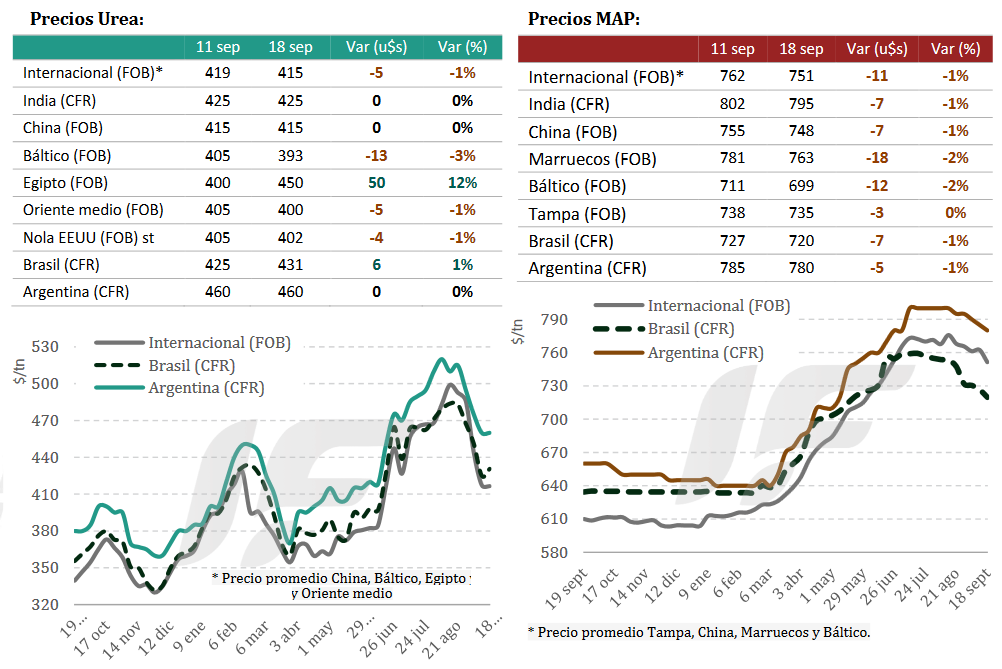

The international urea market continues to be characterized by abundant supply that is not matched by demand, although there are signs that prices appear to be seeking a “floor.”

“In India, prices are holding steady following the purchase of 2.0 million tons in the tender held on September 2. With stocks of 2.7 million tons nationwide and 462,000 tons in ports, the market expects new purchases, although saturation of arrivals could delay this,” notes the weekly report from the consulting firm IF Ingeniería en Fertilizantes.

Meanwhile, in Brazil, prices this week traded within a range of US$420-440/ton CFR for delivery in September-October 2025, with confirmed shipments from Iran (65,000 tons), Russia (41,000 tons), China (67,000 tons), and Nigeria (25,000 tons).

In Argentina, prices remained unchanged at US$460-465/ton CFR, with limited trade and a week characterized by a shortage of physical urea at the ports in Rosario’s area of influence. “The shortage is widely observed for new sales, with importers only committing availability from October 15 onward,” the report notes.

“On the other hand, some importers reported shortages for deliveries of already completed deals, a situation that will begin to normalize starting this weekend with the arrival of new ships carrying urea. However, complex weeks are expected regarding the supply of this product,” he warns.

With the improvement in soybean prices and the drop in the price of urea, demand for the fertilizer has been reactivated, but suppliers’ response capacity has been limited. “A period of 15 to 20 days of tension is expected, which could lead to trade frictions and some late applications,” he projects.

IF Engineering in Fertilizers noted that while the decision to fertilize in the field can be made overnight, import management requires a period of 40 to 70 days from shipment at origin to arrival at Argentine ports.

Regarding the global phosphate market, it had a bearish week. Oversupply from China, a halt in purchasing in India and Bangladesh, and high stocks in Brazil put downward pressure on prices. Morocco and Russia also adjusted their reference prices, while in the US, diammonium phosphate (DAP) prices at the ports of New Orleans (NOLA) remained relatively stable, but with declines in monoammonium phosphate (MAP).

In Brazil, MAP entered the market in a range of US$710 to US$730/ton CFR. Imports so far in September reached 273,000 tons, mainly from China, Saudi Arabia, and Morocco.

In Argentina, MAP was offered at US$780–US$785/ton CFR, while DAP remained at US$770–US$775/ton with no significant transactions. The differential with Brazil exceeded US$60/ton, complicating transactions.

“Phosphate products continue to experience limited commercial activity in the Argentine market. There are already signs of some importers trying to stimulate sales to move stock, which has led to somewhat more aggressive prices this week, especially considering an international scenario where prices continue to decline due to the persistent lack of demand,” the report notes.

Source: Valor Soja

Ammonium sulfate gains prominence in the fertilizer market

Rising fertilizer prices and unfavorable exchange rates are driving the search for less concentrated products

Ammonium sulfate (AMS) has been gaining prominence in the Brazilian market in recent months. The increase in demand for fertilizers, according to a weekly report from StoneX, a global financial services company, was expected in the run-up to summer. However, the preference for less concentrated fertilizers has been one of the factors driving this increase.

“At this time, it is estimated that the amount of ammonium sulfate expected in Brazilian ports, especially in Santos and Paranaguá, far exceeds the volume of urea estimated to arrive in the country,” highlights the Market Intelligence analyst, Tomás Pernías (in the picture).

By 2025, high fertilizer prices and unfavorable terms of trade led importers to seek more competitive alternatives. “The need for nitrogen and phosphates is being partially met precisely by these lower-concentration products, which require larger quantities in tons to provide the same amounts of nutrients that would be present in higher-concentration products,” he says.

As a result, this choice increased the total volume of fertilizers entering Brazil, intensifying port traffic, precisely at a time of traditionally strong demand. “According to information collected by StoneX, this preference for lower-concentration products is likely to continue in the coming weeks,” he emphasizes.

Given this scenario, nitrogen imports are expected to remain strong in the final months of the year, mainly due to the need to supply the second corn crop, a crop that demands high levels of nitrogen. “Consequently, the market remains vigilant to determine whether ammonium sulfate will maintain its leading position in imports or whether urea will regain ground by the end of 2025,” he concludes.

Source: Cultivar Magazine

APC, Sinofert renew MOP agreement for 2026-28

Jordanian potash producer APC and Chinese importer Sinofert have extended a potash agreement which will see Sinofert continue to be the exclusive marketer for APC’s potash products in China to 2028.

The new agreement renews a similar agreement signed between the two parties in 2022, which expires this year.

APC will supply Sinofert with potash during this three-year period. The volumes agreed have not been disclosed.

In 2023-24, China imported 1.1 mn t from Jordan, according to GTT. Of this total, 374,102t was imported in 2024.

Source: Argus Media

ARGENTINA’S MAIN CROP OVERVIEW:

CORN: Over the past few days, producers have intensified their planting pace of grain corn due to the approaching storm front. This situation has led to accelerated crop yields, seeking to take advantage of current soil conditions before the onset of precipitation that could disrupt progress. To date, planting progress is estimated to have reached 6.2% of the 7.8 million hectares projected for the 2025/26 season. In Córdoba, good water availability is driving early planting, where it could represent 25% of the plantings, in contrast to the previous season, where it represented 15%. Likewise, in the core zone, the good humidity is being taken advantage of, and producers agree that early planting could exceed 80% of the total for the area.

SUNFLOWER: Planting progressed 1.2 percentage points week-over-week, reaching 25.6% of the projected area (2.6 Mha), reflecting advances compared to the average for the last five campaigns and the previous cycle: 5.6 and 17.3 percentage points, respectively. Planting was concentrated in the central-eastern part of the agricultural area (Northern Core and Central-Eastern Entre Ríos), unlike in the central-northern part of Santa Fe, where planting slowed, giving priority to corn. Regarding the area already planted, good plantings are observed in the north of the country, responding favorably to the rainfall recorded in recent weeks.

WHEAT: This week’s rainfall, concentrated in the NEA region, directly benefits the cereal, which is currently in the earing and grain-filling stages in 93% of the area. Meanwhile, in the central and southern agricultural areas, as a result of high water availability, there has been an increasing application of fungicides to manage rust and yellow spot, and in the most difficult fields with waterlogging, some cases of chlorosis and nutrient leaching have been observed. However, 97.1% of the area is in Normal to Excellent crop condition, while 54.6% is already in critical stages (from stem-setting onward), maintaining high production expectations for the cereal.

BARLEY: Regarding barley, nationwide, 91% of the planted area has adequate/optimal water conditions; consequently, 88% of the crops are in normal/good condition. In this context, 66% is in full tillering, while 32% has already begun the tillering stage, mainly in the central region. In the southern barley areas, 82.5% is in normal/good condition. Fungicide applications have begun following the recent rains.

Source: Buenos Aires Grain Stock