The temporary suspension of export duties had no major impact on fertilizer demand, despite initial expectations in the agricultural nutrient industry.

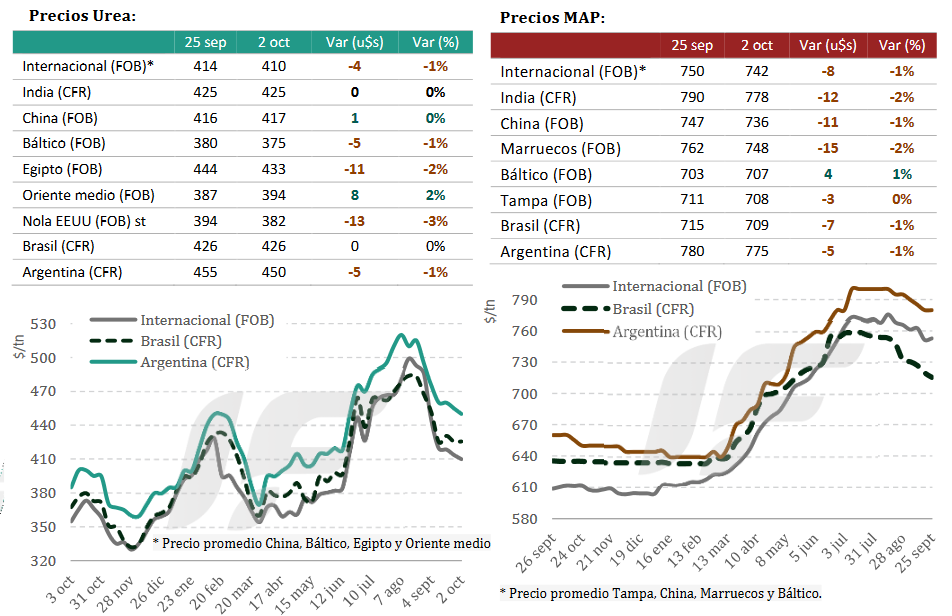

Within this context, fertilizer prices in the Argentine market continued to decline, matching the international price decline.

The main reason for this phenomenon is that the suspension of export duties had a limited to zero effect on cereals, which are the largest fertilizer consumers.

This week, an increase in exportable supply from China continued to drive down prices for phosphate fertilizers, amid a global demand that shows limited purchasing power.

“In addition to the poor demand for phosphate fertilizers that Argentine producers have shown throughout the year, importers are now beginning to face the final quarter of the year with a still uncertain demand before the end of the main planting season,” states the latest report from the consulting firm IF Ingeniería en Fertilizantes.

“While this expected price drop by Argentine producers could boost demand, it is working against inventory values, which are beginning to erode with the drop in international prices,” it adds.

The reference import price for monoammonium phosphate in Argentina this week stood at US$775/ton CFR, US$5.0/ton lower than the previous week.

On the urea side, international prices continued their downward trend until late this week, when India announced a new tender to purchase 2.0 million tons with a closing date of October 15. This halted the downward trend.

“This reversal in international urea prices was quickly reflected in CFR prices in the Argentine market, with offers rising to US$450 from US$440/ton at the beginning of this week. However, there has been no change in the trend in local prices,” the report notes.

“It is expected that, at the beginning of next week, importers will stop rushing urea deals by lowering prices, as has been the case in recent weeks, and will begin to defend their positions based on how international prices evolve,” the consulting firm projected.

Source: ValorSoja

Use of less concentrated fertilizers will skyrocket in 2025

Demand for lower-concentration fertilizers is gaining momentum in the Paraguayan and Brazilian markets in 2025, according to the weekly fertilizer report from StoneX, a global financial services company. Between January and August, Paraguay’s imports of SSP (single superphosphate) grew 25% compared to the same period the previous year, while NP, a nitrogen and phosphorus-based product, increased 38%. Conversely, purchases of MAP, a higher-concentration phosphate, fell 13% compared to 2024.

This isn’t an isolated move, as the growth in purchases of less concentrated fertilizers in Brazil also signals a strategic shift by producers. Faced with trade terms at their worst levels in recent years, high prices, and limited global supply, buyers are seeking more affordable alternatives to maintain crop fertilization without compromising profitability.

“The market has been adjusting to a scenario of tighter margins and still-high costs. Choosing lower-concentration products, such as SSP, is a strategy to maintain agronomic efficiency without compromising producers’ cash flow,” assesses Market Intelligence analyst Tomás Pernías.

In the nitrogen segment, the trend is similar. Paraguayan imports of ammonium sulfate, a product with a lower concentration than urea, are 15% higher than in 2024. Purchases of urea, a product with a higher nitrogen content, increased only 4%, reinforcing the trend of partial substitution by more economical options.

Source: Cultivar Magazine

European Union opened anti-dumping investigation into Russian urea fertilizer imports

The European Union has initiated an anti-dumping investigation into imports of urea fertilizer from Russia following complaints from European producers that Russian shipments are undercutting market prices.

Industry group Fertilizers Europe argued that Russian exporters benefit from artificially low, state-controlled natural gas prices, a key input in urea production. This pricing advantage, the group claims, enables Russian producers to outcompete EU rivals, according to the official notice launching the probe.

Russia remains a major urea supplier to the EU, particularly after the loss of Russian natural gas deliveries forced many European fertilizer plants to scale back or shut down. The bloc’s reliance on Russian imports has raised concerns that Moscow could manipulate supply, either by raising prices or flooding the market with excess product, putting additional pressure on European farmers.

The investigation will review imports between July 2024 and June 2025. If evidence of dumping is confirmed, the EU could impose tariffs on Russian fertilizer shipments.

Source: Bloomberg

ARGENTINE MAIN CROPS OVEVIEW:

CORN: Corn planting saw an inter-week progress of 7.4 percentage points (p.p.), reaching 19.8% of the 7.8 Million Hectares (MHa) estimated for this campaign. Favorable soil moisture is allowing for the execution of early planting plans, resulting in a year-on-year advancement of 7 p.p. However, in regions such as the west, center, and northeast of Buenos Aires, poor field conditions and impassable roads have slowed the planting pace. Conversely, in other areas like central Santa Fe and Entre Ríos, plots already between the V2 and V4 stages are beginning to show a good response to fertilization.

SUNFLOWER: Of the new projected sunflower area of 2.7 MHa (+ 100 thousand Ha vs. previous projection), 32.4% has been planted following an inter-week progress of 1.4 p.p. This maintains significant advancements compared to the last five-year average (12.3 p.p.) and the previous cycle (22.1 p.p.). Over the last week, rainfall occurred across various parts of the agricultural area, primarily benefiting the western agricultural regions (San Luis province, central and southern Córdoba, northern and eastern La Pampa). Meanwhile, the center-west of Buenos Aires and southern Santa Fe are once again experiencing situations of aggravated water excess. As a result, collaborators report that the start of planting activities in these sectors will be delayed and subject to the evolution of both rainfall and temperatures. Regarding the standing area, 100% is rated under Normal to Excellent crop condition, and the first plots in the northern part of the country are beginning to show flowering, with high yield expectations.

WHEAT: In the case of wheat, the aforementioned rains have had a mostly positive impact. Although no hectares were under restrictive moisture conditions, this input is timely and beneficial given rising temperatures and the fact that 80% of the cereal is progressing from stem elongation onward. While phytosanitary applications continue for the control of fungal diseases and pests, estimated yields continue to rise, approaching historical highs. Furthermore, collaborators in the NOA (Argentine Northwest) report the first harvested plots, with yields averaging around 10 quintals per hectare (qq/Ha), aligning with currently projected values.

BARLEY: Nationwide, following the latest rainfall, 88% of the planted barley area shows an Adequate/Optimal water condition, and almost 9 out of 10 hectares maintain an Excellent/Good crop condition, consistent with the previous report. In this context, 13% of the plots have begun the heading stage and 1% the flowering stage, mainly in the northern and southern core regions. In southern Buenos Aires, high humidity has favored the emergence of diseases such as “net blotch,” prompting continued fungicide applications. However, with 60% currently in the stem elongation period, 75% of the plots in the southern barley core regions maintain a Good/Excellent condition, supported by optimal soil moisture levels.

Source: Buenos Aires Grain Exchange