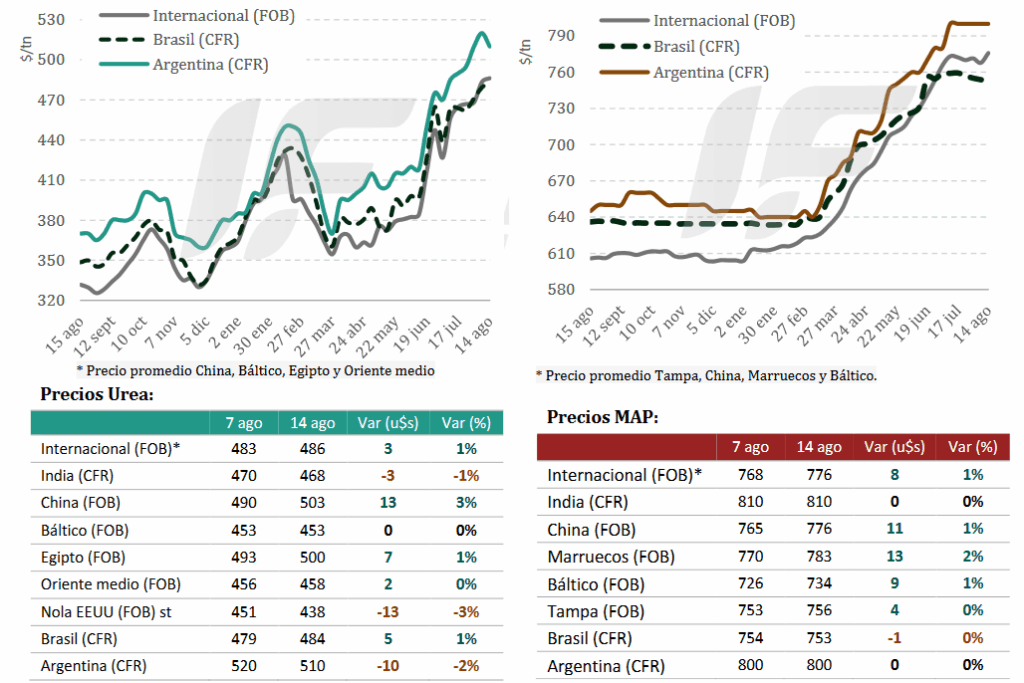

International fertilizer prices, after reaching record highs, are experiencing fluctuating situations across different markets due to the specificities of each market.

India this week held an import tender for 2.0 million tons of granulated urea and announced that it will launch a new tender for an additional 1 million tons in two weeks. “This move confirms that we are on track to see high urea prices for at least 30 to 45 more days,” states the latest report from the consulting firm IF Ingeniería en Fertilizantes.

The US (NOLA) showed a calm market with export prices adjusting, while Brazil saw urea import prices rebound with shipments from Algeria, Nigeria, and Middle Eastern countries.

“Argentina saw a price drop of US$10/ton compared to other weeks; this downward pressure stemmed from expectations of increased arrivals from the Middle East and Nigeria, moderately growing demand, and low immediate demand from major consumers. It was a week in which market participants focused on adjusting price differentials, which are now at more reasonable levels compared to Brazil,” the report states.

In the Argentine market, virtually no one is willing to sell below a wholesale price of US$600/ton. “This context is leading many Argentine producers to reconsider application rates,” notes IF Engineering in Fertilizers.

In any case, purchases of both urea and phosphate fertilizers are beginning to gain momentum to secure fertilizers for agricultural designs during the heavy rain season.

With this upswing in demand in Argentina, companies began to adjust prices for both phosphorus and urea upward, bringing the prices offered closer to replacement prices. “There are fewer and fewer farmers sustaining low prices per volume,” the report notes.

In addition to meeting the needs of the major crop season, demand in the southern Pampas region is also mobilized to fertilize wheat and barley crops, which are in excellent condition.

In the global phosphate market, prices remained stable in several key origins, although with occasional movements in large-volume transactions.

India made massive purchases of diammonium phosphate (DAP) to ensure supply, purchasing 600,000 tons from Saudi Arabia for shipments in September and October.

In Bangladesh, the Ministry of Agriculture set maximum import prices for DAP and triple superphosphate (TSP), while China maintained export restrictions, and no new quotas are expected for the remainder of the year. Meanwhile, in Morocco, the state-owned OCP sold DAP to Asian destinations at stable prices.

The Brazilian market saw very low purchasing activity, influenced by seasonality and financial constraints affecting producers. Brazilian buyers prioritize cheaper alternatives such as single superphosphate (SSP), given the relatively high prices of monoammonium phosphate (MAP).

In Argentina, no large-volume transactions were recorded, but product availability is adequate thanks to prior contracts and secure logistics. Price stability reflects a market without immediate pressure.

Source: Valor Soja

NATO sanctions on Russia threaten agricultural costs in Brazil

The measure could restrict access to Russian fertilizers, which represent more than 25% of Brazilian imports.

A new geopolitical risk has come to the fore after NATO’s secretary-general, with US support, threatened to impose secondary sanctions on countries that trade with Russia. The measure could directly affect Brazil, which relies on Russian fertilizers for 26% of its imports. This is according to Agro Mensal, a report published by Itaú BBA’s Agro Consulting.

In a scenario of restrictions, the country would have to seek alternative, possibly more expensive, suppliers, which would increase agricultural production costs. This situation could worsen the already unfavorable situation for producers, especially grain producers, who face less advantageous exchange rates between agricultural products and fertilizers.

According to the document, nitrogen prices remain high in the market, with urea rising 5,2% in July to USD 455/t at Brazilian ports. Potassium and phosphate prices remained stable, with MAP (monoammonium phosphate) falling 0,3% in the month to USD 757,5/t, and KCl (potassium chloride) remaining at USD 362,5/t.

Russia stands out as a readily available supplier and, in general, more competitive than other sources. In 2024, 53% of Brazil’s MAP and 40% of its KCl imports came from the country, while Russia’s share of urea was 20%.

The supply of nitrogen has already been suffering disruptions since the beginning of recent conflicts, according to Itaú BBA. Urea plants in Egypt have shut down, activity in Iran has been reduced due to the Israel-Iran war, and in July, a Russian nitrogen plant was hit by a drone. This situation has led countries with centralized purchasing, such as India, to anticipate purchases as a precaution. Thus, even with the drop in international prices of natural gas—the main input for nitrogen—urea and other products remain on an upward trajectory.

Source: Cultivar Magazine

Mosaic sells its Brazil potash mine for $27 million to mitigate market pressures

Mosaic has agreed to sell its Taquari-Vassouras potash mine in Brazil to VL Mineração for up to $27 million in cash, with the buyer assuming about $22 million in asset retirement obligations.

The transaction, pending approval from Brazil’s Administrative Council for Economic Defense, will be paid in installments: $12 million at closing, $10 million after one year, and $5 million over six years. Mosaic said the mine would require more than $25 million in new capital to remain viable and that the proceeds from the sale could yield better returns if invested elsewhere in its portfolio.

According to the company, VL Mineração has indicated it is prepared to make the investments needed to extend the mine’s operational life.

Mosaic’s South American operations include potash and phosphate facilities in Brazil, Paraguay and Peru. Shares in the New York-listed company rose 2.89% on Wednesday morning, giving it a market capitalization of about $10.1 billion.

The sale comes as Mosaic faces softer fertilizer demand and tariff-related pressures. Shares fell as much as 13% on Wednesday, the steepest drop since May 2022, after the release of second-quarter earnings. The company reported weaker sales volumes, citing the impact of US tariffs on phosphate imports, which have reduced combined phosphate and potash imports by about 20% so far this year.

Mosaic’s executive vice president of commercial, Jenny Wang, said falling corn and soybean prices, coupled with “global trade uncertainty,” have tightened farmers’ nutrient budgets. The company posted an $8 million loss in its phosphate segment for the quarter as planned maintenance projects took longer than expected, further weighing on sales volumes.

Fertilizer Daily

ARGENTINA MAIN CROPS OVERVIEW:

SUNFLOWER: To date, sunflower planting covers 12.8% of the projected area for the 2025/26 season. Despite the lack of rain this week, available moisture has favored an accelerated planting pace. Particularly noteworthy is the progress of work in early-season areas, reflecting a year-over-year advance of 12.4 percentage points and a 6.8 percentage point increase compared to the average for the last five seasons.

WHEAT: Regarding wheat, the climate favored the recovery of part of the area in regions affected by excessive water, although flooding is still observed. However, in the north of the country, it is estimated that nearly half of the planted area is already in the process of tillering, and although the water supply exceeds that of previous cycles, it would be ideal to have new contributions to sustain high yield potential. At the same time, in the central and southern agricultural area, the transition between phenological stages remains closely linked to temperature trends and is therefore still in the vegetative stages.

CORN: Meanwhile, the grain corn harvest recorded week-on-week progress of 5.3 percentage points, reaching 94.6% of the estimated total for the 2024/25 season, with an average harvested yield of 72.1 t/ha. It is worth noting that harvesting has concluded in the north-central region of Córdoba with good results, around 80.4 t/ha. Harvesting has also concluded in Entre Ríos province with an average yield of 69.4 t/ha, and also in the northern core region, with yields of 93.9 t/ha. In the most backward areas, corresponding to the center and south of Buenos Aires, harvesting has progressed to 83.9% of the estimated total, with an average yield of 69.4 t/ha. In this context, we maintain our production projection at 49 MTn. Meanwhile, the first data are beginning to be collected from plots planted for the 2025/26 season in some areas of central Santa Fe and Entre Ríos, where soil temperature and good water availability allow planting to begin.

SORGHUM: The grain sorghum harvest is now complete across the entire national agricultural area after a 5 percentage point increase in the two-week period, reporting an average harvested yield of 35.1 t/ha (average yield for the last five campaigns: 35.8 t/ha), although some plots remain to be harvested, which would not affect our estimates. Both the core zone and the north-central region of Córdoba were the best performing areas, with yields of 57 t/ha and 52.8 t/ha, respectively. On the other hand, the regions with the greatest relative area weight (NE and north-central Santa Fe) were the regions most affected by water stress during the crop’s growth period, so this campaign’s results decreased to 26.5 t/ha and 32.4 t/ha, respectively. In this context, final production for the crop is estimated at 3.1 MTn, i.e., approximately 100,000 tons above the previous season’s figure.

Source: Buenos Aires Grain Stock