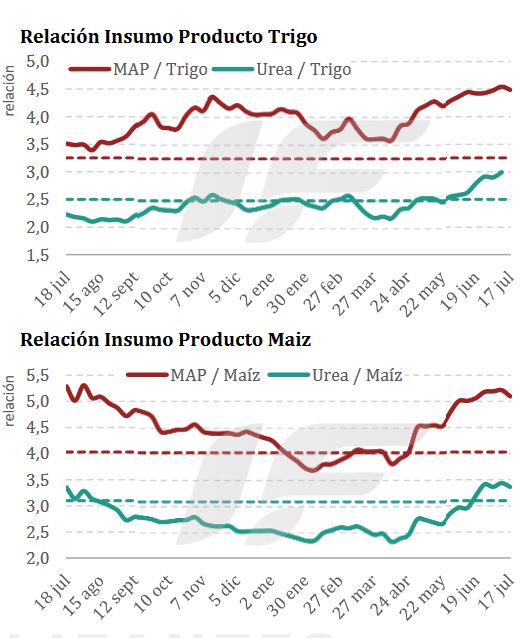

Considering current international prices, urea should exceed US$600/ton and phosphorus US$900/ton in the Argentine wholesale market, although the prices of both fertilizers remain lower due to weak domestic demand.

This week, transactions were once again scarce, and concern is growing in the sector ahead of the 2025/26 harvest season.

“It should be noted that if the international market remains strong and there are no significant declines—a situation that seems unlikely in the short term—local prices are expected to eventually adjust to these international levels once importers liquidate their inventories purchased at previous prices,” according to the latest report from the consulting firm IF Ingeniería en Fertilizantes.

“In addition, this week there was a notable disparity in the prices offered by different importers, with differences of up to US$30-35/ton between alternatives. This shows both the anxiety of some operators to close deals and the short position of others’ inventories, depending on the perspective from which it is analyzed,” it adds.

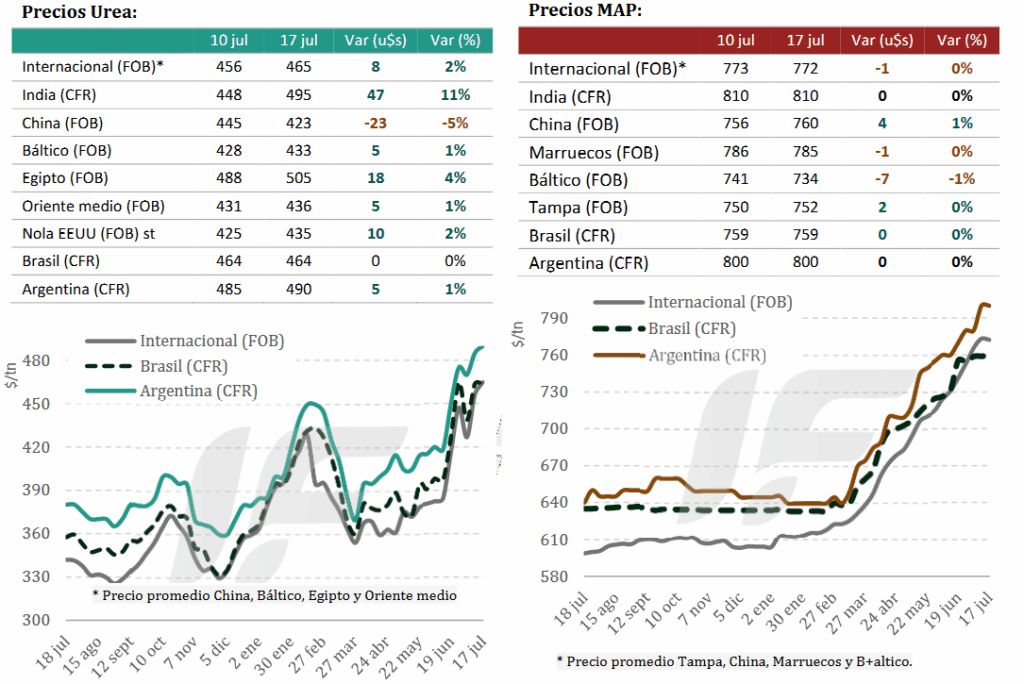

The global urea market showed signs of stability this week, reaching an apparent ceiling after India’s recent purchase of 1.5 million tons, which helped sustain high prices worldwide. India anticipated a new tender for mid-August, forecasting additional demand of approximately one million tons over the next three months.

“In contrast, global demand outside India is moderate. Western countries are showing little interest due to the poor input/output ratio resulting from low grain prices. Brazil remains a major player, making significant purchases with a focus on competitive suppliers such as Iran and China, obtaining occasional discounts,” he notes.

In Argentina, demand for urea continues to be affected by local economic uncertainty and low grain prices (the country applies agricultural export duties and intervenes in the exchange rate), which limit commercial operations.

Meanwhile, this week the global phosphate fertilizer market faced significant movements and challenges. The main focus was on India, where concerns about DAP shortages increased significantly ahead of the “Rabi” agricultural season.

“Although India secured supply agreements with Saudi Arabia and Morocco, a government directive not to exceed a purchase price of US$810/ton CFR led to the cancellation of a tender for 50,000 tons. However, the national fertilizer company purchased 50,000 tons of Moroccan DAP at US$814/ton CFR, an increase of US$10/ton over the previous week,” the report explains.

In China, the market remained stable with significant limitations due to uncertainties about new government export quotas. The FOB price for 64% DAP remained stable at US$760/ton.

“Brazil presented a complex situation with a mismatch between domestic prices and import costs. Although CFR prices remained stable between US$755 and US$765/ton, local demand indicated that realistic levels would be closer to US$730. Importers were cautious, operating on immediate demand and avoiding accumulation of costly inventories. Mosaic opened a plant in Tocantins, projecting significant domestic growth,” it said.

Finally, in Morocco, the national company OCP made significant sales to India and Europe, consolidating its role as a key supplier in those destinations. Russia also stood out with stable prices and NPK sales to India, reflecting sustained demand for complex fertilizers.

Source: Valor Soja

Mosaic opens new fertilizer plant in Palmeirante

Unit expands blending capacity and strengthens the company’s presence in northern Brazil

Mosaic Company begins operations this month at its new fertilizer blending, storage, and distribution facility in Palmeirante, Tocantins. The inauguration will take place today (16) in the presence of local authorities and Mosaic’s executive vice president, Jenny Wang.

With an annual capacity to process 1 million tons of fertilizers, the new unit is expected to process around 500 tons by 2025. The project expands the company’s presence in the north of the country and strengthens its growth strategy in the Matopiba region – an agricultural frontier comprising areas of Maranhão, Tocantins, Piauí, and Bahia.

The plant received an investment of US$84 million. According to the company, the project was delivered on time and within budget. The expected margin is US$30 to US$40 per ton, with an internal rate of return exceeding 20%.

The facility includes warehouses, automated mixing and bagging systems, and a direct rail link to the port of Itaqui, Maranhão. This logistical connection aims to reduce operating costs and ensure quality control with cutting-edge technology.

Mosaic’s projection is to increase distribution sales in Brazil, from less than 8 million tons in 2024 to up to 14 million by the end of the decade.

“With the new unit, we’re taking an important step toward making Tocantins an even stronger and more competitive hub within the national agribusiness sector. This modern structure allows us to be closer to producers, offering technological solutions and a high level of service. Furthermore, we reaffirm our commitment to local socioeconomic development, generating jobs, income, and opportunities in the region. Palmeirante is an important milestone for us, aligned with the company’s long-term strategy,” says Eduardo Monteiro, Country Manager at Mosaic.

Source: Cultivar Magazine

ARGENTINA MAIN CROPS OVERVIEW:

WHEAT: Wheat planting is at 92.8% of the projected area of 6.7 million hectares, after week-on-week progress of only 1.8 percentage points, due to delays caused by new rains in areas complicated by excess water. Specifically, in central and southeastern Buenos Aires, work has been completely halted pending better soil conditions for the entry of seeders, and there have even been reports of some losses of planted area due to flooding that may require replanting. Meanwhile, in the center and north of the agricultural area, where work is practically complete, crops are developing and maintaining Normal to Excellent growing conditions in 96.9% of the area, setting an encouraging scenario for the transition to tillering and stem elongation in the early-planted plots.

CORN: With regard to corn for commercial grain, the harvest of late crops continues to progress at a good pace in the center and north of the agricultural area, with an interweekly progress of 8.5 percentage points, reaching 78.9% of the national total. To date, cumulative production is estimated at 40.4 million tons. In the province of Córdoba, harvesting already covers 83.6% of the area, with an average yield of 77.6 qq/Ha. Very good results are noted in fields planted at the end of December, while those planted between the end of November and the beginning of December show more irregular yields. In the south-central agricultural area, widespread rainfall in the region has hampered the progress of the harvest, causing an average delay of 10 percentage points compared to previous seasons. In this context, the national production forecast remains at 49 million tons.

SORGHUM: The grain sorghum harvest advanced 8.5 percentage points in the last fifteen days, reaching 82.4% of the total estimated area for the season, with an average yield of 36.5 quintals per hectare. In the Northern Core area, work has been completed, with an average yield of 52.7 qq/Ha and a total production of 120,000 tons. Meanwhile, in the province of Córdoba, harvesting tasks are in their final stage, with good yields of around 48 qq/Ha. to the north of the agricultural area, the NE region reports that 68% of the harvest has been completed, with an average yield of 27.3 qq/Ha. In this context, the national production forecast remains at 3 MTn.