In Argentina, the market remained stable, but with a downward trend, influenced by the Brazilian decline and the caution of local producers,” it adds.

Meanwhile, the global market for phosphate fertilizers maintained a downward trend, pressured by weak demand, high inventories, and the start of the embargo on exports from China.

“India and Brazil were the focus of attention; the former due to delays in Rabi cycle agricultural subsidies, and the latter due to its oversupply and low commercial activity. Europe and the US showed shrinking markets, while Morocco and Egypt made modest adjustments to their prices,” he notes.

In China, the closure of exports in mid-October halted significant shipments, reducing global availability. Despite this, prices continued to decline, although the shortage is expected to stabilize the market by the end of the year.

In Russia, maintenance work and European tariff restrictions affected export competitiveness, maintaining a moderate sales pace.

In Morocco, the OCP corporation reduced its level of activity and prioritized long-term contracts with India and Bangladesh, while in Egypt the market remained balanced with regular sales to South America (especially Brazil).

Source: Valor Soja.

The risk of a restriction that worries the global fertilizer market

The Chinese government’s measure prioritizes domestic supply and could affect dependent countries, such as Brazil.

The international fertilizer market is operating cautiously ahead of the possibility of China restricting its exports in the fourth quarter of 2025. According to a weekly report from StoneX, a global financial services company, this measure is common in the months leading up to the application season in the Asian country and aims to guarantee domestic supply and control prices for Chinese farmers.

According to StoneX Market Intelligence analyst Tomás Pernías, Chinese authorities tend to prioritize the domestic market during this period, which could compromise the global supply of fertilizers—especially nitrogen and phosphate fertilizers, categories in which China is one of the world’s leading exporters.

“Although this policy is recurrent, there is rarely any predictability in the Chinese government’s decisions. The lack of clarity about when restrictions will be implemented or lifted increases uncertainty and creates instability among importers, who may be forced to seek alternative sources of supply due to the unavailability of Chinese products in the international market,” he states.

In 2024, China’s MAP (monoammonium phosphate) exports accounted for approximately 16% of global exports, reinforcing the country’s importance in the global supply chain. Because MAP is widely used in the Brazilian market, any restrictions on Chinese exports could directly affect supply in Brazil.

For Brazilian importers, the reduction in global supply tends to be negative, as it could intensify competition for cargoes and drive up prices. “For farmers, the scenario is also challenging, especially at a time of high production costs and unattractive terms of trade,” Pernías emphasizes.

Still, it’s important to consider the domestic calendar. In Brazil, purchasing momentum typically slows in the final quarters of the year, as most purchases occur before the summer crop is planted. “Therefore, the impact of a potential Chinese restriction will depend on the type of fertilizer affected and the behavior of demand in each segment,” concludes the analyst.

Source: Cultivar Magazine

Indonesian gran urea sold to Philippines

A trader has sold 7000 t of granular urea to a Philippine importer at US$400/t. The cargo is for shipment in November 2025 from Indonesia.

This deal is up by about US$7/t compared with previous trades in the region, which suggests a potential increase in demand from southeast Asian buyers for November-loading volumes. Most southeast Asian markets will enter the nitrogen application season from end-October to November. But it is unclear how strong urea demand from the region will be, as it would depend on weather conditions and crop prices, both of which influence farmers’ appetites.

Urea inventories in Thailand and Vietnam are high, and importers have not been in the market seeking any fresh volumes in the past month. The last trade in the region was state-owned Pupuk Indonesia’s 8 October sale tender of 45 000 t granular urea at US$393.33/t fob.

Source: World Fertilizer

ARGENTINA MAIN CROPS OVERVIEW:

CORN: Corn planting grew 5 percentage points week-over-week, reaching 29.9% of the projected area nationwide. However, excessive rainfall continues to limit the pace of work in central and western Buenos Aires. As a result of these conditions, it is expected that the initial early planting plans will not be achieved. Therefore, the share of these crops in the total planted area has been adjusted downward: in western Buenos Aires, the estimate has dropped from 44% in September to 35%, while in central Buenos Aires it has fallen from 59% to 32%. Meanwhile, in the central agricultural area, early corn planting is practically complete, with only a few specific plots remaining in the Core Zone and in Córdoba, whose implementation is expected to be completed in the coming days.

SUNFLOWER: As for sunflowers, work is beginning to regain momentum, entering the optimal planting window for the agricultural south. Despite some delays caused by weekend rains, week-over-week progress of 5.3 p.p. was achieved, covering 40.3% of the projected 2.7 Mha to date. This progress continues to exceed the previous cycle and the average for the last five years by 16.1 and 6.2 p.p., respectively. 78.4% of the standing area shows Adequate to Optimal water conditions, allowing 99.1% of the sunflower crop to maintain Normal to Excellent crop condition. Regarding phenology, while planting is beginning in the south, in the NEA and North-Central regions of Santa Fe, the area in flower bud stage has reached 78% and 33%, respectively.

WHEAT: In the case of wheat, 70.6% of the crop is currently progressing from the heading stage onward and is entering key yield definition stages. The highly favorable conditions under which the cereal has developed continue to elevate yield expectations above average. Although available moisture has begun to decline due to both evaporation and crop demand following the rise in temperatures, 72.8% of the area still exhibits Adequate to Optimal moisture levels. Consequently, 89.9% of the wheat crop maintains a Good to Excellent condition. Faced with this scenario, producers continue to carry out applications against pests and diseases, in some cases preventively, to safeguard the crop. However, forecasts warn of an incoming cold air mass next week which, depending on its intensity and distribution, could affect the cereal during these critical stages.

BARLEY: Regarding barley, at the national level, 90% of the crop is rated under Good/Excellent condition, with 8 out of every 10 hectares maintaining Adequate/Optimal water condition. For the most advanced plots in the center of the agricultural area, yields are expected above the historical average as a result of timely rainfall. In the central and southern regions of Buenos Aires, high humidity has favored the appearance of diseases such as “net blotch” and other fungal diseases, driving the continuation of fungicide applications. Nevertheless, with 40% of the crop progressing through the heading stage, 80% of the plots exhibit a good crop condition, projecting yields above the historical average. Within this context, we maintain our production forecast at 5.3 Million Tons (MTn).