Last week, the international price of urea continued to rise, driven by a tender held by India. Indian Potash Limited received bids for 2.6 million tons to purchase 2.0 million at prices of US$530-532/ton CFR. Shipments are scheduled for next September, and the next tender is expected in the first half of September.

“Analysts view these prices as a ceiling for 2025, with possible corrections if new demand does not emerge before the next tender scheduled for early or mid-September,” notes the weekly report from the consulting firm IF Ingeniería en Fertilizantes.

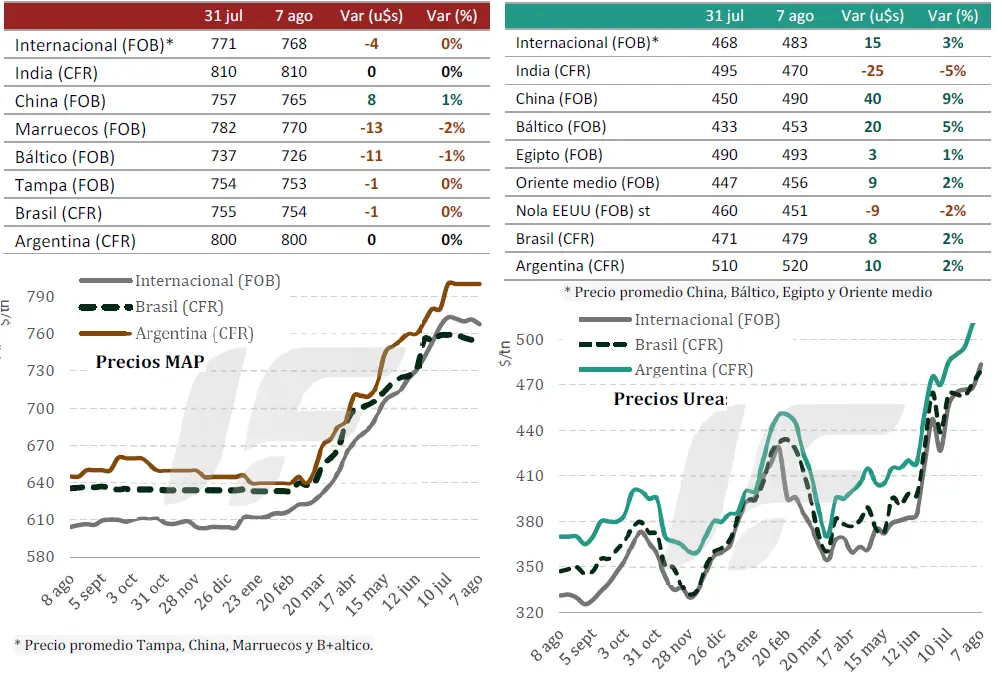

China has allowed urea exports to India, but will reduce availability starting in October of this year due to its domestic season, while Egypt and Middle Eastern nations maintain high prices for nitrogen.

“Supply is tight, but the absence of other major buyers and the closing of the Indian window could generate downward pressure. Factors such as the Trump-Putin meeting and the European energy outlook also play a role,” the report notes.

Meanwhile, the Brazilian urea market is experiencing a challenging situation, marked by a combination of high prices and low trading activity.

The weakness in domestic demand persists and is also spreading to Argentina, where urea has been adjusting upward but has stabilized at US$600/ton in the wholesale market, while liquid NS solutions have yet to react to the rise in urea prices.

For its part, the international phosphate market was mainly influenced by the Bangladeshi auction—which attracted Chinese producers—while in India, buyers remain reluctant to accept prices above US$810/ton CFR.

The US Gulf registered a slight correction after last July’s peak, with diammonium phosphate (DAP) trading in the range of $800–$810/tonne FOB.

In the Baltic, DAP fell to $710–$749/tonne FOB, while monoammonium phosphate (MAP) remained stable at $728–$733/tonne. Morocco posted increases, with DAP trading between $779–$815/tonne FOB, and DAP sales to Europe at $850–$855/tonne.

“In Brazil, the market remains stable, although with little activity. MAP is quoted between US$750 and US$755/ton CFR, but purchase offers are significantly lower, around US$710/ton, highlighting a gap between sellers’ and buyers’ expectations. There are no signs of immediate demand recovery, as farmers have not yet finalized their purchases for the soybean season,” the consultancy firm comments.

The Argentine MAP market remains inactive, with reference prices close to US$800/ton CFR. “Unlike Brazil, no upcoming shipments or significant logistics movements are reported, indicating a cautious stance on the part of buyers,” it notes.

“Phosphate prices remained stable this week in the Argentine market and continue to be below the replacement price, in an international context that shows no signs of falling prices in the short term, so it’s a good decision to purchase phosphates early today. NPS and NPS+Zn chemical sources are a very competitive option compared to MAP and DAP prices,” the report summarizes.

Source: Valor Soja by Valor Soja, August 8, 2025

PhosAgro reports higher output and earnings in H1 2025

According to its consolidated interim condensed financial statements for the six months ended June 30, PhosAgro Group increased production, sales, and earnings in the first half of 2025.

Output of agrochemical products rose 4% year-on-year to 6.12 million tonnes, with phosphate fertilizers and feed phosphates up 6% to 4.69 million tonnes. Total sales volumes grew 2.4% to 6.24 million tonnes, including a 2.8% increase in phosphorus-containing fertilizers and feed phosphates.

Revenue rose 23.6% from a year earlier to 298.6 billion rubles. EBITDA advanced 26.8% to 94.6 billion rubles, while adjusted EBITDA increased 50% to 115.3 billion rubles. Free cash flow more than doubled to 56.5 billion rubles.

As of June 30, net debt stood at 245.7 billion rubles, with the net debt-to-EBITDA ratio down to 1.25x.

The company reported strong shipment growth to India — up almost 41% — driven by Chinese export restrictions for much of the period and favorable pricing. Shipments to Africa and Europe also recorded significant gains.

Source: Fertlizer Daily

CF Industries reports on 1H25 earnings

CF Industries Holdings, Inc., a global manufacturer of hydrogen and nitrogen products, today announced results for the 1H25 and 2Q25 ended 30 June, 2025.

Highlights

- 1H25 net earnings of US$698 million, or US$4.20 per diluted share, EBITDA of US$1.37 billion, and adjusted EBITDA of US$1.41 billion.

- 2Q25 net earnings of US$386 million, or US$2.37 per diluted share, EBITDA of US$757 million, and adjusted EBITDA of US$761 million.

- Trailing 12 months net cash from operating activities of US$2.50 billion; free cash flow of US$1.73 billion for same period, which includes cash inflows and outflows associated with Blue Point joint venture.

- Repurchased 8 million shares for US$202 million during the 2Q25.

- Donaldsonville carbon capture and sequestration project began generating 45Q tax credits for permanent sequestration of carbon dioxide in July 2025.

“The CF Industries team worked safely and delivered outstanding operational performance against the backdrop of constructive global nitrogen industry dynamics, helping drive strong financial results in the 1H25,” said Tony Will, president and CEO, CF Industries Holdings, Inc. “We also have reached a historic milestone in our company’s decarbonisation journey with the start up of the Donaldsonville CCS project and measurable emissions reduction.

We are realising the financial benefits of investing in low-carbon ammonia production through both 45Q tax credit generation and the premium that these low-carbon tons command in the global marketplace.”

Source: World Fertilizer

ARGENTINA: MAIN CROP OVERVIEW

WHEAT: After a week-over-week increase of 1.7 percentage points, the 2025/26 wheat planting season is complete, with a total national area estimated at 6.7 million hectares. Although some plots yet to be planted are reported, these would not change the current estimate. Regarding phenology, 38.2% of the wheat in northern Argentina is in the stem stage and shows good yield potential. Meanwhile, in the central and southern agricultural area, 100% of the wheat remains in the vegetative stage, maintaining a Normal to Excellent crop condition across 99% of the planted area. Despite persistent excess water levels in central and southeastern Buenos Aires, the national water condition is Adequate to Optimal across 81.9% of the standing area.

BARLEY: Regarding barley, sowing is nearing completion, with 98% of the fields already planted. Only the last fields located in the southern part of the agricultural area remain to be sown. Over the last two weeks, sowing progress was 6.9 percentage points, although a year-on-year delay of 2 percentage points has been recorded. In the southeast and southwest of Buenos Aires, 30% of the fields are currently in the tillering stage, while the entire planted area is in normal to good condition, thanks to adequate water availability during sowing. However, the first symptoms of foliar diseases are beginning to be detected in some fields.

CORN: Over the last seven days, the grain corn harvest advanced 1.3 percentage points, reaching 89.3% of the national total, with an average harvested yield of 72.3 t/ha. In the northern agricultural area, the harvest is over 90% complete, although yields were below initial expectations, with specific exceptions, such as southern Santiago del Estero, where the campaign concluded with favorable results. In the central-western region, the harvest is also nearing completion, recording average yields between 75 and 80 t/ha. Meanwhile, in the southern agricultural area, producers continue to wait for the fields to reach optimal moisture content for harvesting, with 25% of the area still to be harvested, with yields averaging 70 t/ha. In this context, a production projection of 49 MTn is maintained.

SUNFLOWER: The 2025/26 sunflower campaign has begun with 7.2% planting progress on a projected 2.6 million hectares. So far, work has been concentrated in the northeast of the agricultural region, in prime areas for the oilseed. Unlike in recent years, the campaign has begun with good reserves in the crop profile, allowing it not only to recover the area lost in previous campaigns but also to plant them in the optimal planting window.

Source: Buenos Aires Grain Stock